Virax Biolabs (VRAX) shares ripped higher on July 9 after the company announced an exclusive commercial supply agreement with healthcare heavyweight Fosun Diagnostics.

As investors cheered the new partnership, VRAX’s relative strength index climbed into the early-70s, a technical setup that often triggers aggressive profit-taking.

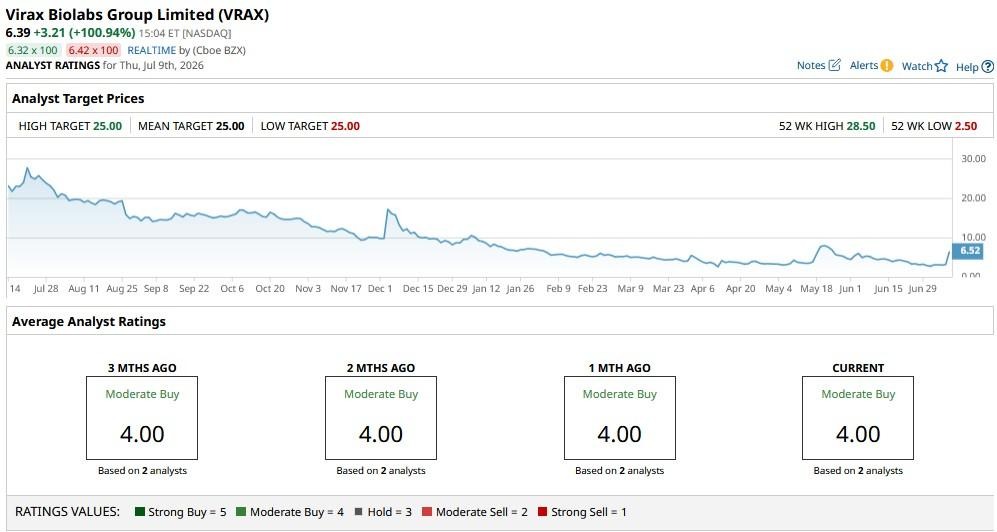

Despite its explosive rally on Thursday, Virax stock remains down more than 25% year-to-date.

Why Virax Stock Soared on Thursday

The announcement is largely bullish for VRAX shares because it opens up six ASEAN markets — Thailand, Vietnam, Indonesia, Malaysia, Singapore, and the Philippines — for the firm’s flagship offering, ImmuneSelect.

By partnering with a subsidiary of the multi-billion-dollar Fosun Pharma group, Virax gains instant access to an established regional customer network as well as commercial infrastructure.

Crucially, the agreement is purchase-order-driven, creating immediate, near-term revenue potential for the company’s T-cell immune profiling products.

The structured, volume-based pricing tiers pave a scalable path for future commercial expansion, potentially including private-label manufacturing opportunities.

Why VRAX Shares Still Aren’t Worth Buying

Investors should note, however, that Virax remains a highly speculative, high-risk play. At its core, it remains a penny stock vulnerable to extreme, retail-driven manipulation and unusual volatility.

Capitalizing on today’s rally, Virax announced a $3.3 million options-exercise deal at a discounted $6 per share.

The biotechnology company will issue up to 2.1 million new warrants, which introduces substantial dilution risk for existing shareholders as well.

It's also worth mentioning that Virax Biolabs recently executed a 1-for-25 reverse stock split to regain compliance with Nasdaq’s minimum listing requirements, further highlighting the

This reinforces just how fragile VRAX’s fundamentals really are.

Wall Street’s View on Virax Biolabs

At the time of writing, Virax Biolabs receives coverage from just two Wall Street firms.

While analysts at those two firms rate it “Moderate Buy,” with the mean price target of $25, the sheer lack of broader Wall Street coverage underscores how little institutional conviction there is behind VRAX stock.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/Chipset%20held%20over%20rush%20hour%20traffic%20by%20Jae%20Young%20Ju%20via%20iStock.jpg)