/Women%20sitting%20on%20roling%20chair%20in%20front%20of%20computer%20monitors%20by%20ThisisEngineering%20via%20Unsplash.jpg)

Shares of cybersecurity giant Palo Alto Networks (PANW) ended more than 1% higher in yesterday's trading session after Citi reiterated its “Buy” rating on the stock with a price target of $400, a possible upside of 21% from current levels. PANW stock is doing even better today as it is up over 6% in afternoon trading.

Sounding out that it's Idira unit, or what was formerly known as CyberArk, might see improvement in margins, Citi further said, “Net-net, while profitability expansion has near-term hurdles relative to peak 50x NTM EV/FCF/80x NTM P/E (~20/30-turn premium to 5-year median), IR’s constructive tone on core business trends—validated by our early checks and recent CIO survey readthroughs—and our positively-skewing new organic NNARR sensitivity analysis (extrapolating recent platformization trends, assessing NNARR bridge by-segment) give us confidence revs/NGS ARR could see steady positive revisions and power med-term operating leverage."

About Palo Alto

Founded in 2005, Palo Alto Networks is one of the world's largest pure-play cybersecurity companies and has evolved from a next-generation firewall pioneer into a broad, AI-powered cybersecurity platform company. Today, it competes across network security, cloud security, security operations, identity security, and AI security. Its customer base includes more than 70,000 organizations across over 150 countries, including 85 of the Fortune 100.

Valued at a market cap of $265.6 billion, PANW stock is up a very healthy 91% on a year-to-date (YTD) basis.

However, can PANW live up to Citi's billing and continue to grow? I think it can, and here's why.

Giving Cybersecurity a Platform

The global cybersecurity market is already huge at $248.3 billion in 2026 and is forecasted to reach about $700 billion by 2034. And Palo Alto, with a market share of 16%, sits right at the top.

Notably, Palo Alto's shrewd acquisitions and, more importantly, its strategic focus on becoming an end-to-end enterprise security platform have been the core drivers of its growth.

However, the company did not reach here by chance. Rather, it was slow and deliberate. It began by protecting networks with next-generation firewalls, expanded into cloud and security operations, and has now added identity security and observability.

Now, in the age of AI, just combating known actors will not suffice. AI agents can go rogue and must be kept in check.

Here, Cortex XSIAM, Palo Alto’s security operations platform, answers this by fighting machines with machines. Rather than the old model of piling logs into a SIEM and waiting for tired analysts to chase alerts, XSIAM ingests data at a petabyte scale and applies AI to detect, investigate, and remediate largely on its own.

Notably, the XSIAM 3.5 pushed this toward what the company calls an agentic SOC. Its Autonomous Playbooks now analyze and shut down known threats without waiting for a human, while Agentic Response spins up AI agents that build multistep investigation plans and act in real time, with human approval kept in the loop for sensitive moves.

This differentiates XSIAM from the competition, which offers SIEM, XDR, SOAR, and attack surface tools separately, whereas XSIAM folds all of them into one AI-driven platform. Palo Alto backs this with real numbers, noting Enhanced Application Log ingestion now cuts the cost of pulling firewall and SASE data into XSIAM by roughly 10 to 15 percent, at no extra charge.

Thus, for enterprises drowning in tools and alerts, this unified, autonomous approach is the draw, and it is reflected in the 70,000-plus customers Palo Alto now serves.

Acquisitions have also played a critical role in the company's recent growth, and two of the most material ones have been of CyberArk and Chronosphere. Both acquisitions extend Palo Alto into ground it did not previously own, and both are framed squarely around securing the AI era.

CyberArk, which Palo Alto acquired for roughly $25 billion, hands the company the leading identity security platform, something it genuinely lacked before. Notably, CyberArk lets Palo Alto secure every identity, whether human, machine, or the multiplying AI agents, by extending privileged access controls beyond a narrow set of admins to the whole enterprise. On the other hand, Chronosphere, completed in January 2026 for about $3.35 billion, offers something different: observability. This is the discipline of monitoring the health, performance, and behavior of modern cloud-native applications at a massive scale.

Chronosphere lets customers achieve more in-depth visibility across both security and observability data at a petabyte scale from a single lens, which is increasingly valuable as sprawling AI workloads generate enormous volumes of operational data.

Solid Q3

Palo Alto's market-leading position has been reflected in its numbers, as Q3 saw the company reporting a beat on both revenue and earnings.

Revenues for the quarter came in at $3 billion, a growth of 31% from the previous year. Remaining performance obligations, a key indicator of future demand, witnessed a rise too. The figure saw an uptick of 36% from the previous year to $18.4 billion.

However, earnings moved up by just 6.3% in the same period to $0.85 per share, coming in ahead of the consensus estimate of $0.79 per share. This was the ninth consecutive quarter of earnings beat from the company.

For Q4 2026, Palo Alto expects revenue to be between $3.345 billion and $3.355 billion, while the same for earnings is forecasted to range between $0.96 and $0.98 per share. Analysts are forecasting revenues of $3.35 billion and EPS of $0.98 per share in Q4 for the company.

Coming back to Q3, Next-Generation Security ARR, the component intended to show the scale and growth of Palo Alto's newer subscription-based security businesses beyond its traditional hardware firewall franchise, came in at $8.1 billion. This marked an annual growth of 60%.

The cash flow figures also improved from the prior year to $871 million (vs. $628 million earlier), with free cash flow coming in even better at $910 million. Overall, Palo Alto ended Q3 2026 with a cash balance of $2.4 billion, with short-term debt of just $160 million.

However, as is the case with many hot tech stocks, PANW is trading at overvalued levels. Its forward P/E, P/S, and P/CF of 160.59, 28.80, and 108.80 are all considerably above the sector medians of 25.05, 3.41, and 19.03, respectively.

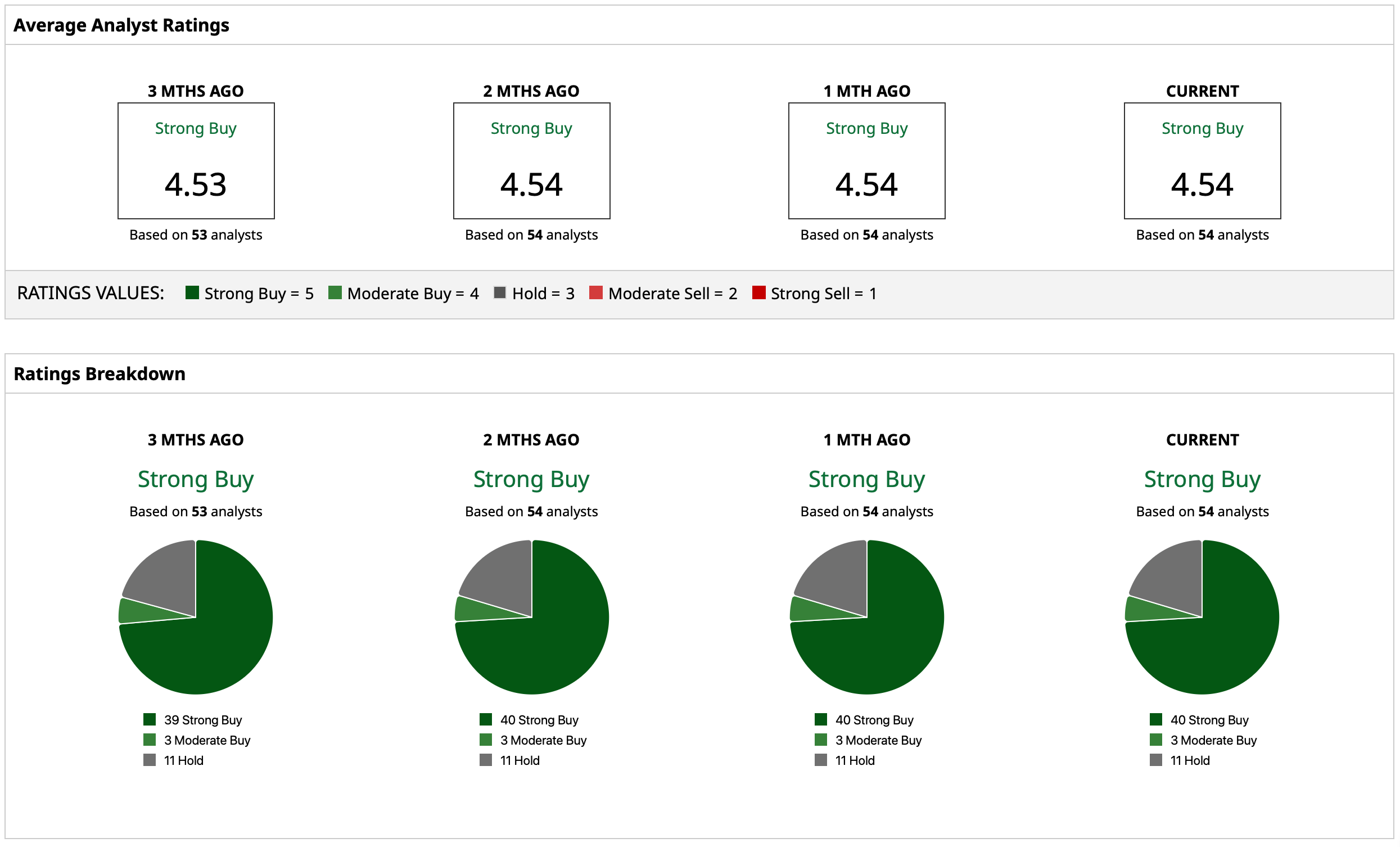

Analyst Opinion on PANW Stock

Overall, analysts have deemed PANW stock to be a consensus “Strong Buy,” with a mean target price that has already been surpassed. The high target price of $433 indicates an upside potential of about 24% from current levels. Out of 54 analysts covering the stock, 40 have a “Strong Buy” rating, three have a “Moderate Buy” rating, and 11 have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.