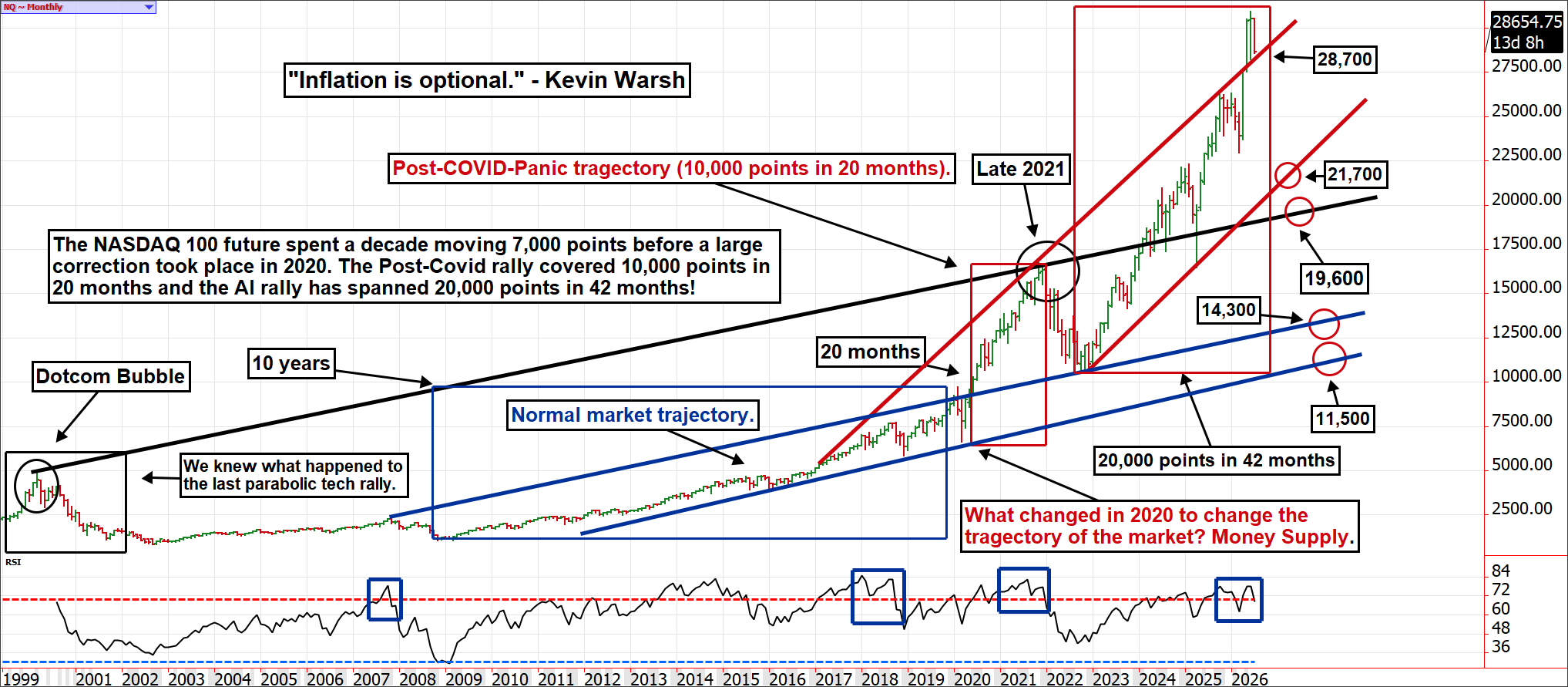

Perhaps the single most important statement made all year was delivered by the new Federal Reserve Chairman, Kevin Warsh. Earlier this week, during a Congressional testimony, he said plainly and simply, “Inflation is a choice.” The new Fed Chair is the first to say out loud that the inflation problems we are experiencing today are the direct result of too much liquidity in the system. Those of us who have been around for a while remember the onset of Quantitative Easing (QE) programs to combat the Global Financial Crisis. These programs involve the government buying its own Treasury debt and were intended to be temporary. QE is designed to add liquidity to the system and keep asset prices afloat, in hopes that the wealth effect would encourage economic activity.

Perhaps the single most important statement made all year was delivered by the new Federal Reserve Chairman, Kevin Warsh. Earlier this week, during a Congressional testimony, he said plainly and simply, “Inflation is a choice.” The new Fed Chair is the first to say out loud that the inflation problems we are experiencing today are the direct result of too much liquidity in the system. Those of us who have been around for a while remember the onset of Quantitative Easing (QE) programs to combat the Global Financial Crisis. These programs involve the government buying its own Treasury debt and were intended to be temporary. QE is designed to add liquidity to the system and keep asset prices afloat, in hopes that the wealth effect would encourage economic activity.

It worked too well because we have been addicted to it ever since. In fact, our central bankers and politicians went back to the well in a bigger fashion in 2020 and 2021 to thwart the economic impact of pandemic shutdowns. We have yet to learn whether Warsh is just jawboning or serious; if he puts his money where his mouth is, the landscape has changed dramatically. It removes the punch bowl that has buoyed asset prices beyond reasonable levels and avoided economic recessions. Specifically, less money sloshing around in the economy means more headwinds for stocks and commodities. For instance, without the 40% increase in money supply between 2020 and 2021, would vendors on the Las Vegas Strip find demand for a single latte priced at $20 or a sharable tomahawk steak for just under $1,000? Probably not. Scott Shellady and I spoke about this on Cow Guy Close; click here to watch the archive.

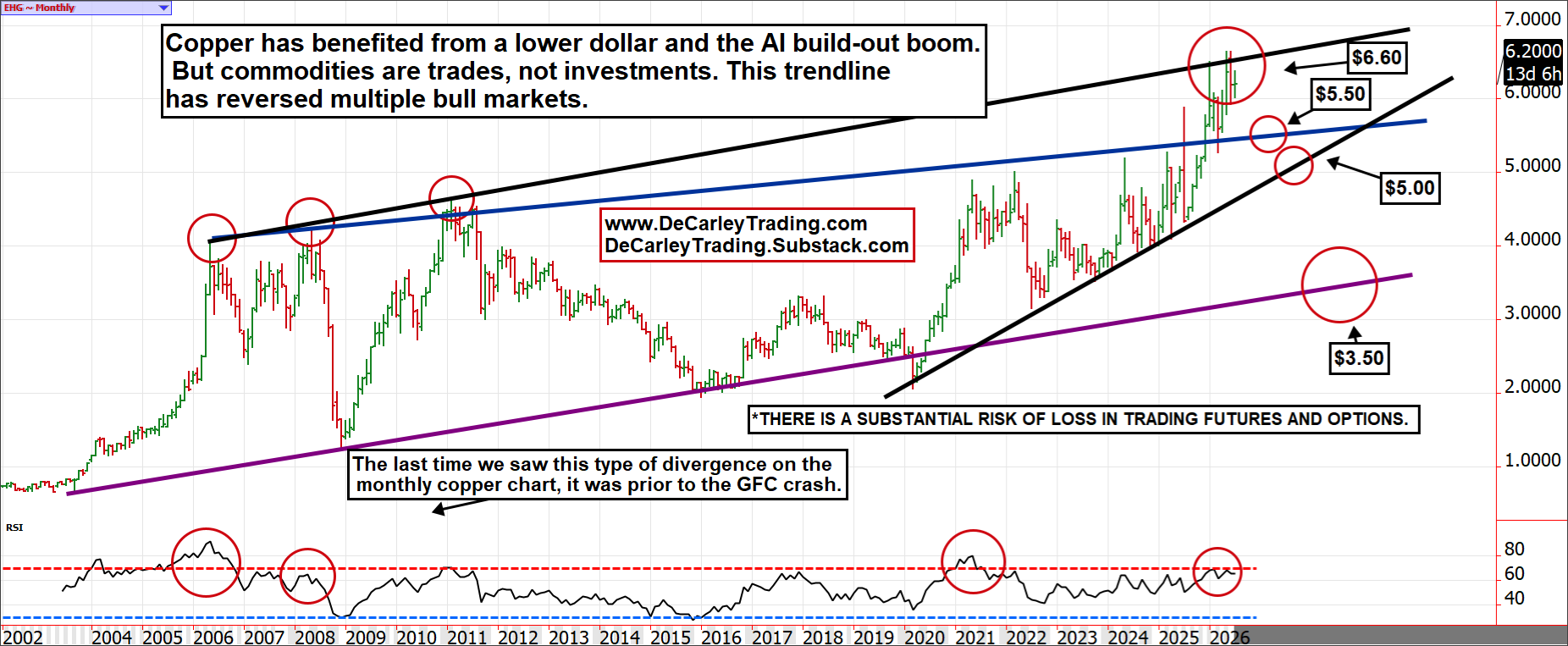

It is no coincidence that gold and silver peaked earlier this year, precisely when Kevin Warsh was announced as the next nominee for Fed Chair. It didn’t take long for those markets to recognize the writing on the wall. However, the unwinding of the debasement trade would also include selling assets that have yet to acknowledge the risk of a reduction in the Fed's balance sheet (i.e., a smaller money supply), such as stocks, copper, coffee, and cattle.

Let’s look at some charts. These charts aren’t intended to be sell signals, but rather a reality check into the big picture in assets that have, thus far, avoided the same type of reality check that gold, silver, crypto, grains, and energies have succumbed to.

Despite bullish fundamental narratives dominating stock market price action, such as the so-called AI revolution and earnings acceleration. It is hard to argue against the idea that the massive bull market we have seen since 2020 has been largely supported by monetary policy and the expansion of the money supply. At its core, inflation is too much money chasing too few assets, and that is exactly what this NASDAQ 100 chart reflects. If central bankers are willing to normalize our economy by draining excess cash from the system, the equity market would need to trade sideways for a few decades for reality to catch up. Or we would need to see a massive repricing that might leave the NASDAQ under 20,000. We saw a similar, but smaller, double top in the RSI prior to the 2022/2023 correction of 35+%.

We haven’t seen a diverging double top in copper since the Global Financial Crisis. At the time, the copper market fell from $4.20 to $1.20 in a handful of months! The same trendline that rejected the pre-GFC rally in the summer of 2008 seems to have rejected the current rally near $6.60. If we repeated the pattern, copper would take a nearly 50% haircut to the purple trendline near $3.50…gulp. We don’t think this is out of the question, so it should be recognized that the risk of being long copper far outweighs the benefits of being long copper.

Next up is coffee; a product produced in countries without proper reporting resources or requirements. Further, it is often difficult to trust the data agencies report. It wasn’t that long ago that we were being spoon-fed distorted fundamental data in cocoa to artificially propel prices to astronomical levels. All we can do in coffee is focus on the current price action and what history has taught us.

The chart shows a clear market reaction at 250.00 (250 cents per pound). Above 250.00, bull markets become ultra-bulls, and below this level, we tend to see bull markets die and bear markets emerge. The current rally has been stunning. In fact, coffee saw the largest single-session rally in history earlier this month. This type of volatility shakes the core of market participants, triggering ongoing volatility that takes time to work off. However, we aren’t necessarily convinced that this revives the bull market. Instead, if prices hold below 350/360, we suspect prices continue to work their way lower. Again, despite challenging harvest and planting weather, demand destruction is a wild card that could render supply concerns obsolete. Should prices drop below 250.00, we would anticipate a sharp meltdown toward the trendline near 200.00, and eventually, we believe, a full round trip into the 100.00 handle is probable.

Lastly, in hindsight, it is easy to see the last two substantial cattle bull markets have been on the heels of massive government stimulus programs. The first began in 2009, just after our elected leaders passed a massive stimulus package and the Federal Reserve initiated a Quantitative Easing program to inject liquidity into the economy. The second came in 2020 following an even bigger series of stimulus packages and more aggressive money printing. The first rolled over after five years; has this rolled over in the sixth year?

There is a substantial risk of loss in trading futures and options.

These recommendations are a solicitation for entering into derivatives transactions. All known news and events have already been factored into the price of the underlying derivatives discussed. From time to time persons affiliated with Zaner, or its associated companies, may have positions in recommended and other derivatives.

There are no guarantees in speculation; most people lose money trading commodities. Past performance is not indicative of future results. Seasonality is already factored into current prices, any references to such does not infer certainty in future price action

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)