/Pfizer%20Inc_%20logo%20sign-by%20JHVEPhoto%20via%20iStock.jpg)

Pfizer (PFE), a global pharmaceutical giant that was once a pandemic darling, is now facing turbulence. Following a period of extraordinary vaccine-driven revenue, the company now faces a more sobering reality. Declining pandemic-related sales and increased competition in key therapeutic areas have raised investor concerns about the company’s future.

Pfizer stock has fallen 15.5% in the last year. Investors are now wondering whether Pfizer’s ambitious cost-cutting initiatives and new pipeline drugs will revive the company’s declining stock price.

A Solid Financial Foundation, Despite the Headwinds

In the first quarter of 2025, Pfizer reported revenues of $13.7 billion, down 8% year-over-year. This decline stemmed from an expected drop in Paxlovid sales, as well as changes in U.S. Medicare Part D under the Inflation Reduction Act (IRA). Management emphasized that the decline in legacy blockbusters such as Paxlovid, Eliquis, Xeljanz, and Ibrance was offset by growth in products such as Vyndaqel, Comirnaty, Padcev, Nurtec, and Lorbrena.

However, the company’s bottom line showed encouraging growth. Adjusted diluted earnings per share (EPS) were $0.92, exceeding consensus expectations and representing a 12% from the prior-year period. This increase was driven by higher gross margins, tighter cost controls, and favorable tax resolutions. The adjusted gross margin increased to 81%, reflecting Pfizer’s improved product mix and reduced royalty obligations.

During the Q1 earnings call, Pfizer CEO Albert Bourla emphasized the company’s ongoing transformation and discipline across all operations. He emphasized concentrating less on underperforming assets and more on late-stage, high-potential assets in oncology, vaccines, inflammation and immunology (I&I), and internal medicine. In April, Pfizer discontinued danuglipron, an obesity drug in its internal pipeline. While the decision appeared to be a setback for investors, it reflects Pfizer’s renewed willingness to cut losses early and redirect efforts.

Importantly, Pfizer anticipates total net savings of $7.7 billion by 2027, which it intends to reinvest in pipeline development. This includes at least $4.5 billion in total net cost savings by the end of 2025. These new savings will be primarily achieved through the use of automation, artificial intelligence (AI), and digital business process simplification. These savings could help boost both earnings growth and investment in innovation.

A Pivotal Pipeline in Focus

While cost cuts have temporarily stabilized margins, investor sentiment ultimately depends on Pfizer’s pipeline development.

The company has around 108 clinical programs underway. 2025 is shaping up to be a turning point for pipeline milestones, with at least four regulatory decisions and up to nine Phase 3 readouts. While its pipeline includes several disease areas, oncology stands out as the most immediate and significant growth driver.

One notable candidate is sasanlimab, which is being tested in non-muscle invasive bladder cancer (NMIBC). The Phase 3 CREST trial results were positive, indicating promise in a field where treatment has not advanced in over 30 years. Padcev, a key component of Pfizer’s oncology portfolio, is another critical asset. Along with Merck’s (MRK) pembrolizumab, it is currently the most commonly prescribed first-line treatment for locally advanced/metastatic urothelial cancer in the U.S.

Additionally, Elrexfio is a therapy for relapsed/refractory multiple myeloma. A Phase 3 readout is expected this year, which could lead to a significantly larger patient pool and longer treatment durations. Pfizer’s antibody-drug conjugates (ADCs), specifically PDL1 vedotin and sigvotatug vedotin (SV), are arguably the company’s most promising candidates. Both are intended to treat non-small cell lung cancer (NSCLC), the world’s most common and lethal cancer. If successful, these best-in-class ADCs could change the global standard of care in this critical area.

Vaccines are another area of strategic investment. Pfizer hopes that its fourth- and fifth-generation pneumococcal conjugate vaccines (PCVs) will solidify its leadership in pneumococcal prevention.

Despite recent revenue struggles, Pfizer continues to prioritize long-term shareholder value, proving its worth as a defensive dividend stock. In the first quarter, it returned $2.4 billion to shareholders through dividends. It offers an appealing yield of 7%, which is significantly higher than the healthcare average of 1.6%.

What Does Wall Street Say About Pfizer Stock?

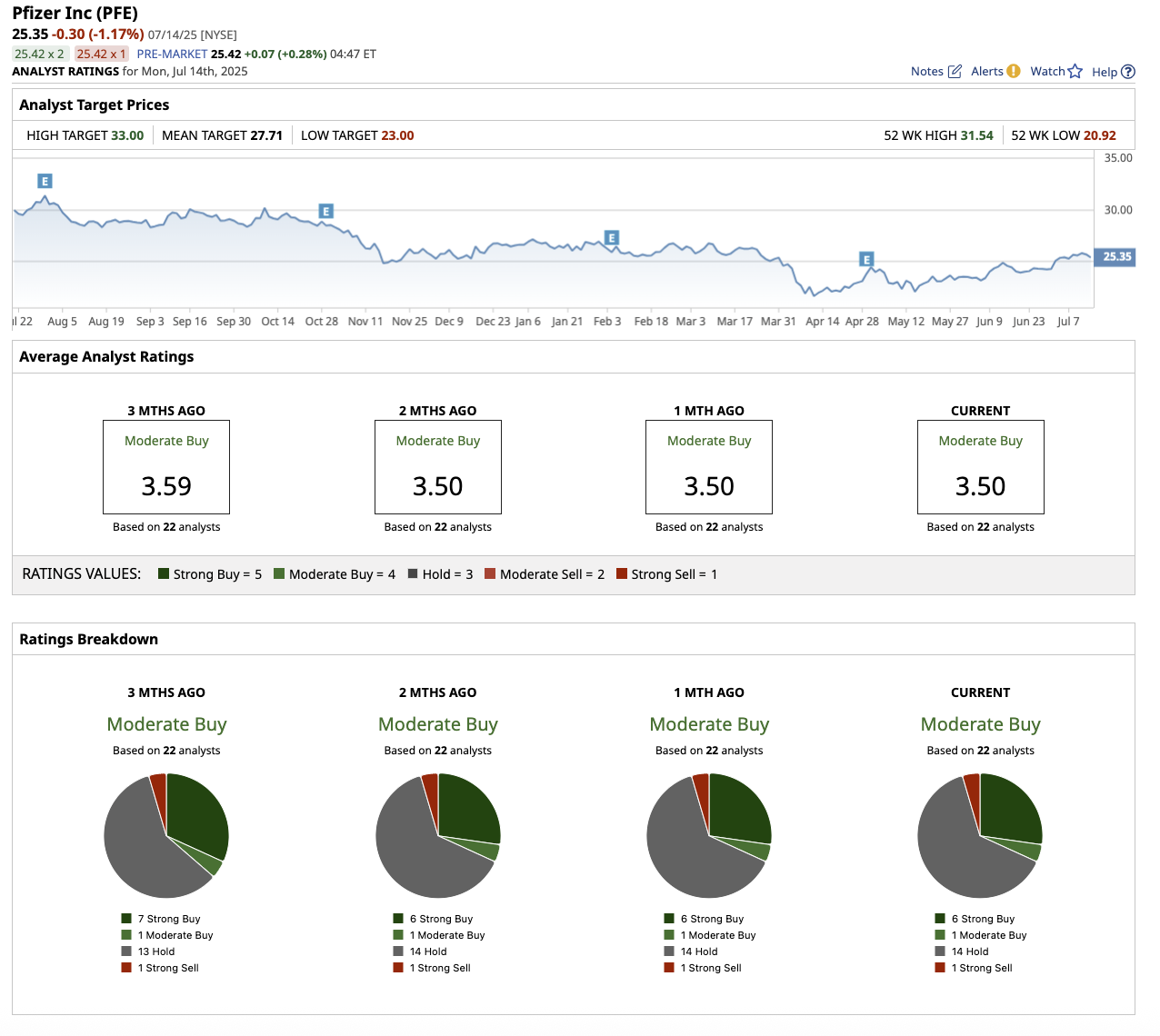

On Wall Street, Pfizer stock is rated a “Moderate Buy.” Out of the 22 analysts who cover PFE stock, six rate it a “Strong Buy,” one says it is a “Moderate Buy,” 14 rate it a “Hold," and one suggests a “Strong Sell.” Its average price target of $27.71 suggests that the stock can increase by 12.7% over current levels. However, its high target price of $33 implies upside potential of 34% over the next 12 months.

The Bottom Line on Pfizer Stock

Pfizer is clearly at a crossroads. With the COVID-19 tailwinds gone, the company must now show that it can reinvent itself as a leaner, innovation-driven pharma powerhouse. Its cost-cutting strategy is working well, and it has laid the groundwork for the next phase of growth, particularly in oncology, vaccines, and internal medicine. However, Pfizer’s stock revival will depend on whether the maturing pipeline can generate significant new revenue streams.

Investors with patience and a long-term outlook may find Pfizer’s reset an appealing entry point, with its stock trading 22% lower than its 52-week high of $31.54. However, for risk-averse investors, Pfizer remains a biotech stock to watch from the sidelines.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/Facebook-you've%20been%20Zucked%20by%20Annie%20Spratt%20via%20Unsplash.jpg)

/NVIDIA%20Corp%20logo%20on%20phone-by%20Evolf%20via%20Shutterstock.jpg)