/Palo%20Alto%20Networks%20headquarters%20campus%20exterior%20of%20cybersecurity%20company%20By%20MichaelVi.jpeg)

Palo Alto Networks (PANW) stock has surged 113.5% over the past three months, fueled by strong recurring revenue growth, rising adoption of its unified cybersecurity platform, and increasing enterprise investment in artificial intelligence (AI).

As AI deployments expand and AI data centers rise, demand for cybersecurity is accelerating, positioning Palo Alto for sustained long-term growth.

PANW Platform Strategy Is Driving Larger Customer Relationships

Palo Alto's platformization strategy—combining multiple cybersecurity solutions into a single integrated platform—is becoming a major competitive advantage. Enterprises are increasingly replacing standalone security tools with unified platforms that simplify operations while lowering costs.

The strategy is driving higher customer retention, larger contracts, and broader product adoption. During the quarter, Palo Alto added 110 new platformized customers, bringing the total to about 2,280. These customers typically deploy multiple security products, resulting in net revenue retention of 120% and single-digit churn.

Management expects platformized customers to exceed 4,000 by fiscal 2030, supporting its long-term goal of reaching $20 billion in annual recurring revenue (ARR) from Next-Generation Security (NGS). Cross-selling also continues to improve as more customers adopt multiple products.

Palo Alto’s Recurring Revenue Continues to Strengthen

Third-quarter revenue increased 31% year-over-year (YOY) to $3 billion, supported by continued growth in software subscriptions and recurring services, which are improving revenue visibility.

NGS ARR climbed 60% to $8.13 billion. Although acquisitions, including CyberArk and Chronosphere, contributed approximately $1.63 billion, the company's core business also delivered strong organic growth.

Network Security Sustained Momentum

Network Security, which generates roughly 70% of Palo Alto's revenue, posted one of its strongest quarters in years. Growth accelerated across hardware, software firewalls, and Secure Access Service Edge (SASE) as enterprises invested in comprehensive network protection.

SASE ARR rose 40% YOY to $1.6 billion, while net new ARR expanded nearly 50%, driven by customer wins and competitive displacement.

Hardware also surprised to the upside. Although it accounts for only about 10% of revenue, the segment recorded its strongest quarter in a decade as firewall bookings surged by nearly 40%, supported by early AI data center deployments. As AI infrastructure expands, demand for advanced network security is expected to remain strong.

AI Is Emerging as a Major Growth Engine

AI is emerging as the company's most significant long-term growth driver. Palo Alto's software firewall business continues to deliver strong results, with ARR growing 25% as organizations increase their ability to inspect the rising volume of traffic between cloud environments and AI workloads. Meanwhile, Prisma AIRS, the company's AI security platform, remains its fastest-growing offering. Its customer base has expanded significantly, highlighting the rapid increase in enterprise demand for securing AI applications and infrastructure.

As businesses move beyond generative AI pilot projects to production-scale AI deployments and autonomous AI agents, cybersecurity requirements are becoming far more complex. This expanding threat landscape is creating new cybersecurity spending opportunities that go well beyond traditional endpoint and network security.

The rise of AI data centers and AI-powered enterprise networking is also opening a new hardware opportunity for Palo Alto. Growing demand for AI infrastructure could provide an additional long-term growth avenue for the company's firewall appliances.

Recent acquisitions further strengthen the company's AI strategy. The acquisition of Chronosphere enhances its AI observability capabilities, while Portkey strengthens its AI gateway security offering, positioning Palo Alto to provide more comprehensive security across the AI lifecycle.

Growing RPO Provides Revenue Visibility

Remaining performance obligations (RPO), a key indicator of future revenue, continued to expand. Total RPO increased 36% YOY to $18.4 billion. Even excluding acquisitions, RPO grew 22%, while current RPO accelerated to 17% growth from 15% in the previous quarter. The expanding backlog indicates customers are making longer-term commitments to Palo Alto's platform, improving future revenue visibility.

Management Expects Momentum to Continue

Management expects strong growth to continue. For the fourth quarter of fiscal 2026, Palo Alto projects revenue of approximately $3.35 billion, representing about 32% YOY growth. NGS ARR is expected to reach between $8.9 billion and $8.95 billion, up 59% to 60%.

Can the Rally Continue?

Although Palo Alto's 107% rally has raised valuation concerns, its recurring revenue continues to grow rapidly, platform adoption is strengthening customer relationships, and AI security is emerging as a significant growth driver.

As enterprises consolidate cybersecurity vendors while expanding AI deployments, Palo Alto Networks appears well-positioned to deliver solid growth, which will support further gains in its stock price.

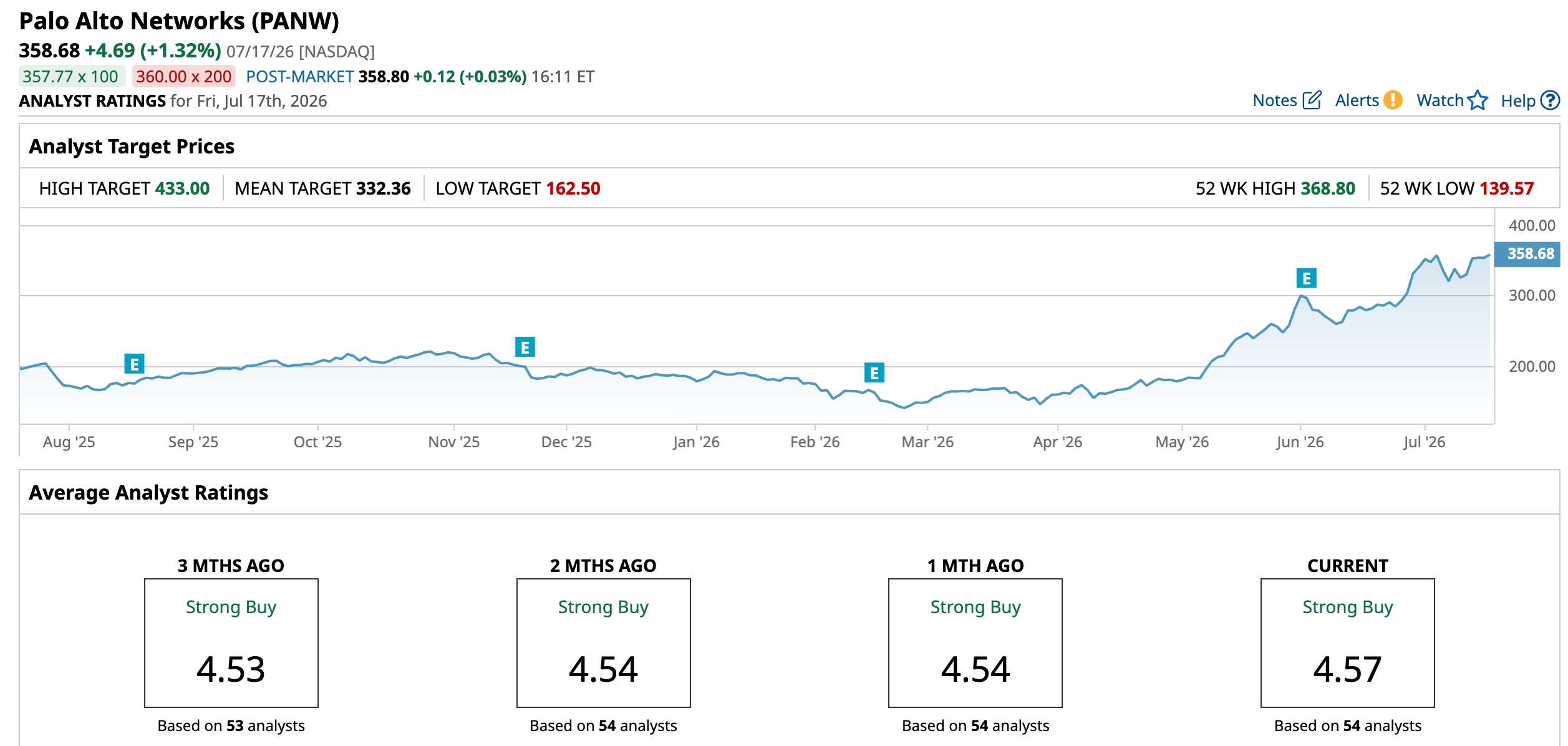

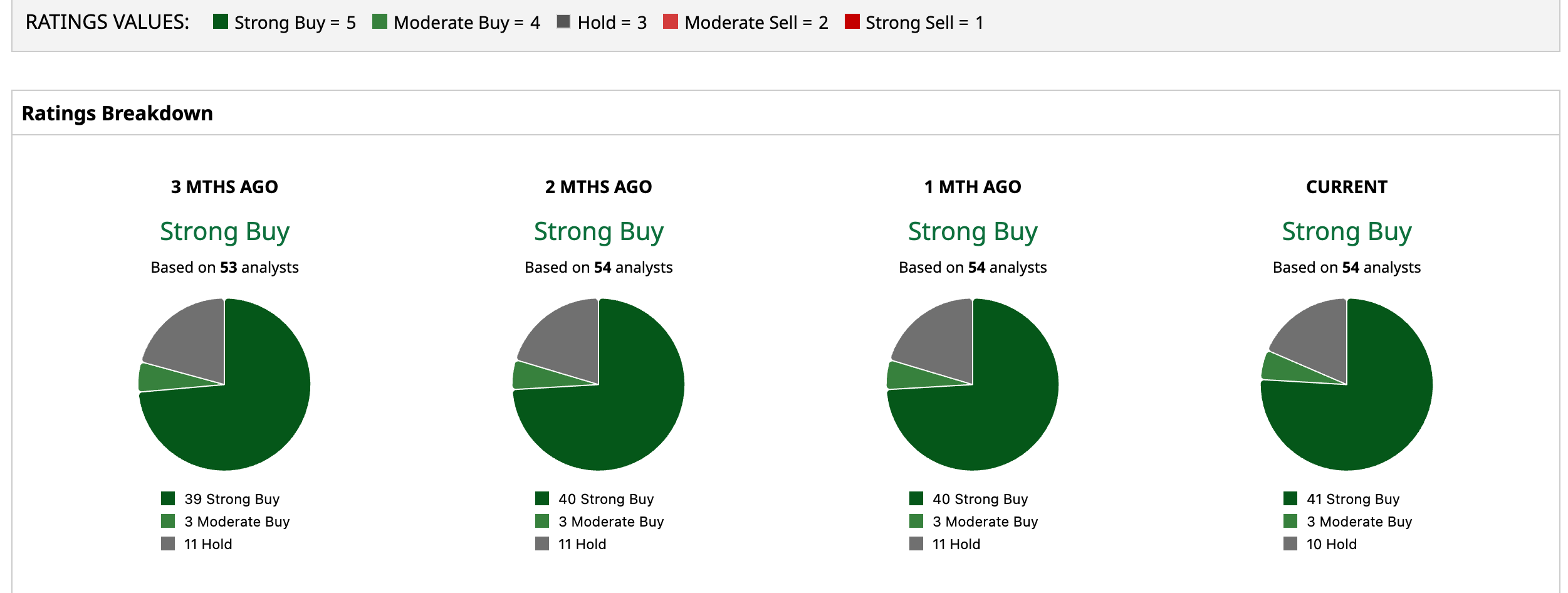

Analysts remain optimistic, with Wall Street maintaining a “Strong Buy” consensus rating on the shares.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)