Howdy market watchers!

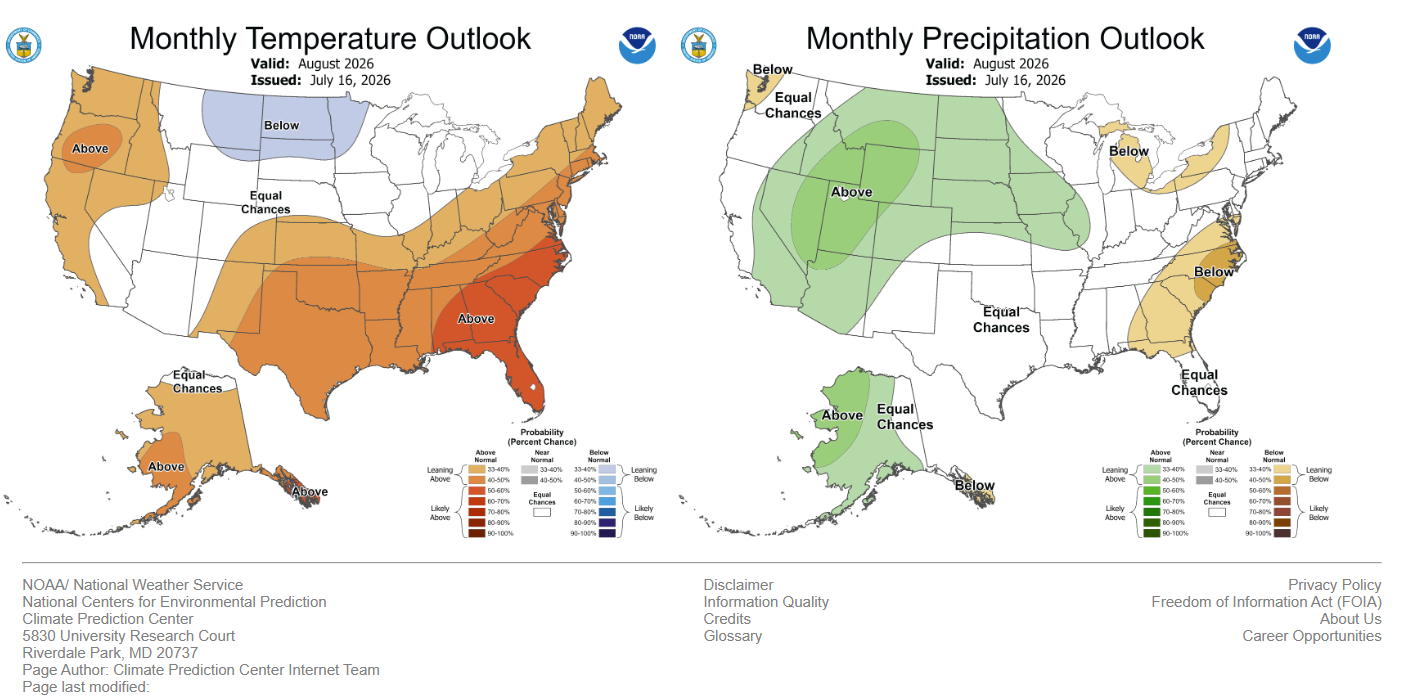

Agricultural commodity markets found renewed volatility this week as traders balanced favorable U.S. crop conditions against tightening global grain supplies, improving export demand, and a warmer, drier weather forecast across portions of the Corn Belt.

Following the July USDA World Agricultural Supply and Demand Estimates (WASDE) report, market participants shifted their focus from government balance sheets back toward weather during the critical reproductive stages for corn and soybeans. Meanwhile, cattle markets continued demonstrating exceptional strength on historically tight supplies, while energy prices stabilized after recent geopolitical volatility.

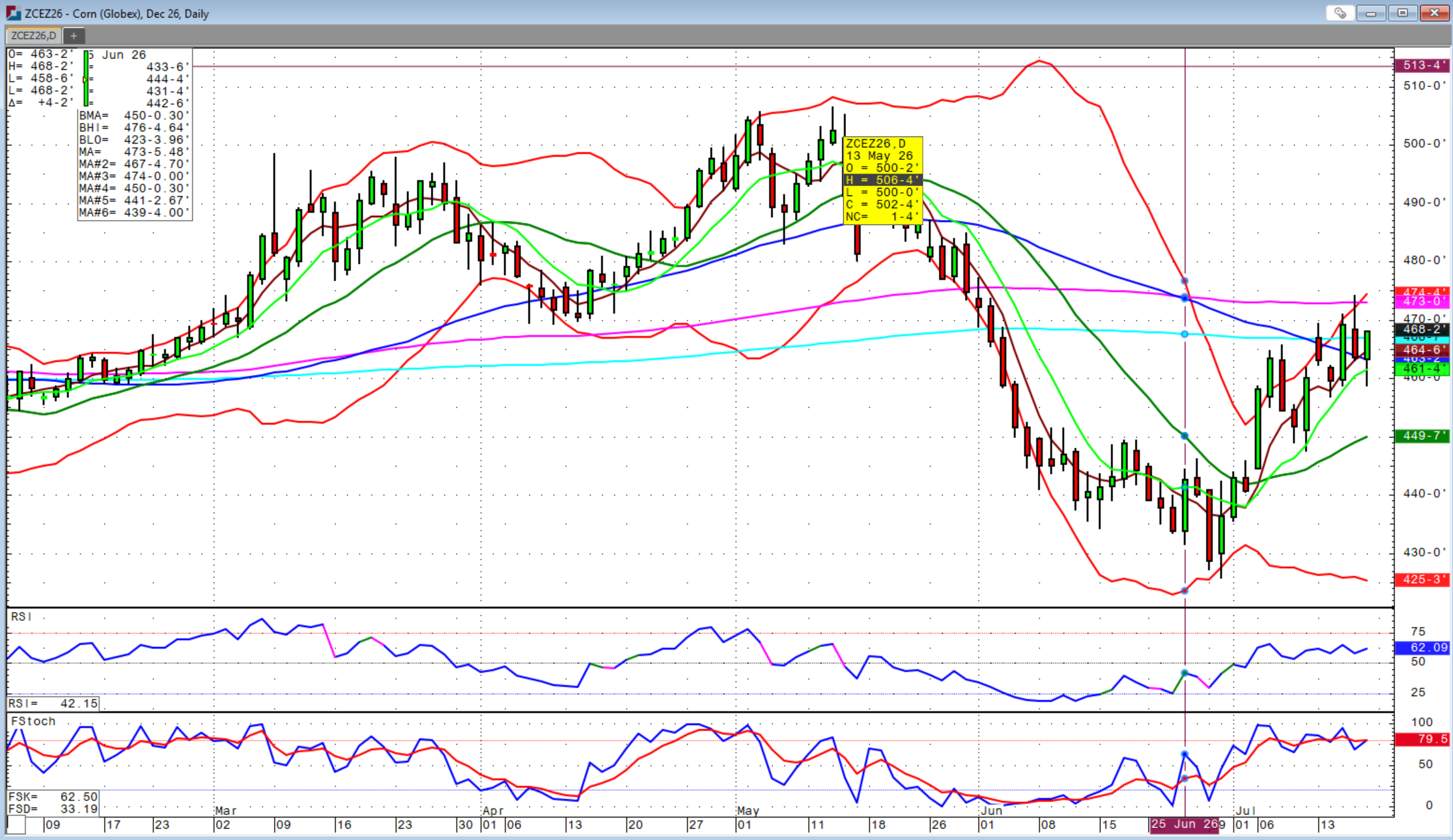

Corn futures posted modest gains this week after recovering from early pressure. While USDA's latest Crop Progress report rated 68% of the U.S. corn crop in good-to-excellent condition, one percentage point higher than the previous week, traders became increasingly focused on forecasts calling for hotter and drier conditions across portions of the western Corn Belt during pollination.

The July WASDE report maintained expectations for another large U.S. crop, but traders recognize that the next three weeks remain the most important period of the growing season. Pollination success will ultimately determine whether trend-line or above-trend yields can be achieved. Export demand has shown encouraging signs. Lower U.S. prices have improved competitiveness in world markets, while ethanol demand has remained relatively steady despite fluctuations in energy prices.

Although Brazil continues marketing a large second-crop corn harvest, U.S. export prospects have improved compared to earlier this summer. Investment funds have also begun reducing large short positions established earlier in the season, providing additional price support whenever weather forecasts become less favorable. For producers, weather will remain the dominant driver through the remainder of July. Any widespread heat combined with limited rainfall during pollination could quickly tighten production expectations and increase volatility.

Soybean futures strengthened during the week as renewed Chinese buying interest and developing weather concerns offset generally favorable crop conditions. USDA reported 65% of soybeans rated good-to-excellent, also improving from the previous week. However, soybeans enter their most weather-sensitive reproductive stages later than corn, meaning August weather historically carries even greater importance for final yields. China has returned to the U.S. export market more aggressively in recent weeks, providing an important boost to demand. Combined with continued domestic crush demand and stable renewable diesel production, soybean fundamentals have improved modestly.

The July WASDE report increased production expectations based on updated acreage estimates, but also projected stronger export demand, preventing a significant increase in ending stocks. As a result, traders interpreted the report as generally neutral.

Soybean oil has regained strength alongside higher crude oil prices earlier this month, although vegetable oil markets remain highly sensitive to changing biofuel policies and global palm oil production. The soybean market remains positioned to react quickly to August weather forecasts, particularly if forecasts shift toward prolonged heat or limited rainfall. Wheat futures experienced the strongest rally among the grain markets this week following USDA's reduced estimate for U.S. wheat production and increasing concerns regarding global supplies.

Harvest continues advancing across Kansas, Oklahoma, and Texas with mixed yield reports. While many producers are reporting respectable yields, protein levels and quality remain highly variable depending on localized rainfall patterns during harvest.

Globally, the wheat outlook has become increasingly supportive. The USDA now projects world wheat production only slightly below expected consumption, significantly reducing the surplus that has pressured markets during recent years. Smaller crops in portions of Europe and ongoing weather concerns in several exporting regions have narrowed the margin for production shortfalls. Despite these supportive fundamentals, global competition remains intense. Russia continues exporting aggressively, although declining acreage and weather concerns there will remain important market drivers heading into fall.

For Oklahoma and Kansas producers, strengthening basis opportunities may emerge if domestic millers begin competing more aggressively for higher-quality wheat supplies.

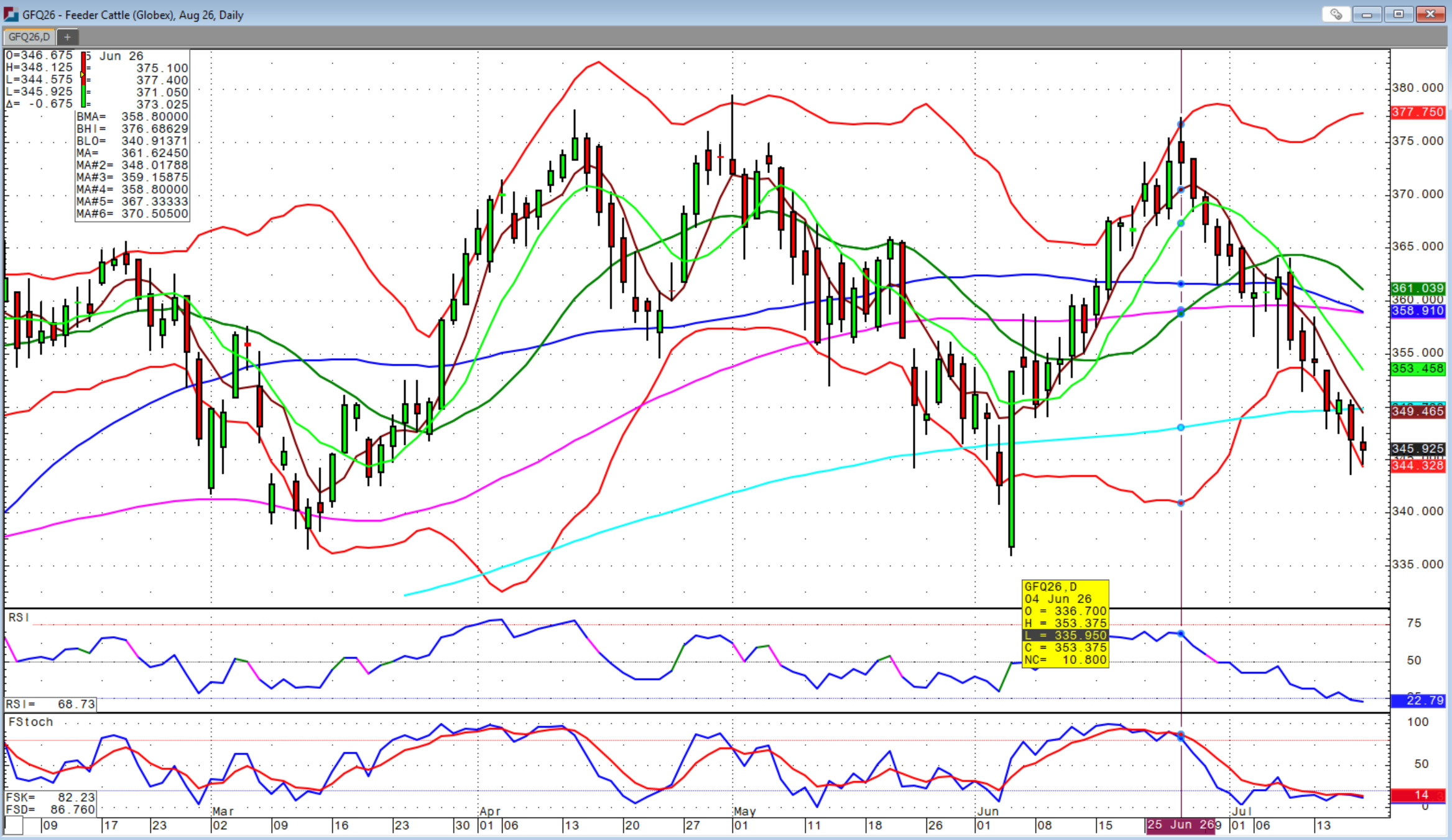

Live cattle and feeder cattle futures continued trading near record highs this week, supported by exceptionally tight cattle supplies and resilient consumer demand. The U.S. cattle herd remains at its smallest level in decades following multiple years of drought-driven liquidation. While improved pasture conditions have encouraged some herd rebuilding, expansion remains slow due to elevated replacement costs and continued uncertainty regarding long-term profitability.

Cash cattle markets remained firm throughout the week as packers competed aggressively for limited market-ready cattle. Beef demand has remained remarkably resilient despite historically high retail prices, allowing wholesale beef values to remain strong. Lower corn prices earlier this summer have modestly improved feeding margins, although feeder cattle prices remain historically expensive due to limited calf supplies. Most analysts expect cattle fundamentals to remain supportive well into 2027, although futures markets remain vulnerable to periodic profit-taking after reaching new contract highs.

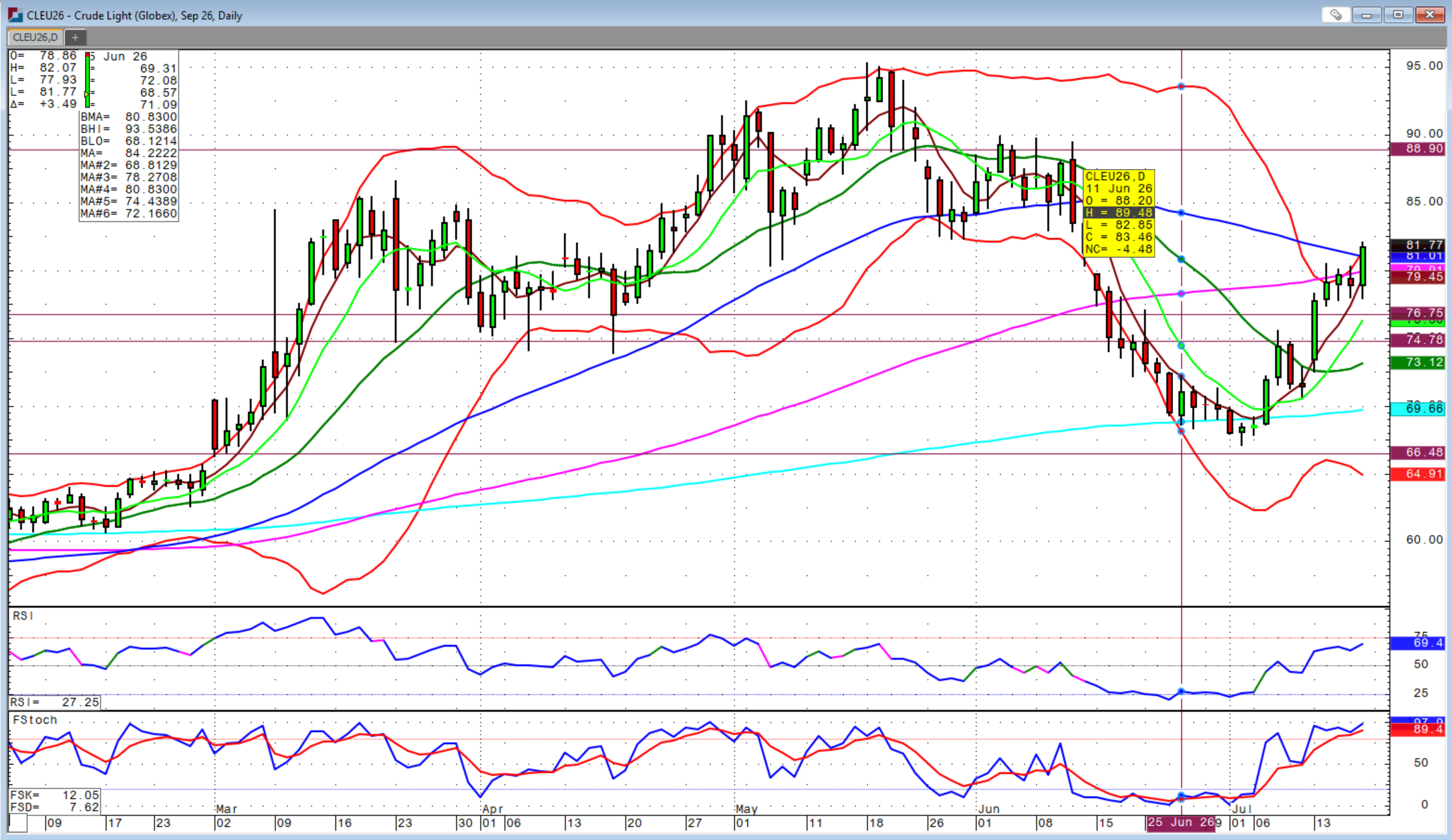

Energy markets remained volatile but generally stabilized this week following significant swings during recent geopolitical developments. Crude oil prices initially rallied on renewed Middle East tensions before retreating as immediate supply concerns eased. Even so, oil prices remain well above early summer lows, keeping diesel prices elevated for producers preparing for wheat harvest completion and fall fieldwork.

Natural gas prices have remained relatively firm as above-normal summer temperatures increase electricity demand across much of the United States. Storage inventories remain adequate, but traders continue monitoring weather forecasts closely as cooling demand increases. Energy prices remain particularly important for agriculture because they directly influence diesel fuel, grain transportation, drying costs, and nitrogen fertilizer production. Sustained strength in crude oil and natural gas could place upward pressure on fertilizer prices heading into fall application season.

As markets move deeper into July, weather has once again become the primary market driver. Corn enters its critical pollination period over the next several weeks, making temperature and rainfall forecasts especially important. Soybean traders will soon shift their attention toward August pod-setting weather, historically the crop's most critical development stage.

The latest USDA reports suggest global grain supplies remain adequate but are becoming less comfortable than in recent years. While another large U.S. harvest remains possible, global production margins have narrowed considerably, increasing the market's sensitivity to adverse weather events. Export demand also bears watching. Improved U.S. competitiveness has attracted additional interest from international buyers, particularly in soybeans, while wheat export opportunities could expand if production problems develop elsewhere in the world.

For livestock producers, fundamentals remain among the strongest seen in decades. Tight cattle inventories continue supporting historically high prices, and herd rebuilding is expected to remain gradual. Overall, commodity markets are entering one of the most weather-sensitive periods of the year. With favorable crop ratings providing a solid production foundation but global grain inventories tightening, volatility is likely to remain elevated throughout the remainder of July. Producers should remain disciplined with marketing plans while remaining prepared to capitalize on weather-driven rallies should growing conditions deteriorate.

Sidwell Strategies is the one-stop shop to protect cattle with futures, puts, LRP or a combination of all, which is probably the best strategy overall. If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available. It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Wishing everyone a successful trading week! Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

Brady Sidwell is a Series 3 Licensed Commodity Futures Broker and Principal of Sidwell Strategies. You’re your Trading Account with Sidwell Strategies at https://portal.stonex.com/prefill/index/BradySidwellU52F112P. Contact us at (580) 232-2272 or at trade@sidwellstrategies.com.

Futures and Options trading involves the risk of loss and may not be suitable for all investors. Review full disclaimer at https://www.sidwellstrategies.com/fccp-disclaimer-21951.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)