/Super%20Micro%20Computer%20Inc%20logo%20on%20building-by%20Poetra_RH%20via%20Shutterstock.jpg)

Investors once treated Super Micro Computer (SMCI) as a clean proxy for the artificial intelligence (AI) buildout. The company rode a powerful demand wave, strengthened its ties with NVIDIA Corporation (NVDA), and embedded itself deep within the architecture of modern data centers.

But now a legal overhang has begun to cast a long shadow, forcing investors to reevaluate risk even as the core business continues to expand at pace. The issue traces back to two individuals tied to the company: co-founder Wally Liaw and contractor Willy Sun, who have pleaded not guilty in a U.S. court over allegations of the illegal shipment of Nvidia-powered servers to China.

A third individual, Ruei-Tsang “Steven” Chang, who served as a sales manager in Supermicro’s Taiwan office and is linked to the case, remains at large. Meanwhile, U.S. District Judge Edgardo Ramos has set a Nov. 2 trial date, establishing a clear timeline for what could still become a prolonged legal process.

Prosecutors allege that the group removed labels and serial numbers from servers and replaced them with dummy identifiers to bypass export controls. These efforts reportedly generated around $2.5 billion in sales for the server maker since 2024, including $510 million worth of shipments between late April 2025 and mid-May 2025 routed through a Southeast Asian entity before reaching China.

While Super Micro itself has not been charged, the situation has started to spill over into market perception. The stock has fallen 27.5% in the past month since the case surfaced on March 19, highlighting the quick erosion of confidence when governance risks come into focus.

At the same time, U.S. authorities have already been tightening scrutiny around AI chip exports, particularly those tied to Nvidia. The case adds another layer of pressure to an already sensitive regulatory backdrop. Now, let us see whether Super Micro can absorb this pressure without cracking under it.

About Super Micro Stock

The San Jose, California-based Super Micro Computer designs and delivers modular, open-architecture server and storage systems tailored for AI, cloud, and enterprise workloads.

With a market cap of $13.5 billion, the company has built its edge on flexibility, offering GPU-accelerated platforms, blade servers, and rack-scale solutions that allow customers to deploy high-performance infrastructure at speed and scale.

Still, SMCI stock has struggled to find its footing, falling 21.16% year-to-date (YTD) and sliding 34.24% over the past 52 weeks.

From a valuation standpoint, SMCI stock is currently trading at 10 times forward adjusted earnings and 0.33 times sales. The figures sit at a notable discount to industry peers as well as their own five-year average multiples.

Super Micro Surpasses Q2 Earnings

Super Micro’s fiscal Q2 fiscal year 2026 results, reported on Feb. 3, painted an optimistic picture. Revenue surged 123.4% year-over-year (YOY) to $12.68 billion, comfortably ahead of analyst expectations of $10.44 billion. The figure also included $1.5 billion deferred from the previous quarter, reinforcing the scale and consistency of demand flowing through its pipeline.

Despite ongoing supply chain constraints, the company delivered record revenue, supported by strong order momentum from large-scale data center and enterprise customers. AI GPU platforms accounted for over 90% of total revenue, leaving little doubt about where the growth engine currently sits.

Adjusted EBITDA expanded 32.2% YOY to $628.6 million, while non-GAAP net income climbed 26.5% to $486.5 million. Adjusted EPS grew 16.9% from the prior year’s quarter to $0.69, clearing the Street’s forecast of $0.49 with room to spare. The market took notice, pushing the stock up 13.8% in the following trading session.

Management credited the momentum to strong adoption of its Rack Scale AI and Data Center Building Block Solutions, which continue to benefit from rapid deployment cycles and deeper partnerships with major cloud players. To that end, the company expects at least $12.3 billion in Q3 revenue and EPS of $0.60. For the full fiscal year 2026, it guides for at least $40 billion in revenue.

On the other hand, analysts project Q3 EPS to jump 184.2% YOY to $0.54. For the full fiscal year 2026, earnings are expected to grow 7% to $1.84, followed by another 38.6% rise to $2.55 in fiscal year 2027.

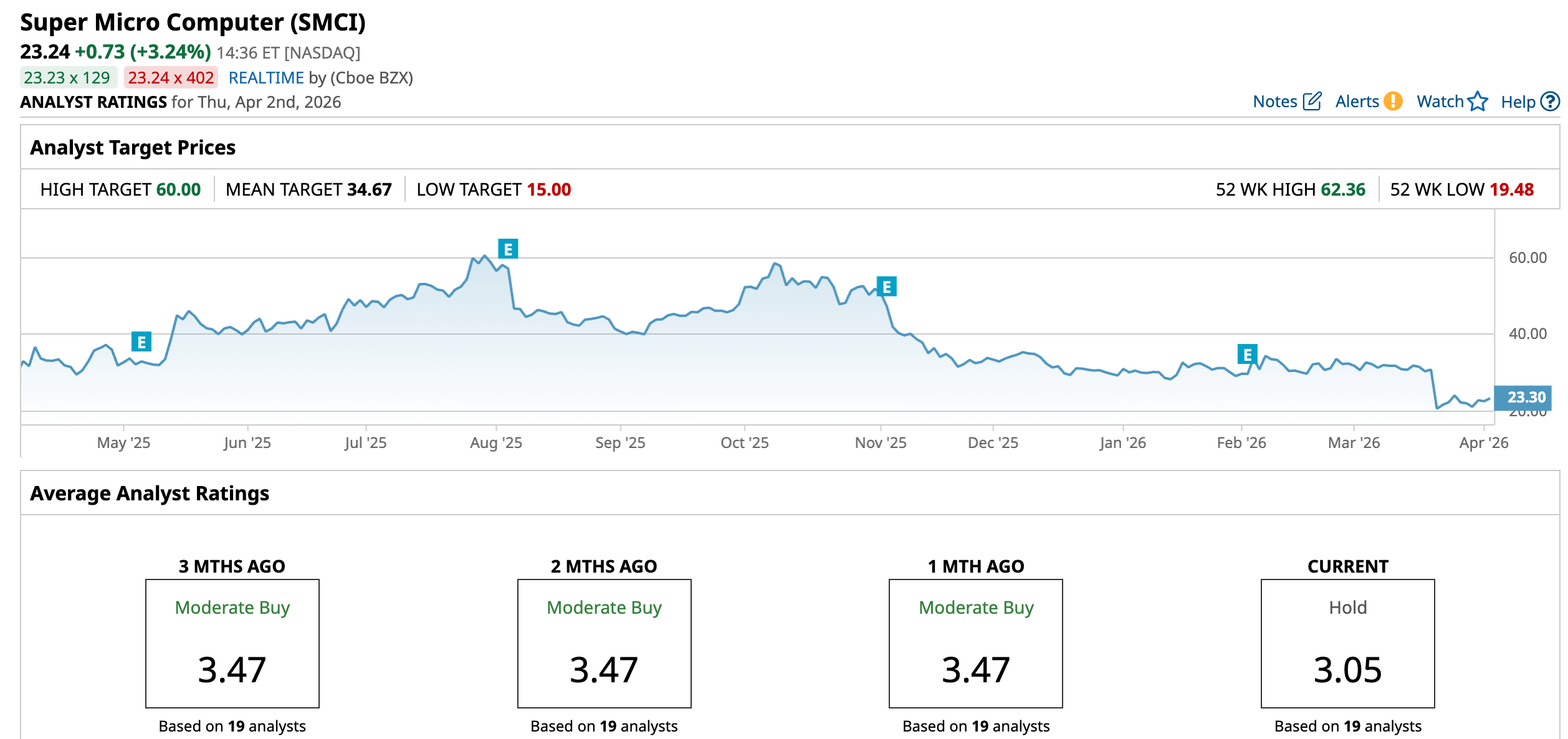

What Do Analysts Expect for Super Micro Stock?

Wall Street has started to recalibrate its stance, with the tone shifting noticeably. Rosenblatt analyst Kevin Cassidy maintains a “Buy” rating but has cut the price target to $32 from $50.

Elsewhere, the stance turns more guarded. Citigroup’s Asiya Merchant holds a “Neutral” rating while lowering the target to $25 from $39. BofA Securities analyst Ruplu Bhattacharya took an even more conservative view, maintaining an “Underperform” rating and trimming the price target to $24 from $34.

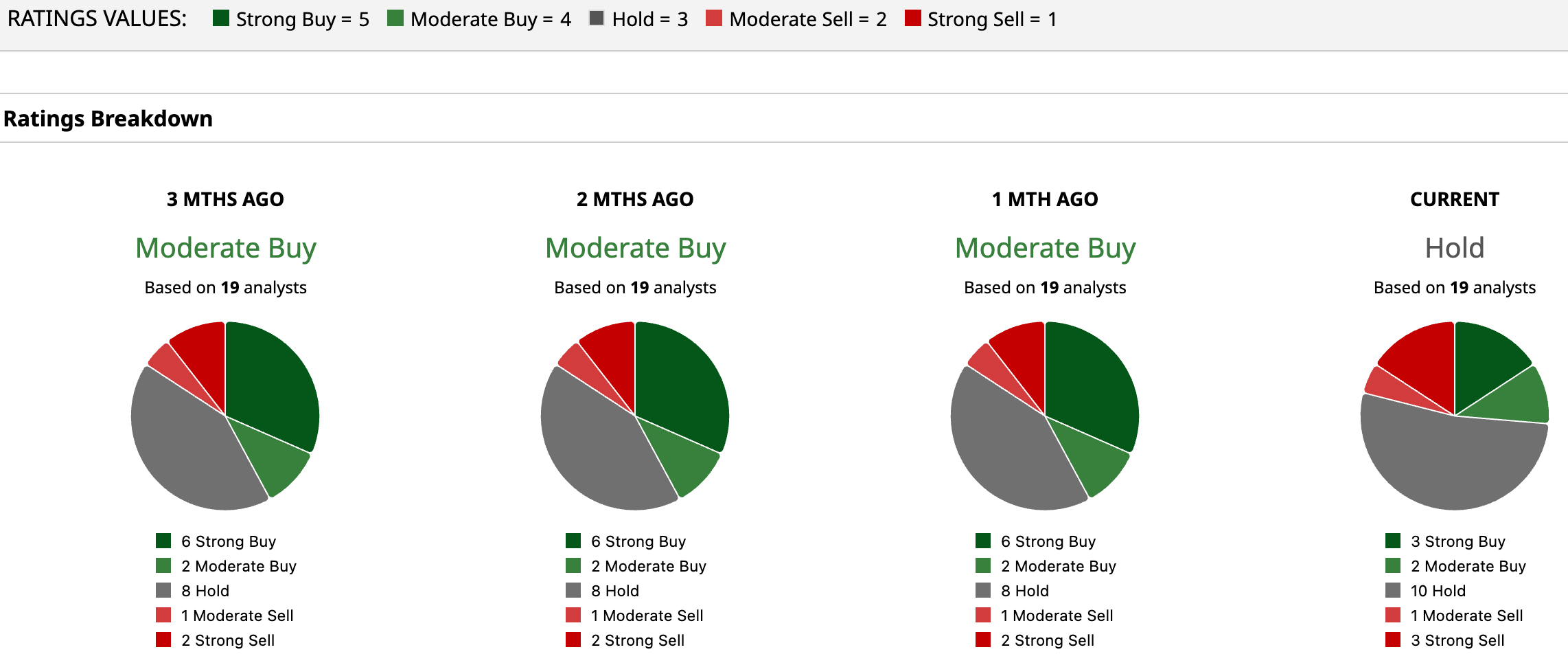

Overall, SMCI stock carries an overall rating of “Hold.” Out of 19 analysts covering the stock, three rate it a “Strong Buy,” two a “Moderate Buy,” 10 suggest “Hold,” one leans “Moderate Sell,” and three flag “Strong Sell.”

Yet, the mean price target of $34.67 signals potential upside of 49.2%. Meanwhile, the Street-high target of $60 suggests a gain of 158.2% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Bundle%20of%20optical%20fiber%20cables%20with%20lights%20by%20volff%20via%20Adobe%20Stock.jpeg)