Galecto (GLTO) shares more than quadrupled on Monday after the biotech firm said it has acquired Delaware-headquartered Damora Therapeutics for an undisclosed amount.

The acquisition could complement GLTO’s existing galectin-targeted therapies, creating a more diversified portfolio in specialized disease areas with significant unmet medical needs.

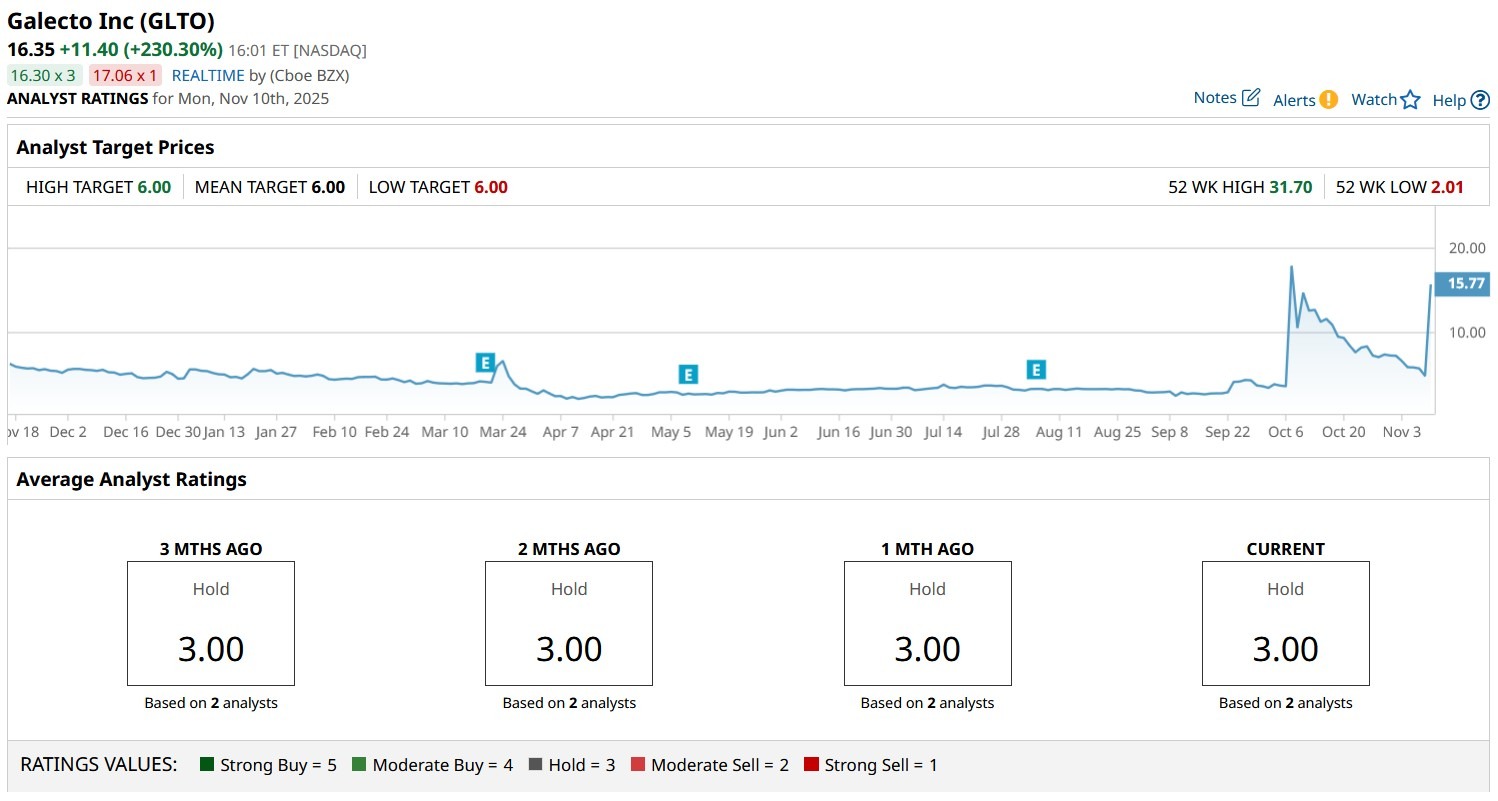

Still, there’s reason to immediately cut exposure to GLTO stock that, at one point on Nov. 10, was seen trading at about 9x its price in early April.

Why GLTO Stock Isn’t Worth Buying on Damora News

The explosive move in Galecto stock today looks egregiously overdone as it ignores the significant execution and integration risks tied to the Damora Therapeutics acquisition.

Integration, in particular, poses a major threat given the complexity of merging two biotech firms with different research focuses and corporate cultures.

Plus, the pharma industry has a notoriously poor track record with acquisitions, with failure rates often exceeding 70% due to overoptimistic synergy projections and operational misalignments.

More importantly, since GLTO was a penny stock ahead of the Damora news, its price action today is more akin to a meme stock rally that typically fades just as quickly as it erupts.

Galecto Shares Lack Any Further Upside From Here

Investors are cautioned against participating in the GLTO share price surge following the Damora announcement as it may be more sentiment-driven than fundamentally supported.

Even the buyout is largely positive for Galecto, the related upside appears more than incorporated already, leaving little to no upside potential for new investors jumping in at the current elevated levels.

At $16 roughly, the biotech stock is pricing in overly optimistic assumptions about future clinical outcomes and execution that hasn’t materialized yet.

This has created an unsustainable valuation bubble that may prove rather hurtful for late investors.

Wall Street Remains Uninterested in GLTO Shares

Another red flag for those interested in owning Galecto shares heading into 2026 is the absence of broad Wall Street coverage, which makes it challenging to value the company.

GLTO stock currently receives coverage from just two analysts – and even they rate it at “Hold” only. The mean target of $6 on the biotech firm signals potential for a massive crash ahead.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/United%20Parcel%20Service%2C%20Inc_%20logo%20on%20truck-by%20100pk%20via%20iStock.jpg)

/A%20close-up%20of%20the%20SpaceX%20sign%20on%20a%20black%20building%20by%20IanDewarPhotography%20via%20Adobe%20Stock.jpeg)