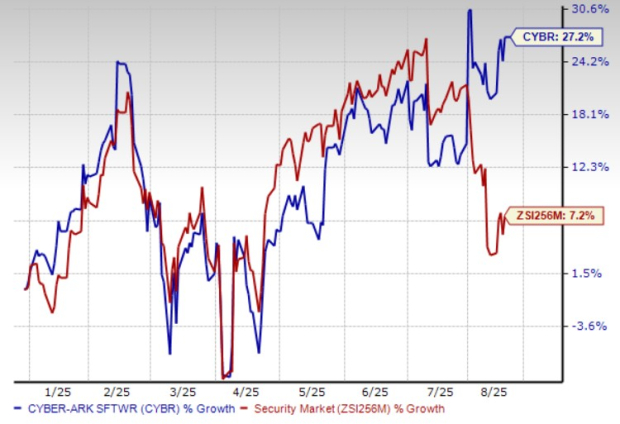

CyberArk Software CYBR shares have gained 27.2% in the year-to-date period, outperforming the Zacks Security industry’s growth of 7.2%. This outperformance raises the question: Should investors accumulate CYBR shares or book profits and exit the investment?

CyberArk YTD Performance Chart

Image Source: Zacks Investment Research

CyberArk Grows on the Back of Identity Security

CyberArk is experiencing massive traction in its identity security offerings, which have crossed the milestone of 10,000 active users worldwide, witnessing a CAGR of 44% from 2020 to 2024. The company projects a total addressable market of $80 billion, giving it huge growth opportunities. In its second quarter of 2025, CYBR’s subscription revenues came in at $264 million, representing year-over-year growth of 66%.

CYBR’s implementation of AI solutions, including CyberArk Secure AI Agents Solution and CORA AI, and its collaboration with Accenture to integrate Accenture’s AI Refinery have deepened its portfolio. The implementation of CORA AI and Secure AI Agents into CyberArk’s identity security platform will aid its customers to secure a full spectrum of identities, including human, AI and machine. The company will also benefit from Accenture's client base with large-scale deployments.

Furthermore, CYBR is also expanding its capabilities through inorganic growth. CYBR’s acquisitions of Zilla Security and Venafi have expanded its expertise in identity governance and machine identity. The acquisitions also enhanced its recurring revenues and market share. The identity security and access management market in which CyberArk operates is expected to witness a CAGR of 8.4% from 2024 to 2029, according to a report by MarketsAndMarkets. This makes CYBR more prospective. The Zacks Consensus Estimate for CyberArk’s 2025 earnings is pegged at $3.86, indicating a year-over-year rise of 27.4%.

Image Source: Zacks Investment Research

Collaboration With Industry Giants Aids CYBR’s Growth

CYBR is a crucial security ally for more than 5,400 global businesses, which comprise over 50% of the Fortune 500 and 35% of the Global 2000 companies. One of the key drivers for customer growth is CyberArk’s strategic partnerships with tech giants like Microsoft, Amazon’s Amazon Web Services and Alphabet’s Google Cloud.

By integrating its solutions with Microsoft’s Azure Active Directory, AWS’ cloud infrastructure and Alphabet’s Google Cloud, CyberArk deepened its ability to secure cloud environments, offering robust identity management solutions across various IT ecosystems.

With all these enhancements in place, CyberArk provides its customers with comprehensive and integrated security solutions, making CYBR an indispensable cybersecurity player. Based upon the strong prospects of CYBR’s business outlook, Palo Alto Networks has agreed to buy CyberArk for about $25 billion at a premium over its 10-day average price as of July 25, 2025.

Key Headwinds Faced by CyberArk

The broader identity security and access management space consists of several players, including CrowdStrike CRWD, Okta Inc. OKTA and Cisco CSCO, which are also implementing AI in their products. Okta provides Identity Threat Protection with Okta AI so enterprises can leverage AI and machine learning techniques for real-time detection of the entire spectrum of Identity attacks.

CrowdStrike is also an established player in the identity security space, providing unified, real-time protection across cloud, identity and endpoint. CRWD is enhancing its identity security platform with the implementation of AI copilots like Charlotte AI and agentic AI solutions like Charlotte AI Agentic Workflows

Cisco provides Identity Intelligence, which is a cutting-edge AI-driven solution intentionally designed to bridge the gap between identity authentication and access control. Its offerings include Duo Smart Authentication, Cisco Secure Access and XDR. To survive in the highly competitive cybersecurity market, each player must continually invest in broadening its capabilities. Over the past few years, CyberArk has invested heavily to enhance its sales and marketing capabilities, particularly by increasing its sales force.

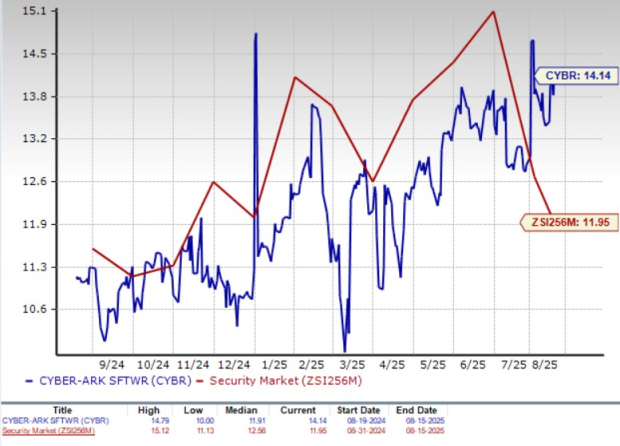

CyberArk Trades at a Premium Valuation

From a valuation standpoint, CYBR trades at a forward price-to-sales ratio of 14.14X, above the industry’s 11.95X.

CyberArk Forward (P/S) Valuation Chart

Image Source: Zacks Investment Research

Conclusion: Buy, Sell or Hold the Stock?

CyberArk’s innovative cybersecurity portfolio with AI integration makes it well-positioned to benefit from the strong TAM of the identity security space. This bodes well for long-term investors. However, it faces competitive and macroeconomic challenges at present and is trading at a premium valuation.

Considering these factors, we suggest that investors should wait for a more favorable opportunity and retain the stock if they have already bought it. CyberArk currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Free Report: Profiting from the 2nd Wave of AI Explosion

The next phase of the AI explosion is poised to create significant wealth for investors, especially those who get in early. It will add literally trillion of dollars to the economy and revolutionize nearly every part of our lives.

Investors who bought shares like Nvidia at the right time have had a shot at huge gains.

But the rocket ride in the "first wave" of AI stocks may soon come to an end. The sharp upward trajectory of these stocks will begin to level off, leaving exponential growth to a new wave of cutting-edge companies.

Zacks' AI Boom 2.0: The Second Wave report reveals 4 under-the-radar companies that may soon be shining stars of AI’s next leap forward.

Access AI Boom 2.0 now, absolutely free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cisco Systems, Inc. (CSCO): Free Stock Analysis Report

CyberArk Software Ltd. (CYBR): Free Stock Analysis Report

Okta, Inc. (OKTA): Free Stock Analysis Report

CrowdStrike (CRWD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Super%20Micro%20Computer%20Inc%20logo%20on%20building-by%20Poetra_RH%20via%20Shutterstock.jpg)