/IBM%20offices_%20Modern%20corporate%20building%20sign%20with%20a%20company%20logo%20By%20Nuria.jpeg)

International Business Machines (IBM) is leaning hard into the idea that the future of artificial intelligence won’t live solely in the public cloud. In its latest move, the company has unveiled a new class of on‑premise servers aimed at enterprises that want to run AI workloads locally. Strategically, this is exactly the way IBM wants to differentiate itself.

The timing makes this even more interesting. Just days before the announcement gained traction, IBM released preliminary Q2 2026 results that fell short of Wall Street expectations.

Its revenue reached $17.2 billion, and adjusted EPS hit $2.93, missing consensus estimates of $17.86 billion and $3.02 per share. This led to the stock suffering its worst single-day decline in decades, dropping over 25%.

But with a new on‑premise AI server now in the mix, the key question becomes more pointed. Is this new on-premise server a meaningful catalyst that could strengthen IBM’s competitive edge and support its stock performance?

IBM’s Recent Numbers

IBM is a global tech and consulting firm based in Armonk, New York, built around hybrid cloud, AI‑ready infrastructure, and mission‑critical systems for large enterprises, with a market value sitting near $198.5 billion.

The stock is down 26% year-to-date and 22.2% over the past 52 weeks.

On the numbers, IBM does not look expensive in every respect, with a forward price-to-earnings GAAP ratio of 22.73 times versus a sector median of 32.59 times, and a price‑to‑sales ratio of 2.79 times against the sector’s 3.31 times.

The stock still pays a forward annual dividend of $6.76 and yields 3.11%, which remains part of its appeal.

However, the March 2026 results show an uneasy market. Sales were about $15.9 billion, a decline of 19.15% year-over-year (YOY), which indicates the top line is shrinking rather than growing. Net income was roughly $1.2 billion, with net income growth at -78.29%.

At the same time, IBM has been clearing the near‑term earnings bar. The quarter ending March 2026 delivered EPS of $1.91 against a $1.81 estimate, a 5.52% beat. The balance sheet is not standing still either. Total assets in March 2026 were $156.2 billion, up 2.86%, which points to continued investment and expansion.

But the strain really appears in the cash flow picture. Operating cash flow was $5.2 billion, down 60.82%, while net cash flow was roughly -$2.8 billion, a swing of -434.04%. That kind of drop signals heavy cash use for investment, working capital, or other outlays.

IBM’s Local AI Build‑Out

IBM’s new Power S1112 server is a clear answer to one trend as more companies want AI to run on their own turf, not just in the cloud. It is an entry-level, single socket Power11 machine built for smaller, tighter setups.

The server is tuned for faster local inferencing using on-chip Matrix Math Acceleration. That lets enterprises process AI workloads closer to their data, with more control over security, while still keeping the option to plug into a wider hybrid environment.

On the software side, IBM is trying to make it easier for big customers to move old systems into the AI era. It is rolling out multi-agent tools and focused modernization workflows that help teams update legacy applications and weave in AI features without rebuilding everything from scratch.

IBM is also updating its mainstay infrastructure. New compact z17 and LinuxONE systems are aimed at organizations that struggle with space, power, and cost constraints in their data centers. These machines are designed to handle heavy, always-on workloads but in a smaller footprint.

All of this is happening while clients are shifting how they spend.

Cautious Optimism Around IBM’s Local AI Story

IBM is heading into a big checkpoint with its next earnings report, set for July 22, after the close. The Street is looking for EPS of $3.01 for the June quarter, up from $2.80 a year earlier. That works out to roughly 7.5% growth and sets a clear bar for the company after the recent warning.

On the analyst side, the picture is mixed but still positive. Bank of America has pulled back a bit, trimming its target from $330 to $280, yet it still tells clients to buy, which shows it views the sell-off as overdone rather than a permanent break in the story.

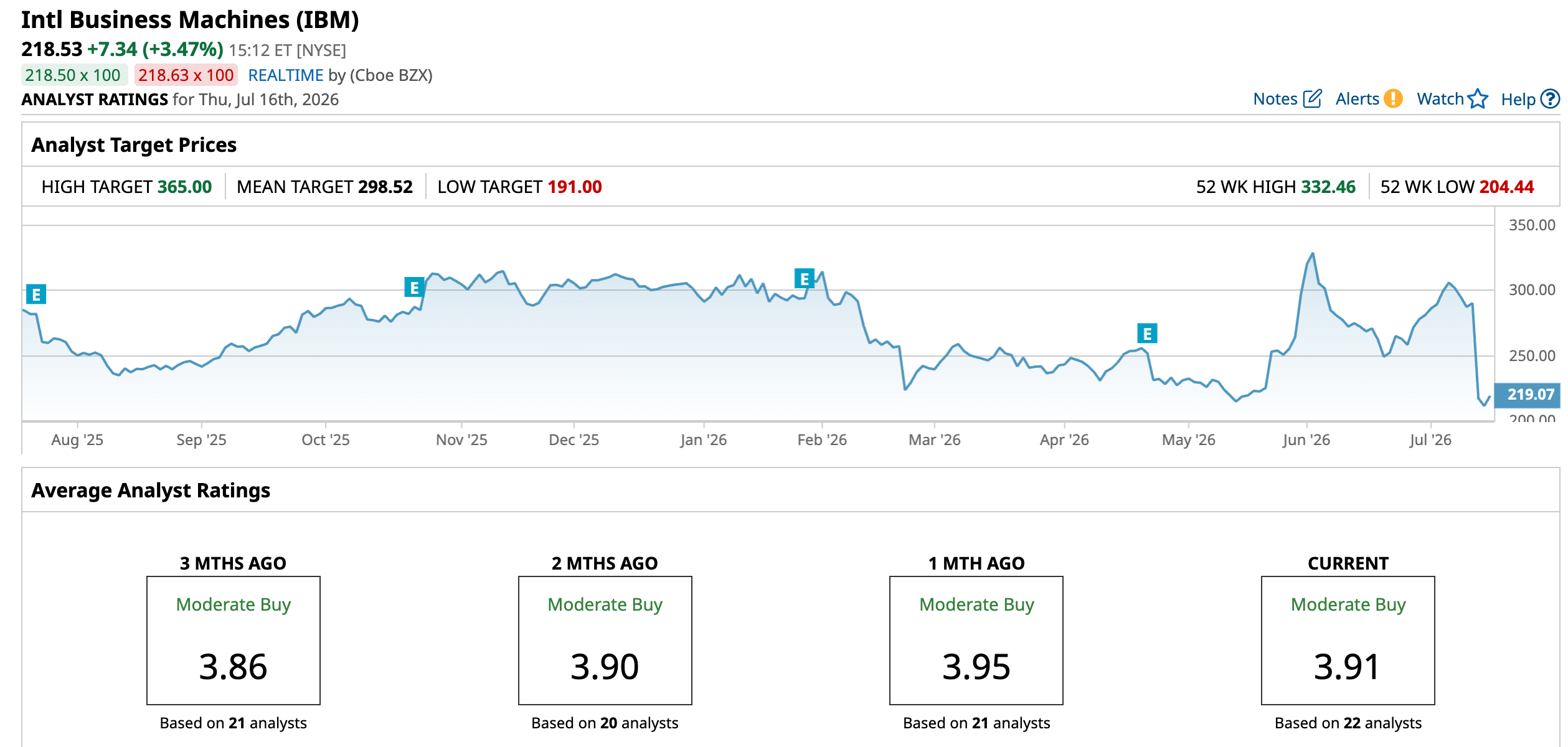

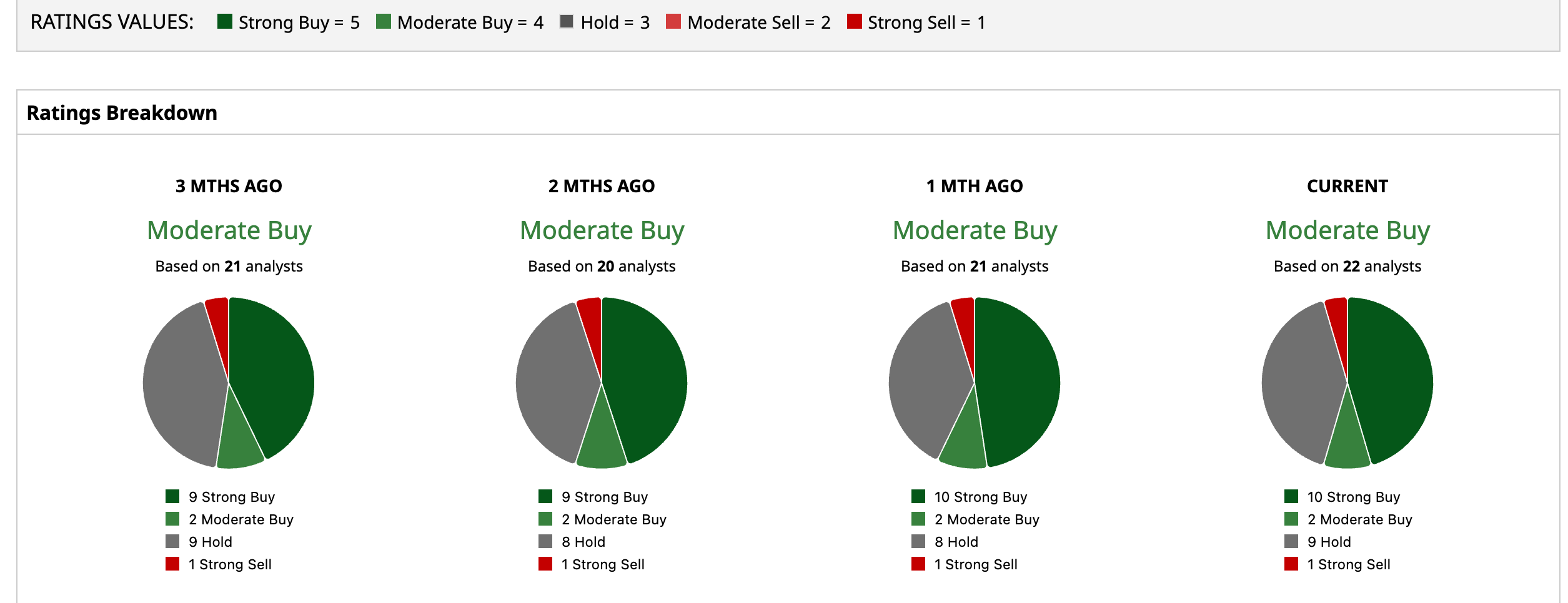

Zooming out, sentiment remains cautiously constructive. Across 22 analysts, the consensus rating is “Moderate Buy.” Their average price target sits at $298.52, implying about 36.6% upside.

Conclusion

Right now, this new on‑premise AI server looks like a solid building block for IBM rather than a big swing that instantly changes the stock story. It fits neatly into a clear plan to serve companies that want AI close to their own data and systems. It should help earnings and cash flow slowly over time, not in one big jump. Given that, the shares seem more likely to edge higher alongside mid-single-digit growth than suddenly shoot up on this one product alone.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)