/The%20Figma%20app%20on%20a%20smartphone%20screen%20by%20Photo%20Agency%20via%20Shutterstock.jpg)

Figma (FIG) got a much-needed boost this week. Bank of America reinstated coverage of the design software company with a “Buy” rating and a $30 price target. The stock reacted well to the development, though long-term shareholders will hardly have any reason to get excited about the 6% surge in stock price. The stock has been hammered, declining 85% from its 52-week high. The steep fall comes due to investors worrying that generative AI could make design tools like Figma less necessary.

BofA analyst Tal Liani thinks that the market might have overreacted to the potential risk. His view is that AI is more of a tailwind than a threat. While AI generates designs and content quickly, Figma is the platform where teams actually collaborate and turn that work into finished products. Liani believes AI creating more complexity increases the need for a shared space to manage it all. So, if anything, this could bring even more people into building digital products, which works in Figma's favor. There’s data behind the optimism too. In the first quarter of 2026, 75% of enterprise customers bought extra AI credits after using up their initial allowance. This suggests that companies are embracing AI features rather than avoiding them.

What makes the bullish view even stronger is that in the same note, BofA took the opposite stance on the company’s larger rival, Adobe (ADBE). The firm downgraded Adobe to an “Underperform” rating, arguing that Figma is set to benefit from the AI shift while Adobe faces tougher competition. The statement is a big boost for Figma, a company whose stock had nosedived from $143 to less than $17 in the past 12 months. Meanwhile, Adobe is dealing with problems of its own.

About Figma Stock

Figma is a design software company that helps teams build digital products in real time. Its product portfolio includes Figma Design, Figma Slides, FigJam, and Dev Mode. Founded in 2012, the company is headquartered in San Francisco and is led by co-founder and CEO Dylan Field.

Figma’s stock has had a brutal run. Since going public nearly a year ago, FIG stock is down 81%, significantly underperforming the broader software sector, with the iShares Expanded Tech-Software ETF (IGV) declining roughly 15% over a similar period. The decline reflects investor concerns that AI could reduce the demand for design software. In the last five days, however, positive analyst sentiment has helped the stock recover 10%.

Figma’s valuation is tricky to assess given it only recently went public. The forward GAAP P/E isn’t meaningful since the company is not yet consistently profitable. The forward price-to-sales ratio of 8.18x reflects a premium valuation due to the market’s high growth expectations. The EPS growth trajectory looks solid. After a slight dip expected in 2026, Figma’s growth is expected to improve every year, reaching 20% in 2027, 32% in 2028, and 47% in 2029. The stronger profitability estimates reflect confidence in Figma’s growing enterprise adoption and early monetization of its AI features.

The balance sheet is perhaps the company’s strongest aspect. Figma holds $1.64 billion in cash against just $56 million in debt. The company being net cash positive by over $1.58 billion means it has plenty of flexibility to invest in growth. Overall, with growth expected to accelerate and a balance sheet carrying almost no debt, Figma’s fundamentals look far healthier than its share performance suggests.

Figma’s Revenue Jumps 46% As It Raises Full-Year Guidance

Figma reported its first-quarter fiscal 2026 earnings on May 14. Revenue of $333.4 million increased 46% year-on-year (YoY), beating the firm’s own guidance for the first quarter. The CEO stated that Q1 was an incredible quarter for Figma, with customers going bigger and broader with the company than ever before. Net dollar retention rose to 139%, its highest level in over two years. CFO Praveer Melwani also called it an exceptional quarter for Figma. Melwani credited the stronger-than-expected seat expansion, enterprise adoption, and early traction from the company’s new AI products as the reasons for a decent quarter.

The company has also raised its full-year guidance. Revenue for the full year is now expected to be $1.422 billion to $1.428 billion, a $55 million increase from its previous outlook. For the second quarter, revenue guidance is $348 million to $350 million, above the analyst consensus. Q2 is expected to be the first full quarter of AI credit monetization. The management sees Figma’s AI features becoming a growing revenue driver through the rest of the year.

What Are Analysts Saying About FIG Stock?

Back in May, Morgan Stanley analyst Elizabeth Porter reiterated an “Equal Weight” rating for Figma while keeping the price target unchanged at $38. The analyst believes the company is well-positioned to benefit from AI-driven software creation. However, ongoing financial uncertainties have led the analyst to keep the “Equal Weight” stance. And in June, Wells Fargo analyst Michael Turrin reduced Figma’s price target from $42 to $36 while maintaining a “Buy” rating.

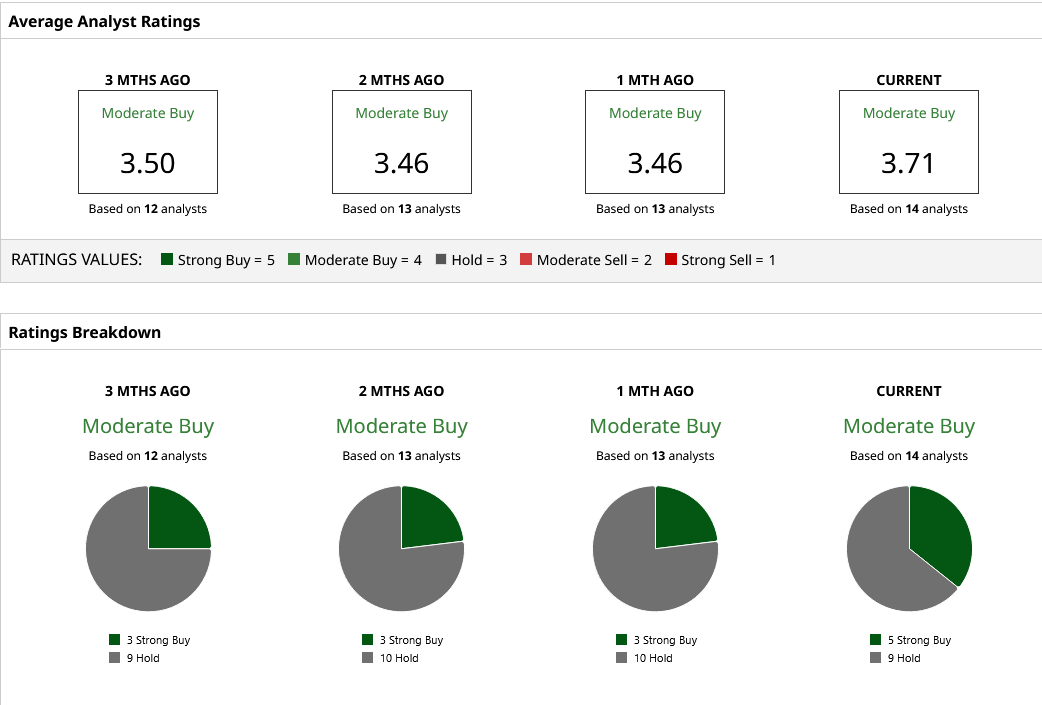

Based on the 14 Wall Street analysts, FIG stock holds a “Moderate Buy” rating with a mean price target of $31.10, indicating a healthy 45% upside. The highest analyst price target reflects nearly 100% upside, while even the lowest price target is above the company’s current stock price. The positive consensus makes sense for a company that has lost 85% of its value from its 52-week high, is delivering strong revenue growth, and has raised its full-year guidance.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Corning%20Incorporated%20on%20screen%20in%20front%20of%20website%20By%20Timon.jpeg)