NiSource Inc. NI continues to benefit from its strategic investment plans to modernize infrastructure. This helps the company to improve service reliability. NI continues to add clean assets to its portfolio, which helps boost its overall performance. Given its growth opportunities, NiSource makes for a solid investment option in the utility sector.

Let’s focus on the factors that make this Zacks Rank #2 (Buy) company a strong investment pick at the moment.

NI’s Growth Projections & Surprise History

The Zacks Consensus Estimate for 2025 earnings per share (EPS) has increased 0.5% to $1.88 in the past 30 days.

The Zacks Consensus Estimate for 2025 sales is pinned at $5.99 billion, indicating a year-over-year increase of 9.8%.

NiSource’s long-term (three to five years) earnings growth rate is 7.88%. The company delivered a trailing four-quarter average earnings surprise of 24%.

NI’s Dividend Growth

The company has been consistently increasing the value of its shareholders through dividends. It expects to deliver a 9-11% annual return over the long term. Currently, NiSource’s quarterly dividend is 28 cents per share. This represents an annualized dividend of $1.12 per share, up 6% from the previous level. The company expects a targeted annual dividend payout ratio of 60-70%. Its current dividend yield is 2.87%, better than the Zacks S&P 500 composite's average of 1.27%.

Debt Position of NI

Currently, NiSource’s total debt to capital is 57.63%, better than the industry’s average of 59.34%.

The time-to-interest earned ratio at the end of the first quarter of 2025 was 3.2. The ratio, being greater than one, reflects the company’s ability to meet future interest obligations without difficulties.

NI Gains From Its Focus on Investments

NiSource is working on a long-term utility infrastructure modernization program. The company made capital investments worth $3.3 billion in 2024. It expects investments in the range of $4-$4.3 billion for 2025. It also projected an investment of $19.4 billion for the 2025-2029 period.

NI expects an annual rate base growth of 8-10% during 2025-2029, driven by its capital expenditures. The company’s planned regulated investments should improve the reliability and safety of its services and provide efficient electric and natural gas services to its increasing customer base. More than 75% of NiSource’s capital expenditure starts providing returns in less than 18 months of investment.

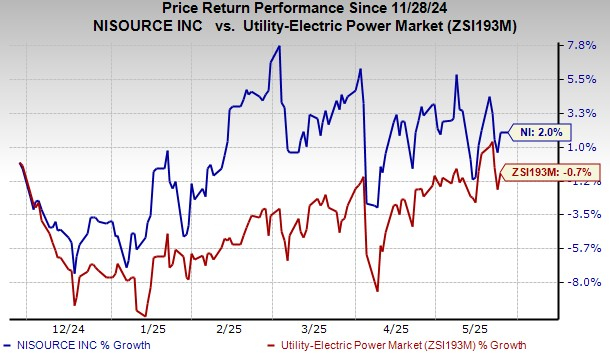

NI’s Share Price Performance

In the past six months, the stock has returned 2% against the industry’s decline of 0.7%.

Image Source: Zacks Investment Research

Other Stocks to Consider

A few other top-ranked stocks from the same industry are Evergy EVRG, Exelon Corporation EXC and WEC Energy Group WEC, each carrying a Zacks Rank #2 at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

EVRG’s long-term earnings growth rate is 5.7%. The Zacks Consensus Estimate for 2025 EPS implies an improvement of 5.8% from the bottom line recorded in 2024.

EXC’s long-term earnings growth rate is 6.42%. The Zacks Consensus Estimate for 2025 EPS implies an improvement of 8% from the bottom line recorded in 2024.

WEC Energy’s long-term earnings growth rate is 6.95%. The Zacks Consensus Estimate for 2025 EPS indicates year-over-year growth of 8.5%.

Zacks Names #1 Semiconductor Stock

It's only 1/9,000th the size of NVIDIA which skyrocketed more than +800% since we recommended it. NVIDIA is still strong, but our new top chip stock has much more room to boom.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $803 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Exelon Corporation (EXC): Free Stock Analysis Report

NiSource, Inc (NI): Free Stock Analysis Report

WEC Energy Group, Inc. (WEC): Free Stock Analysis Report

Evergy Inc. (EVRG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)