Howdy market watchers!

Coming off of a stormy yet festive July 4th weekend in which our Republic celebrated being the oldest such experiment in history, there were plenty of fireworks in the markets, especially commodities, that extended celebrations until the end of the week.

Hotter than normal temperatures in the corn belt combined with more China buying of US soybeans and rumors that they could be in the market for US corn, sent futures surging on Monday with continuation into Tuesday. While the market then took a mid-week breather ahead of Friday’s monthly USDA Crop Production and World Ag Supply & Demand reports, the bulls were further fed to close out the week with little-to-no help from the crude oil market.

The biggest push on Friday was news that Russia’s reinstatement of its wheat export tax claiming that export prices reached levels above the upward threshold. This move will increase export prices that Russia essentially sets for the global market given they are the low-cost supplier. As reported, “the duty equals 70% of the difference between a government-set reference price and the indicative export price. As export prices climb above the threshold, the tax increases. When prices fall below it, the levy can drop to zero. Moscow says the mechanism is designed both to regulate exports and generate revenue to support domestic grain producers.” This comes right at the time that world wheat production and ending stocks are tightening.

Fresh data indicating a lower stocks-to-use ratio was released on Friday morning in USDA’s monthly grain reports. While new crop US wheat ending stocks came in at 722 million bushels, above the 710 million bushel expectations, they were still well below last month’s 744 million bushel estimate and last year’s 935 million bushels. US all-wheat class production also came in above expectations at 1.536 billion bushels versus 1.521 billion bushels anticipated, but still below prior estimates of 1.543 billion bushels and last year’s 1.985 billion bushels.

World wheat ending stocks came in at 272.8 million metric tons, below the expected 273.0 million MT that was already below last month’s 275.4 million MT as well as last year’s 279.0 million MT. The US hard red winter wheat crop, traded as Kansas City futures, was also lower than expected at 471 million bushels versus 476 million bushels expected that was already below last month’s 479 million bushels and last year’s 804 million bushels.

Similarly, the soft red winter wheat crop, traded as Chicago futures, came in at 287 million bushels versus the expected 293 million bushels that was below last month’s 300 million bushels and last year’s 353 million bushels. White wheat and other spring wheat contributed to the slight increase versus expectations.

September KC wheat futures reached my first target of $6.78 on Friday, trading as high as $6.84 1/2 and closing up 22 cents on the day at $6.76 ¼. My next target is $7.09.

December new crop corn futures also found bullish support from the USDA report putting in an outside day, lower low and higher high, on the chart and closing higher. Key moving averages are above with the 50-and-200 day moving averages crossing over at $4.66 and the 100-day moving average at $4.72. While these levels may bring some resistance to price action, there is potential to retest the $5.00 mark and even up to the $5.13 level.

Warmer weather has been supportive and will be important to feed the bulls, but there is still a large and quality crop out there with time and so we really need export demand to reach such levels, in my opinion.

China’s President Xi is scheduled to visit the US in September and that sets a timeline for at least some purchases ahead of that time with more deals likely to be cut during the visit with President Trump.

The USDA report also lent support however, with old crop corn ending stocks coming in at 2.02 billion bushels versus expectations for 2.074 billion bushels and below last month’s 2.145 billion bushels. This is though well above last year’s 1.551 billion bushels. New crop corn ending stocks came in at 1.790 billion bushels, below expectations at 1.865 billion bushels and USDA’s prior forecast of 1.960 billion bushels and last year’s monster 2.145 billion bushels.

There wasn’t much changed with new crop production with corn yields held the same at 183.0 bushels per acre (bpa). Total US corn production is pegged at 16.0 billion bushels.

Brazil corn production was kept unchanged at 138.0 million MT while a slight increase was expected. Argentine corn production was increased to 63.0 million MT, 2.0 million MT above last month. World ending stocks for corn were below expectations at 275.3 million MT versus 278.4 million MT guessed and below USDA’s prior 281.2 million MT and last year’s 298.7 million MT.

December corn futures closed 8.5 cents higher on Friday.

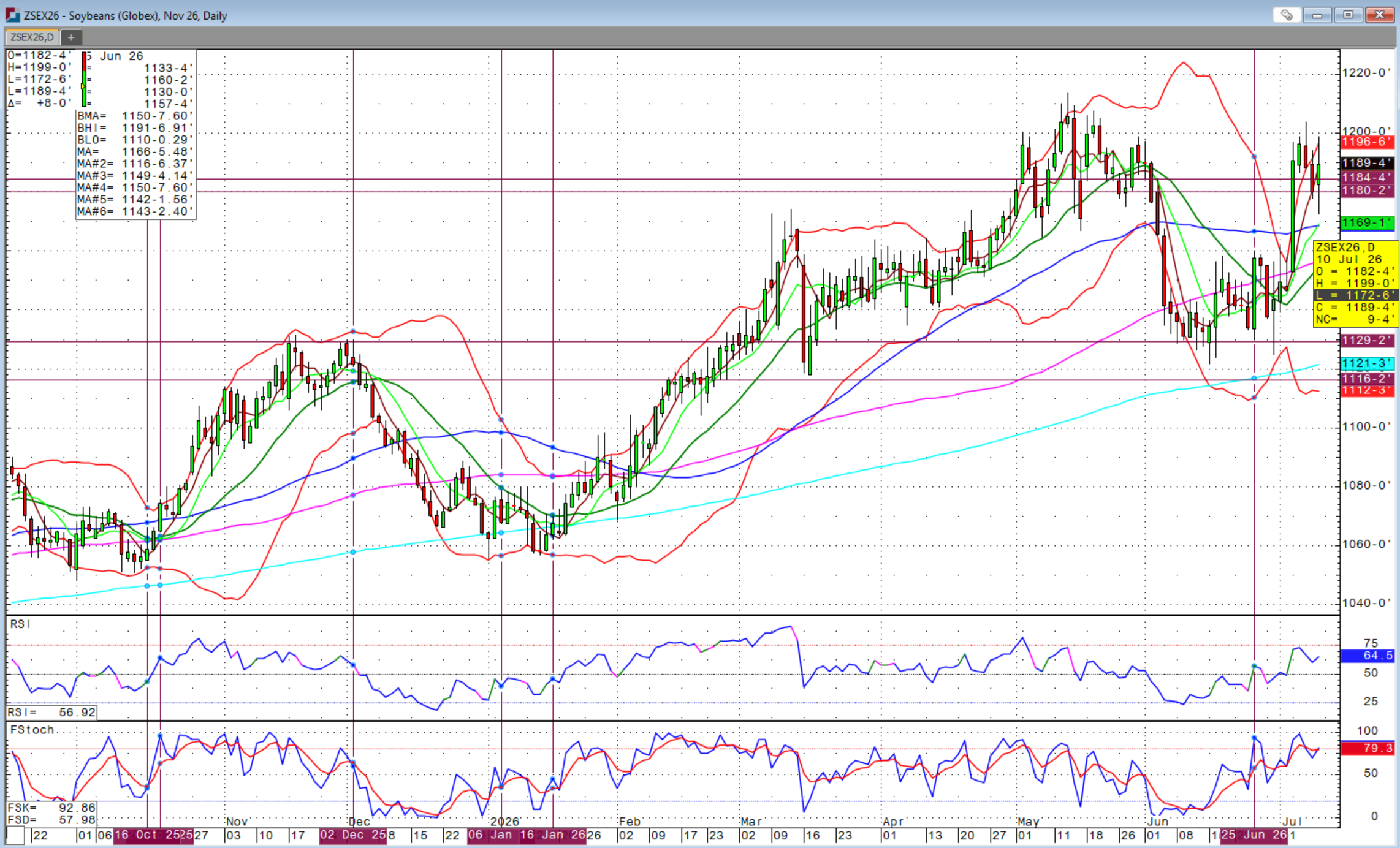

It was a similar story for soybeans with old crop and new crop US ending stocks tighter than expected. US soybean yields were unchanged at 53.0 bpa while production was increased on higher harvested acre forecasts. Soybeans futures are waning for direction, but also had an outside chart day, lower low and higher high, on Friday with a positive close that could suggest more upside to come.

Brazil soybean production was unchanged from last month at 180.0 million MT while a slight increase was expected. Argentine soybean production was also unchanged from last month and below last year’s production by 1.1 million MT. Global soybean ending stocks came in below expectations at 124.2 million MT versus 125.2 million MT, which was expected to be an increase versus last month.

Meanwhile, the US war in Iran has began to ramp back up and in a significant way at least through rhetoric. President Trump was at the NATO summit this week and used strong language towards Iran. There were attacks in both directions this week and talk of assassination threats on Trump. The rhetoric has escalated as the ceasefire is apparently off again with both countries headed towards a collision course while Russia’s Putin also is appearing in greater despair and increasing threats as a result.

We could see some war premium return to commodity markets although I was expecting more sustained support for crude oil this week. It was said this week that the world is beginning to figure out oil supply without Iran. That seems to be increasingly true, but is wild it could be factored in that quickly. Regardless, we will likely still see spikes on any news of major attacks especially if it directly impacts energy infrastructure. There is a chart gap on August crude oil that would fill at $81.68, which is $10 per barrel above the current price level.

Suffice it to say, we will likely see plenty of volatility and action between now and China’s President visiting the US, which is also just ahead of the Mid-term elections.

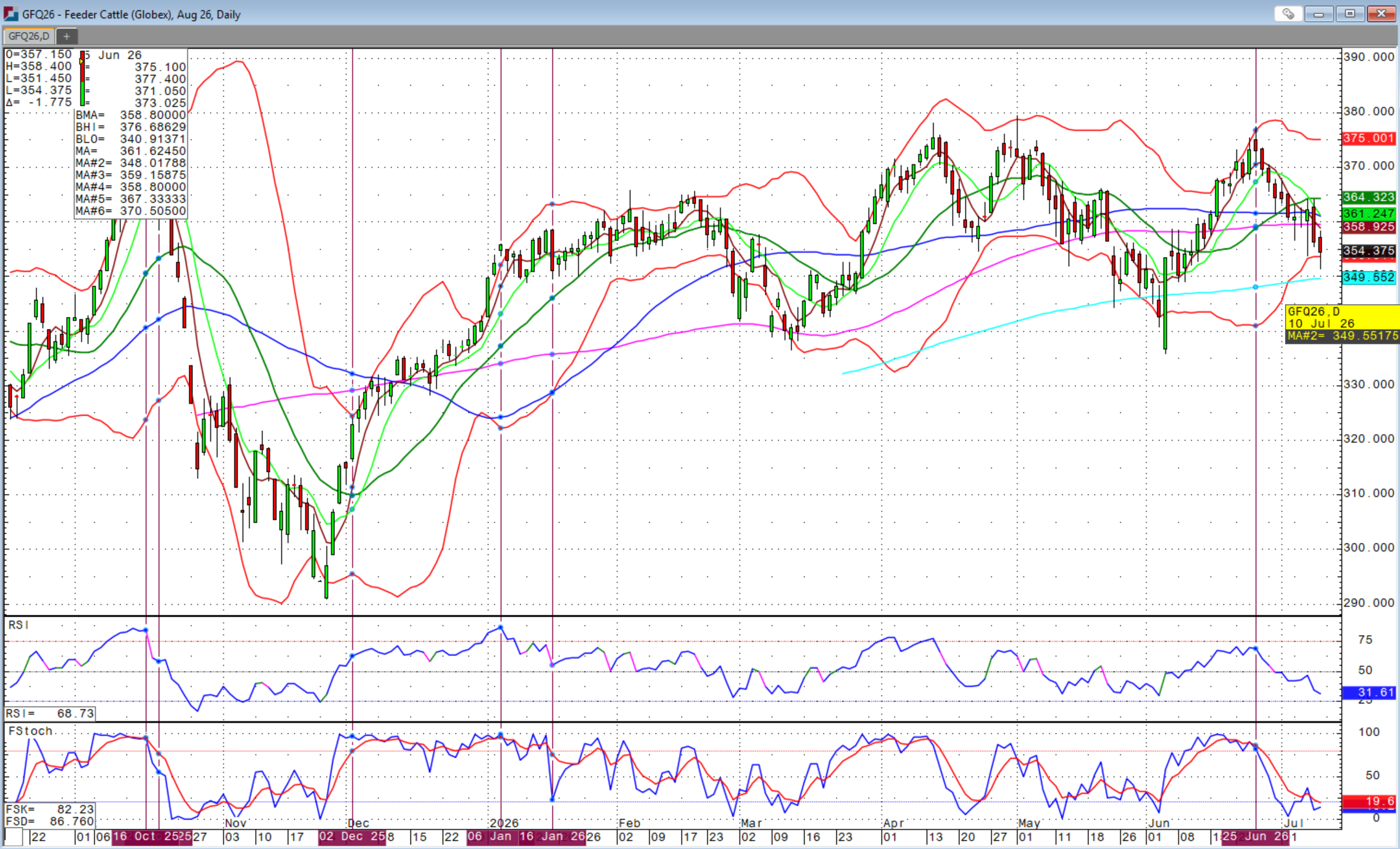

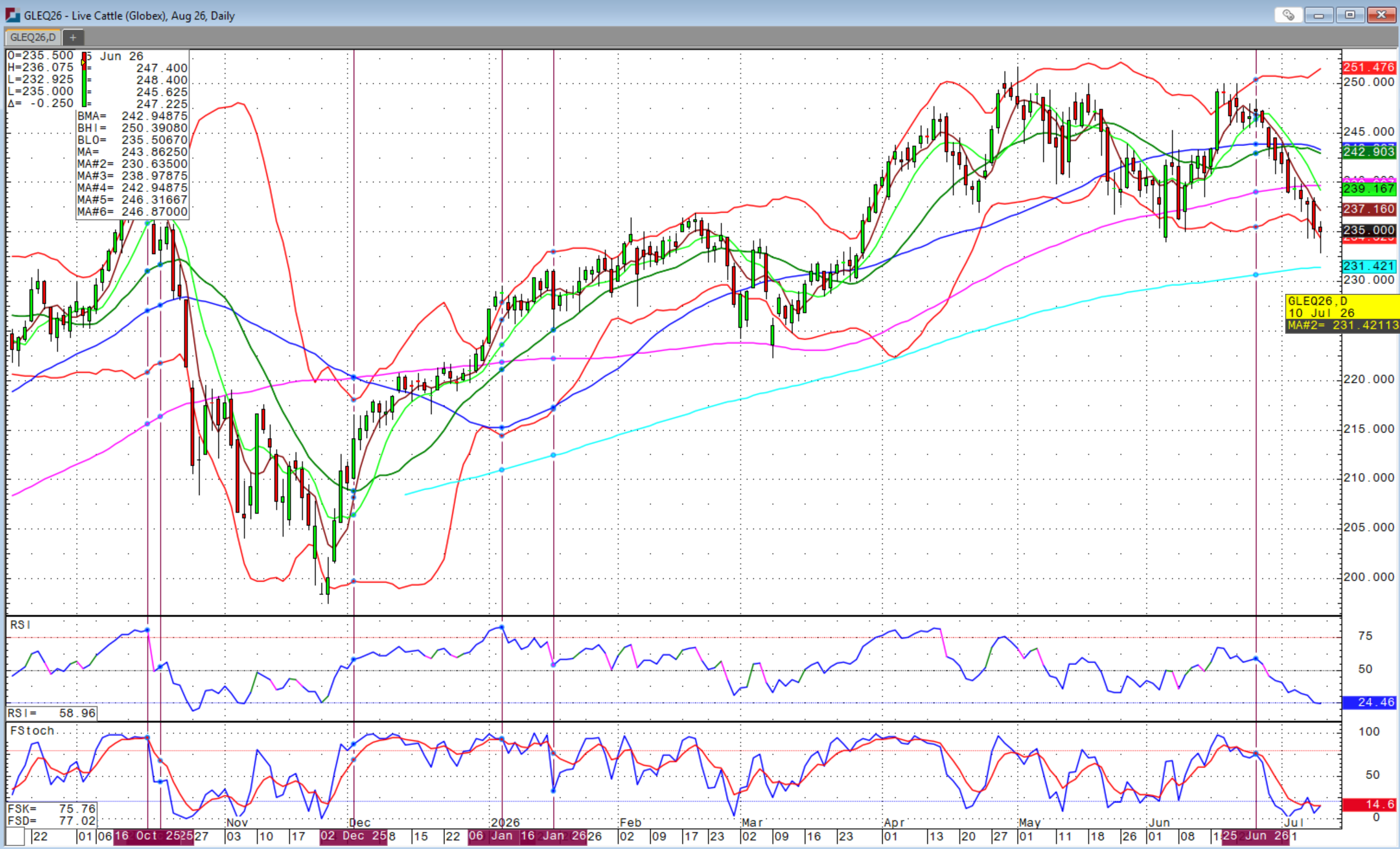

The cattle markets have been a choppy affair this past week after a brutal selloff that started on June 25th. Just as this market begins to find footing, another hammer drops. Interestingly, the cash market indices remain well above the futures. The expectation is therefore that the futures are going to come up to meet the cash market or at least somewhere in between. Having said that, the cash markets have remained much firmer than the futures contracts.

Stronger grain prices, shifting fund positions and lighter trade volume during the summer months has largely been behind this, in my opinion. We traded through an upward sloping, multi-month trendline on Friday, but closed above it. The 200-day moving average is just below at $349.552 on August feeders and $231.421 on August fats. Since June 17th, the August fat cattle futures contract has had 14 lower day closes. Friday’s low on August fats below the June 22nd low was less than encouraging, but we did close above that low. Again, the 200-day moving average, if we reach it, should be strong support.

This market needs direction from strength in boxed beef prices and consumer resilience, which is beginning to wane with stubborn inflation across the economy. Thankfully, fuel prices have come down, but that could be about to reverse, at least somewhat. There is some consumer distraction at the moment with summer vacations well underway and spending continuing.

The real tell will be the return in August and back-to-school to see where things stand. If the war in Iran escalates along with energy markets, that will quickly impact the broader inflationary pressures in the economy and potential further tightening by the new Federal Reserve under Chair Warsh. Interest rates have come down in recent months, but we are not out of the woods just yet.

Stay vigilant as August can often be a tough time for equity markets that can spill over into the consumer and cattle.

Sidwell Strategies is the one-stop shop to protect cattle with futures, puts, LRP or a combination of all, which is probably the best strategy overall. If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available. It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Wishing everyone a successful trading week! Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

Brady Sidwell is a Series 3 Licensed Commodity Futures Broker and Principal of Sidwell Strategies. You’re your Trading Account with Sidwell Strategies at https://portal.stonex.com/prefill/index/BradySidwellU52F112P. Contact us at (580) 232-2272 or at trade@sidwellstrategies.com.

Futures and Options trading involves the risk of loss and may not be suitable for all investors. Review full disclaimer at https://www.sidwellstrategies.com/fccp-disclaimer-21951.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)