/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

The similarities between clean energy solutions provider FuelCell (FCEL) and cloud infrastructure services player Oracle (ORCL) have been eerily similar in recent times. The share prices of both companies jumped as the investor community welcomed the solid showing by both in their most recent quarterly results. Another parallel between the two has been the significant jump in their respective order backlogs.

However, that is where the sameness ends, as the two companies are as different as they can be. While Oracle is a global name with a long track record of profitability and a market cap of close to a trillion dollars, FuelCell is an unprofitable company that operates in the clean energy sector and is a penny stock with less than half a billion dollars of market cap.

Moreover, Oracle co-founder Larry Ellison shares a friendly bond with President Trump, thanks to the Stargate initiative. Conversely, Trump's previous assertions about climate change and clean energy have been anything but complimentary, which have now been backed by policy action.

About FuelCell

Founded in 1969, FuelCell is a U.S.-based company that designs, builds, operates, and services fuel cell power plants and related clean energy technologies. Their offerings include utility-scale and on-site power generation, electrolysis (hydrogen production), carbon capture, energy storage, and similar technologies.

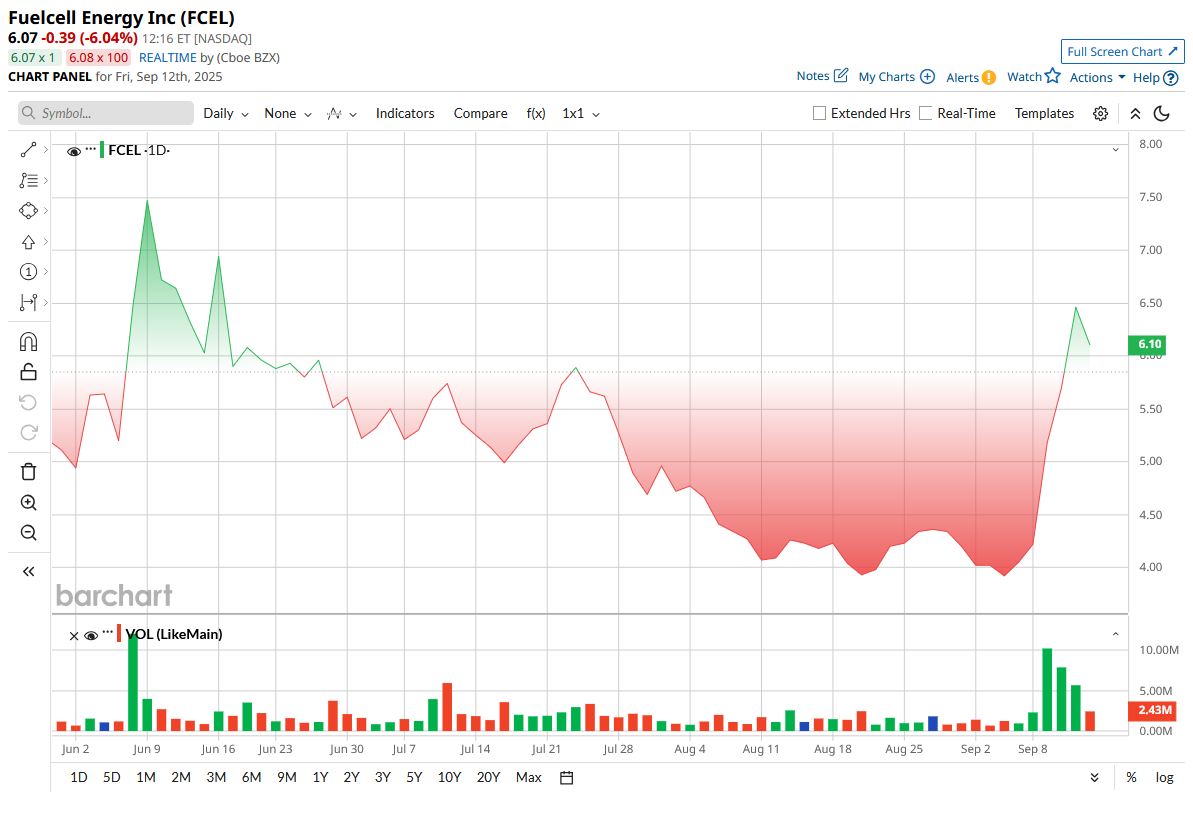

Valued at a market cap of $129.91 million, the FCEL stock is down 32.5% on a year-to-date (YTD) basis but has surged by a whopping 50.6% in less than a week, thanks to its better-than-expected results on some fronts, especially the substantial rise in its order book.

So, that begs the question: Can, despite an increasingly hostile political environment, an investment in FCEL be a prudent move now, or has the run-up been too much for an unprofitable company? Let's try to find out.

Financials Leave a Lot To Be Desired

Granted, FuelCell's results for the third quarter were good, but the unhinged optimism around FCEL stock seems misplaced. Although revenues almost doubled to $46.7 million, compared to $23.7 million in the year-ago period, the loss per share figure mirrored the same in the opposite direction, as it widened to $3.78 from $1.99 in the previous year. Notably, this marked the second consecutive quarter of bottom-line miss from the company. On an operating level, losses witnessed an even sharper rise to $95.4 million from $33.6 million in Q3 2024.

Moreover, the increase in backlog was also nothing noteworthy (certainly did not warrant such a dramatic uptick in the share price), as it went up by a mere 4% on a year-over-year (YoY) basis to $1.24 billion. In fact, the backlogs for the product (-29.6% YoY, $96.2 million) and service segments (-5% YoY, $169.4 million) actually went down when compared to the same period a year ago. However, its biggest segment of generation jumped by 13.8% from the prior year to about $955 million, which was a positive development.

Further, net cash used in operating activities fell to $102.4 million for the nine months ended July 31, 2025, from $158.8 million in the year-ago period. Overall, the company closed the quarter with a cash balance of $174.66 million, much higher than its short-term debt levels of $17.51 million. This makes FuelCell's liquidity position a strong one, allowing it to cushion some of its continued net losses.

Yet, its growth leaves a lot to be desired, with an abysmal 10-year revenue CAGR of -0.85%. Moreover, the company has been around for more than half a century, and it has never reported profits.

Not Met Expectations

Since my somewhat bullish piece on FuelCell, which was the last time I covered the company, FCEL stock has plummeted by a considerable 69.2%, as the company failed to take advantage of the opportunities and remained an inert player in the booming renewable energy space.

Some corrective steps are underway, though their effectiveness remains uncertain. FuelCell Energy has chosen to concentrate on its core molten carbonate fuel cell platform while discontinuing its push to commercialize solid oxide fuel cell technology. The withdrawal from that initiative is expected to trigger impairment charges of more than $60 million. Yet, despite this refocus, the company has seen limited success in attracting new orders for its long-standing molten carbonate fuel cell platform in recent years, aside from a single project in Hartford, CT. Compounding matters, production is being scaled back further at its Torrington facility, which has already been operating well below capacity.

These adjustments appear modest when viewed against the competitive landscape. FuelCell continues to lag peers such as Bloom Energy (BE), both in terms of product development and market traction. While a strategic arrangement was announced earlier this year with Diversified Energy (DEC) and TESIAC for the supply of up to 360 MW, the reality is that FuelCell’s systems often face long lead times before reaching commercial operation and carry higher production and operating costs.

Meanwhile, the company’s carbon capture demonstration project with an ExxonMobil (XOM) subsidiary in Rotterdam will not begin until 2026. Even if the pilot proves viable, commercialization is unlikely to occur for several more years thereafter.

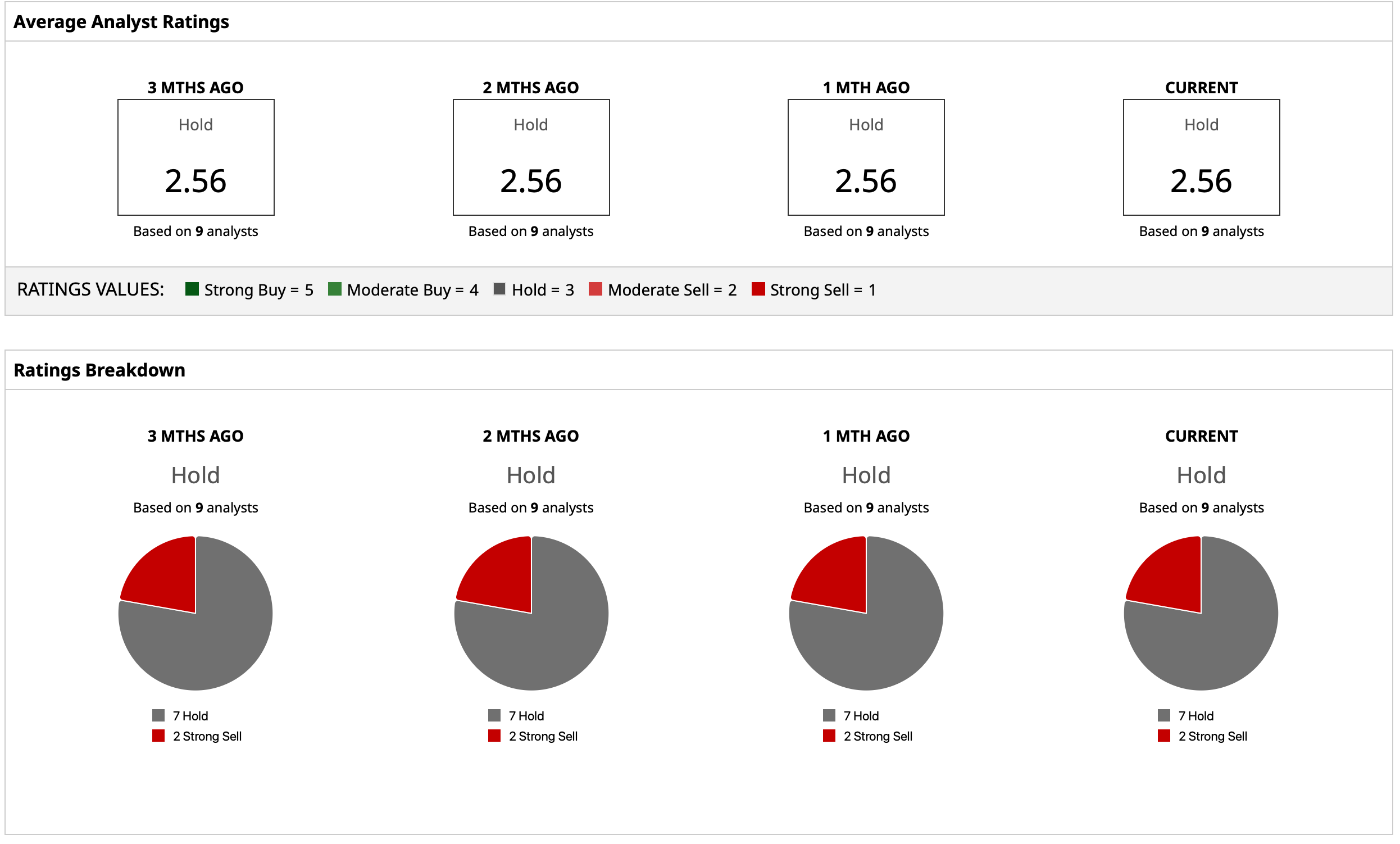

How Do Analysts Rate FCEL Stock?

Thus, analysts have retained a “Hold” rating on FCEL stock, with a mean target price of $7.38. This denotes an upside potential of about 23% from current levels. Out of nine analysts covering the stock, seven have a “Hold” rating, and two have a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)

/Broadcom%20Inc%20HQ%20photo-by%20Sundry%20Photogrpahy%20via%20iStock.jpg)

/AI%20(artificial%20intelligence)/3D%20Graphics%20Concept%20Big%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)