With a market cap of $9 billion, Molson Coors Beverage Company (TAP) is a global beverage manufacturer headquartered in Chicago, Illinois. The company produces a diverse portfolio of alcoholic and non-alcoholic beverages, including iconic beer brands such as Coors Light, Miller Lite, and Molson Canadian, as well as flavored malt beverages, hard seltzers, and ready-to-drink (RTD) cocktails.

Companies worth between $2 billion and $10 billion are generally described as "mid-cap stocks," Molson fits right into that category. TAP leverages several competitive strengths to maintain its position in the global beverage market. The company boasts a diverse portfolio of iconic beer brands like Coors Light, Miller Lite, Blue Moon, and Molson Canadian, catering to a wide range of consumer preferences.

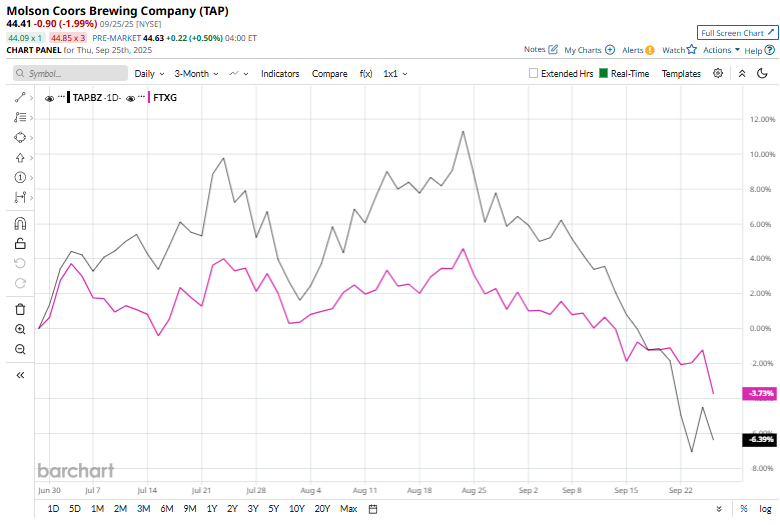

Despite its notable strengths, Molson stock is currently trading 31.3% below its 52-week high of $64.66 on Mar. 10. Molson has gained 6% over the past three months, surpassing the Nasdaq Food & Beverage ETF’s (FTXG) 3.9% rise over the same time frame.

Molson’s performance has remained mixed over the longer time frame. Molson’s stock dropped 22.5% in 2025 and declined 18.7% over the past 52 weeks. In contrast, FTXG has dipped 7.9% on a YTD basis and 16.7% over the past year.

To confirm the recent downtrend, Molson has been trading mostly below its 50-day and 200-day moving averages since the end of April.

On Sept. 12, Molson Coors shares declined over 1% after Barclays plc (BCS) downgraded the stock from “Equal Weight” to “Underweight.” The downgrade reflected the firm’s cautious outlook on the company’s near-term growth prospects, citing potential headwinds in the U.S. beer market, slower-than-anticipated premiumization trends, and pressure from rising input costs.

Furthermore, Molson has significantly outperformed its peer Constellation Brands, Inc.’s (STZ) 40% decline this year and a 47.3% drop over the past 52 weeks.

Among the 22 analysts covering the TAP stock, the consensus rating is a “Hold.” Its mean price target of $54.14 suggests a 21.9% upside potential from current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)