/American%20Express%20Co_%20logo%20on%20building-by%20BalkansCat%20via%20Shutterstock.jpg)

Valued at a market cap of $249.8 billion, American Express Company (AXP) is an integrated payments company based in New York. It is best known for its premium charge cards and credit cards, offering payment, expense management, and travel-related services to consumers, small businesses, and large enterprises.

Companies worth $200 billion or more are typically classified as “mega-cap stocks,” and AXP fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the credit services industry. The company differentiates itself through rewards-focused, high-spending cardmembers, strong brand loyalty, and partnerships with merchants and travel providers. Its focus on affluent customers, premium benefits, and tailored financial products continues to drive growth in billings, card spending, and membership revenue.

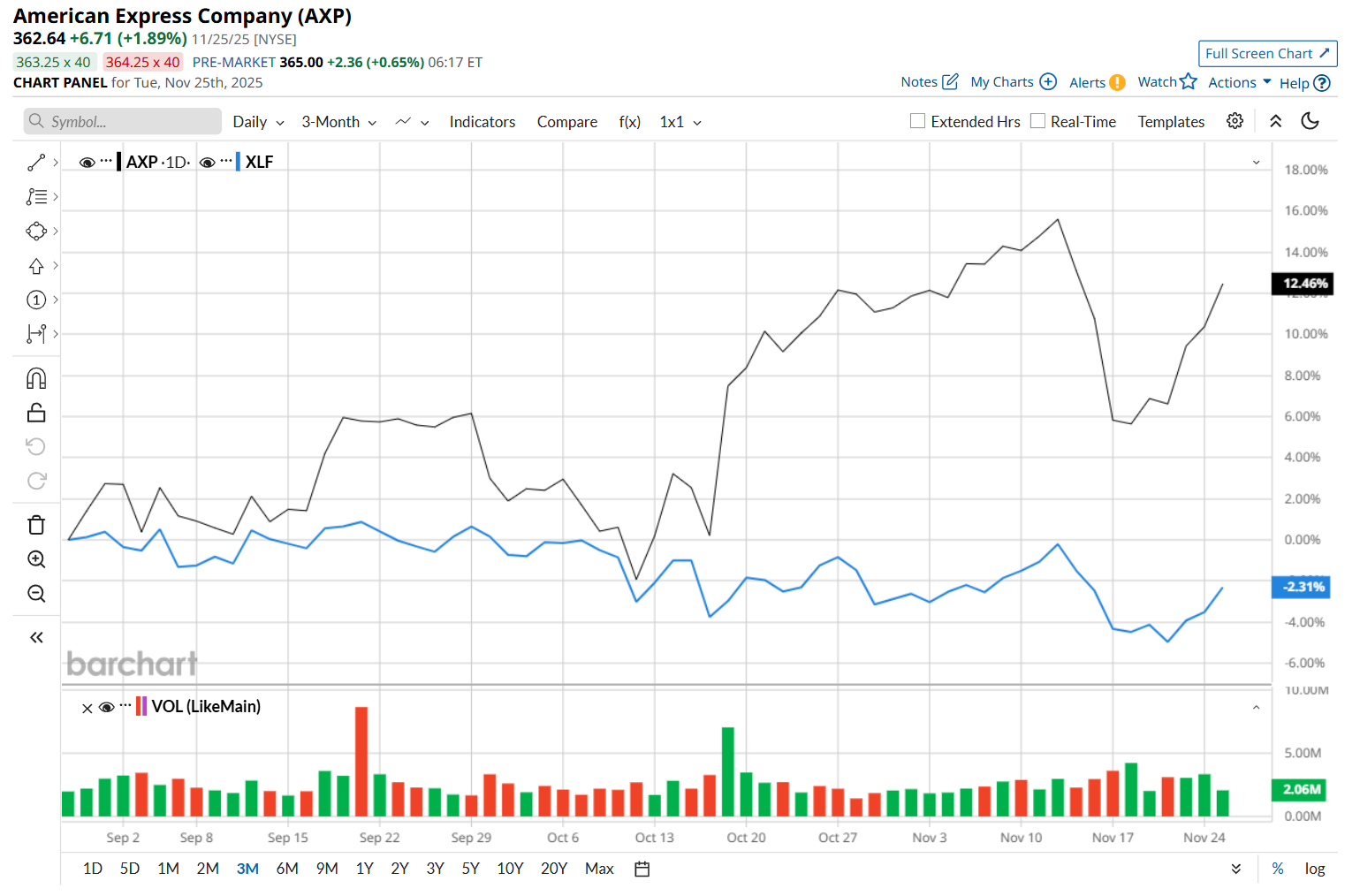

This credit card giant is currently trading 3.9% below its 52-week high of $377.23, reached on Nov. 12. Shares of AXP have gained 14.8% over the past three months, outpacing the Financial Select Sector SPDR Fund’s (XLF) 1.4% drop during the same time frame.

In the longer term, AXP has soared 18.8% over the past 52 weeks, considerably outperforming XLF's 2.9% return over the same time period. Moreover, on a YTD basis, shares of AXP are up 22.2%, compared to XLF’s 8.7% surge.

To confirm its bullish trend, AXP has been trading above its 200-day and 50-day moving averages since early May, with slight fluctuations.

On Oct. 17, shares of AXP soared 7.3% after its better-than-expected Q3 earnings release. The company’s revenue increased 10.8% year-over-year to a record $18.4 billion, surpassing consensus expectations by 2.4%. Moreover, its EPS soared 18.6% year-over-year to $4.14, beating analyst estimates by 4.5%. Observing the strong momentum, American Express raised its fiscal 2025 revenue and earnings guidance, further bolstering investor confidence. Strong spending growth among card members and robust early demand and engagement for its U.S. Consumer and Business Platinum Cards supported its results.

AXP has also outperformed its rival, Visa Inc. (V), which gained 6.8% over the past 52 weeks and 5.9% on a YTD basis.

Given AXP’s recent outperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 29 analysts covering it. While the company is trading above its mean price target of $355.08, its Street-high price target of $400 suggests a 10.3% premium to its current price levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.