/Semiconductor%20Chip%20by%20Gorodenkoff%20via%20Shutterstock.jpg)

Memory chipmaker Samsung projected its Q2 operating profit at 89.40 trillion Korean won (about $58.40 billion), representing a 19-fold increase, as AI chip demand remains sky-high. This is great news for another memory chipmaker, Micron Technology (MU), which is just coming off a high after a blockbuster earnings report.

Micron is experiencing skyrocketing demand amid soaring memory costs. While it’s a pain for tech giants buying these chips, it's been a boon for Micron. The company said its average DRAM selling price jumped more than 260% year-over-year (YOY) in the fiscal third quarter. Chief Business Officer Sumit Sadana also said the company has secured long-term supply deals with consumer-focused smartphone and PC makers.

About Micron Stock

Micron Technology is a global leader in memory and storage solutions, designing and manufacturing DRAM, NAND, and NOR products that support data centers, AI, smartphones, PCs, and connected devices. Its vertically integrated operations cover research, wafer fabrication, assembly, testing, and sales, giving it tight control over quality and scale.

Headquartered in Boise, Idaho, Micron serves customers worldwide through a broad manufacturing and design footprint across North America, Asia, and other key markets. Micron has a massive market capitalization of $1.07 trillion.

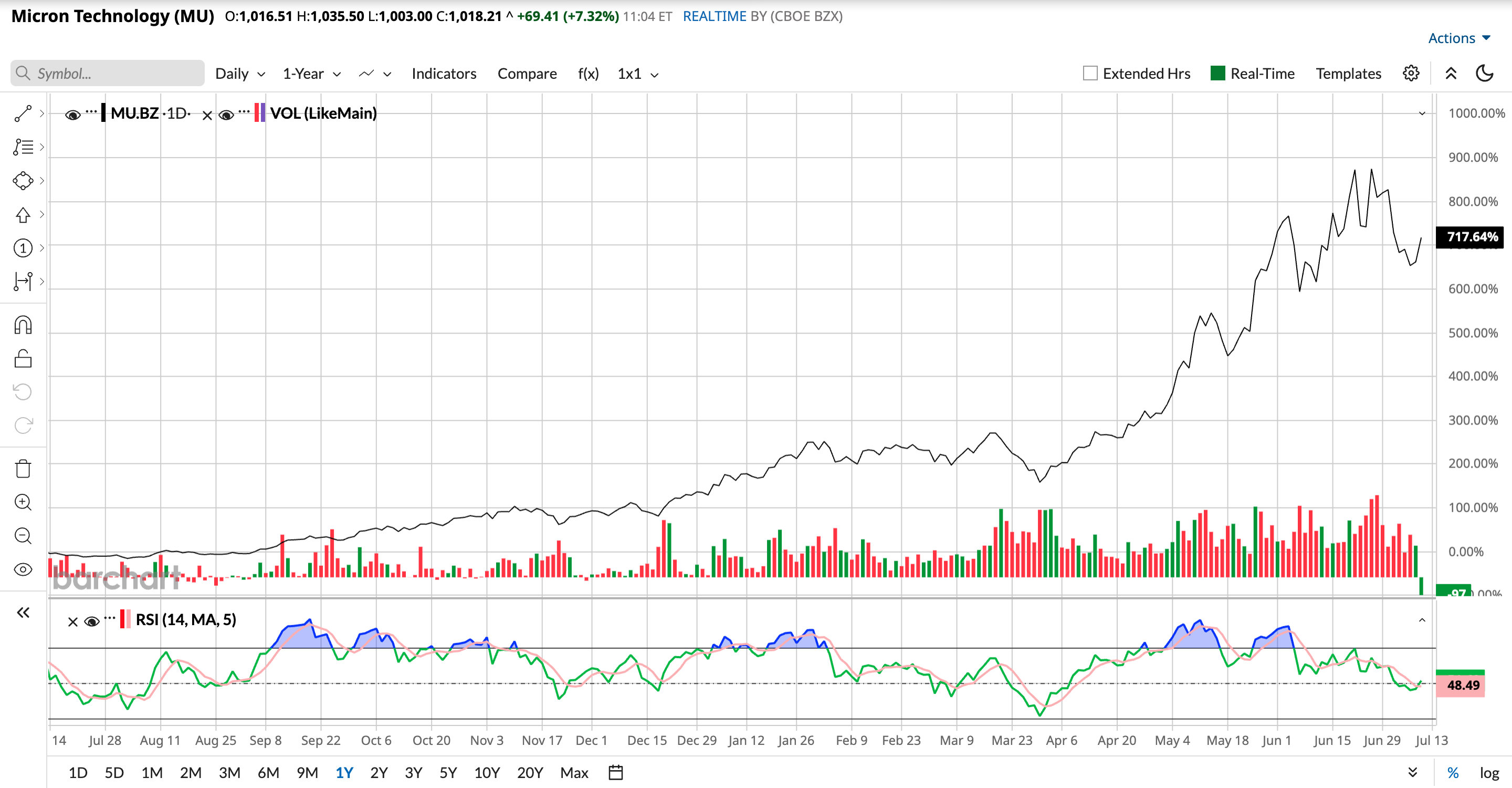

Micron’s stock has climbed sharply over the past year as investors have priced in a much stronger memory-cycle recovery, especially in AI-driven DRAM and NAND demand tied to data centers and server upgrades. Over the past 52 weeks, the stock has gained 729.5%, while it is up 255.3% year-to-date (YTD). Micron’s shares reached a 52-week high of $1,255 on June 25, but are down 19% from that level.

After residing in overbought territory for a short while, the stock’s 14-day relative strength index (RSI) has dropped to 51.41, indicating strong momentum. Micron’s valuation is also reasonable. On a forward-adjusted basis, its price-to-earnings (non-GAAP) ratio of 12.94 times is lower than the industry average of 24.76 times.

Micron Beats Q3 Estimates on Strong AI Memory Demand

Micron reported record-breaking results in the third quarter of fiscal 2026 (quarter ended May 28), amid heightened demand during the memory crunch. The company’s revenue increased 345.7% YOY to $41.46 billion, exceeding the $36.72 billion expected by Street analysts.

This skyrocketing increase was broad-based, with the company recording solid growth across all its business units. The core data center business unit recorded 653.2% revenue growth, while the cloud memory business unit's revenue increased 306.6% YOY.

The unprecedented rise also gave Micron a huge boost in profitability. The company’s non-GAAP operating income as a percentage of its revenue increased from 26.8% to 81.2%. Its non-GAAP EPS grew from just $1.91 in Q3 FY2025 to $25.11 in Q3 FY2026. And, the EPS figure exceeded the $21.39 expected by analysts.

Wall Street analysts expect Micron’s profitability to continue to grow at a brisk pace. For the current quarter, its EPS is expected to grow significantly YOY to $31.06. For fiscal 2026, analysts expect the company’s EPS to grow considerably to $72.94, followed by a 109.3% expansion to $152.63 in fiscal 2027.

What Do Analysts Think About Micron’s Stock?

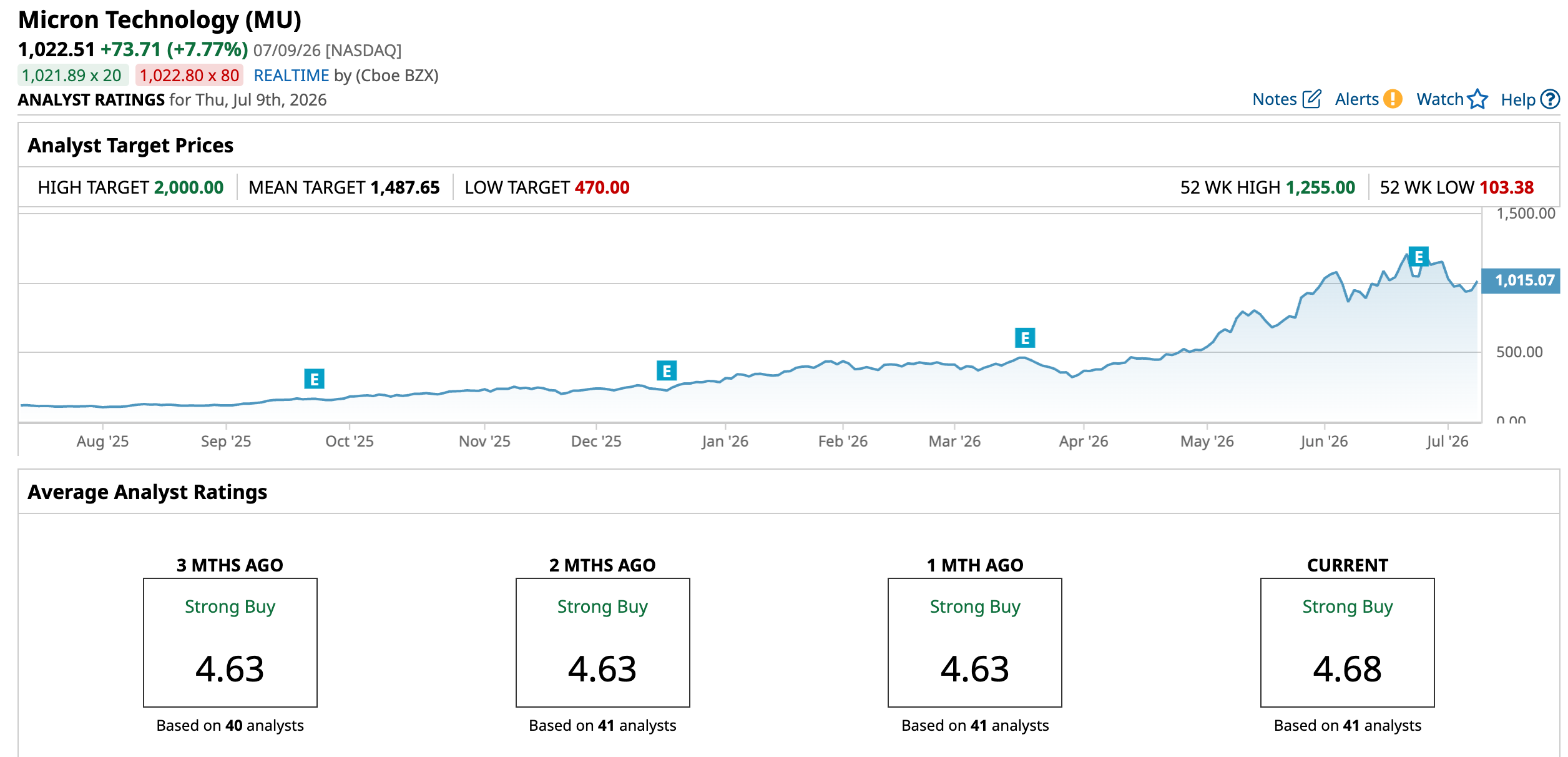

Last month, analysts at Cantor Fitzgerald reiterated an “Overweight” rating on the stock and raised the price target from $1,500 to a Street-high of $2,000. This indicates that Cantor analysts are optimistic about Micron’s prospects.

Recently, Bank of America analysts maintained a bullish “Buy” rating on Micron’s stock and set a $1,500 price target, citing robust AI infrastructure spending to keep the chip cycle on track. Expecting cloud and AI infrastructure spending to reach about $1.50 trillion by 2027, up 40%-50% YOY, and memory playing a big role, analysts see heightened prospects for the company.

Needham analysts also raised the price target from $1,550 to $1,650, while maintaining a “Buy” rating. The firm cited Micron’s recent earnings beat and raised guidance, which exceeded expectations.

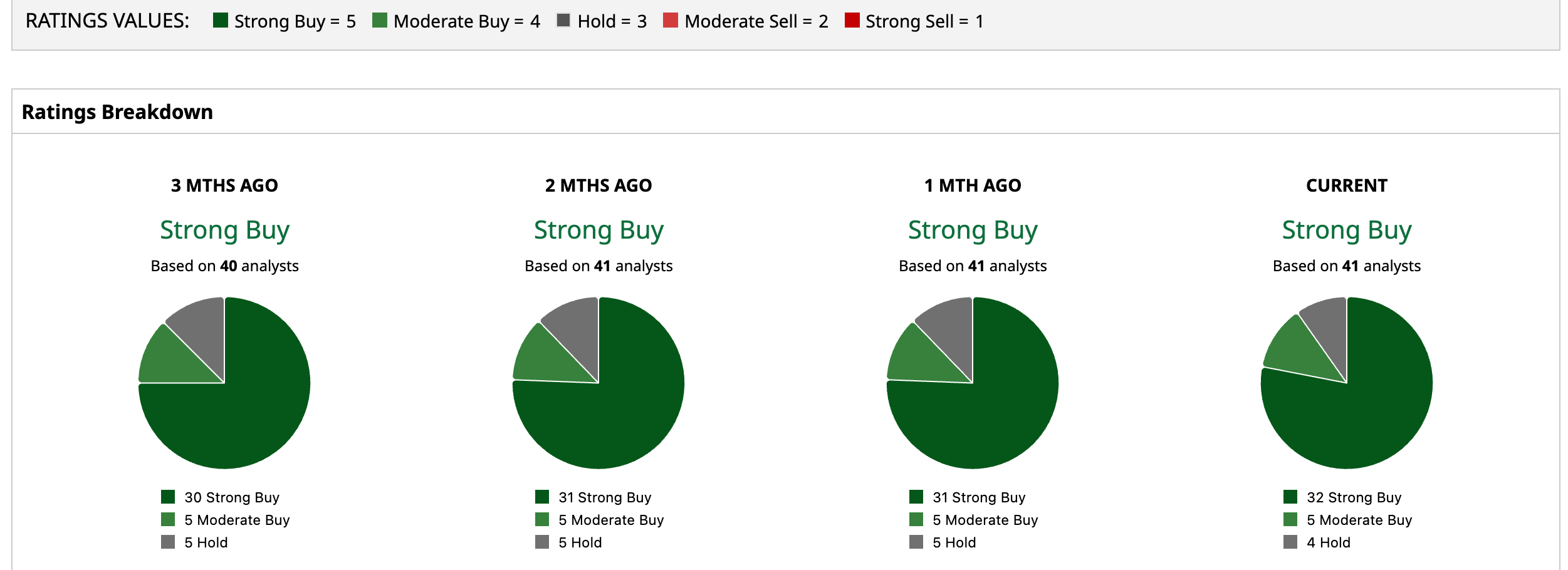

Micron Technology has become a popular name on Wall Street, with analysts awarding it a consensus “Strong Buy” rating overall. Of the 41 analysts rating the stock, a majority of 32 analysts have given it a “Strong Buy” rating, five analysts rated it “Moderate Buy,” while four analysts are taking the middle-of-the-road approach with a “Hold” rating. The consensus price target of $1,487.65 represents a 45.5% upside from current levels. The Street-high price target of $2,000 indicates a 95.6% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)