/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

The ongoing artificial intelligence (AI) buildout has been a massive tailwind for memory chip prices over the last 12 months. Notably, one of the biggest players in the business is making a bold move that could ripple across the entire industry.

Samsung Electronics is reportedly pushing hard for another round of price hikes on its DRAM chips — and the size of the potential increase is quite significant. That push comes at a moment when rival Micron Technology (MU) is already riding one of the strongest stretches in its history. What happens next will matter for anyone who owns a phone, laptop, or a data center full of servers. Let's take a closer look.

Samsung Is Set to Hike Memory Chip Prices

According to a report from ZDNet, Samsung is negotiating aggressively with customers to raise its third-quarter DRAM average selling price by up to 20% from the prior quarter. The report adds that low power DRAM (LPDDR) chips, which face severe supply shortages in both the server and mobile markets, could see even steeper increases, though it is not yet clear whether buyers will accept the full ask.

Samsung's DRAM prices have reportedly climbed faster than those of SK Hynix. Industry watchers cited by ZDNet say that is because Samsung carries a bigger share of commodity DRAM, where prices swing more sharply, and because the company has taken a more aggressive pricing approach overall.

The report notes Samsung's DRAM prices jumped more than 90% quarter-over-quarter in Q1, with growth estimated at 50% to 60% in Q2. SK Hynix, whose lineup leans more heavily on premium HBM chips, is expected to see smaller gains.

Research firm TrendForce offers a somewhat more tempered view. The firm expects supply to remain extremely tight through Q3 2026, but says weaker demand in consumer electronics and tougher year-over-year (YOY) comparisons should keep increases in the 13% to 18% range quarter-over-quarter.

Both reports point to the same underlying story. Memory chips remain in short supply, and the companies that make them are using that leverage to push prices higher.

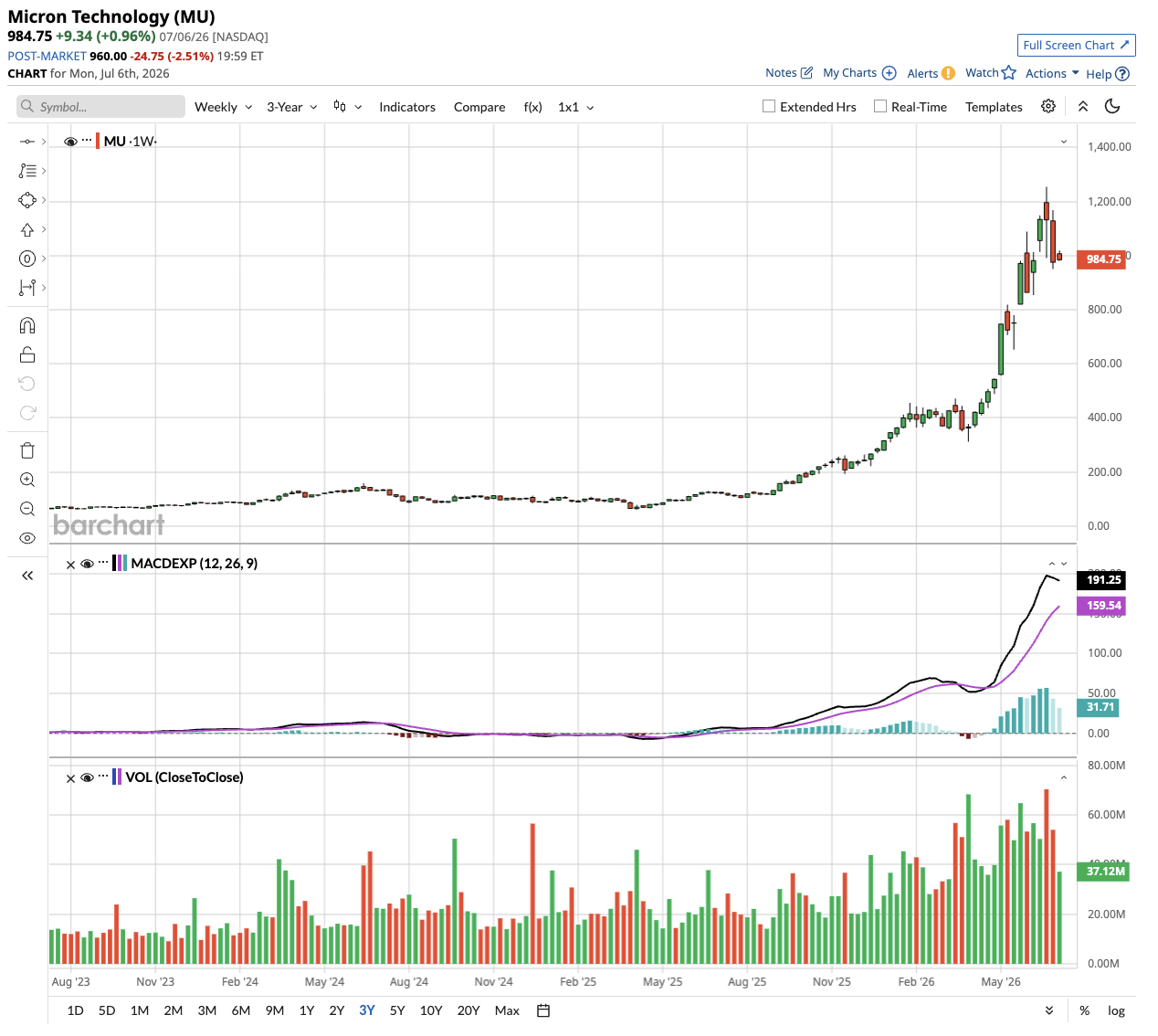

Micron Has Expanded Profit Margins

In fiscal Q3 2026, Micron reported revenue of $41.5 billion, an increase of almost 350% YOY. Notably, the company also reported revenue of $23.9 billion in Q2 and $13.6 billion in Q1.

Gross margins totaled 84.6% in Q3, up from 37.7% in the year-ago period. Over the last 12 months, Micron also increased operating margins from 23.3% to 80.4%. In plain terms, Micron is now keeping much more of every dollar it earns, largely because customers are paying more for the same chips.

Micron's cloud, core data center, and mobile business units each pulled in $11.5 billion or more in the latest quarter, while the automotive unit brought in $4.6 billion. DRAM revenue alone totaled $31.3 billion, nearly double what it was three months earlier.

Executives credited much of this to a shift toward long-term supply deals. Chief Business Officer Sumit Sadana said on the earnings call that Micron has signed 16 strategic customer agreements, structured as take-or-pay contracts that cannot be canceled and carry price floors and ceilings. These agreements now include some of Micron's largest hyperscaler customers and even reach beyond 2027 in visibility.

As ZDNet notes, a growing share of memory shipments is being locked in under these long-term deals, which should help prevent a sharp price collapse next year even as the pace of increases slows.

The trend has spread beyond tech giants, too. Micron recently signed a long-term supply agreement with General Motors (GM) covering memory chips for vehicles, a sign that even automakers are locking in supply amid the ongoing squeeze.

What's Next for MU Stock?

If Samsung succeeds in pushing DRAM prices up another 20%, it would likely signal that the same tailwind is still blowing for Micron. Both companies target similar markets and customers, while wrestling to keep up with demand.

Micron CFO Mark Murphy told analysts that Micron expects cash flow to keep growing into Q4 and plans to return excess cash to shareholders. The company also raised its 2026 capital spending target to around $27 billion and plans to spend even more next year. For now, memory chip prices are heading in one direction. And as long as that stays true, Micron's remarkable run looks far from over.

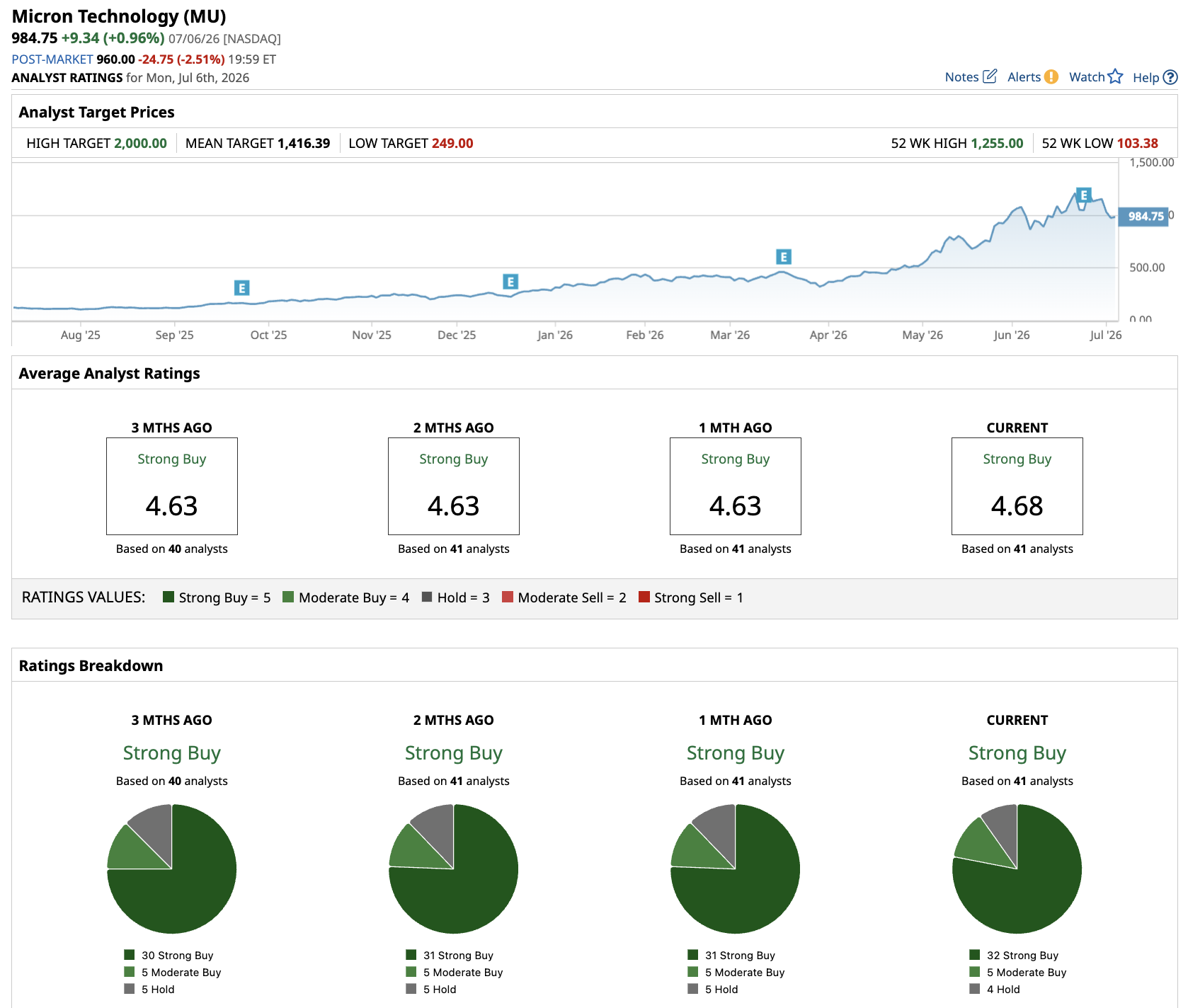

Out of the 41 analysts covering MU stock, 32 recommend a “Strong Buy” rating, five recommend a “Moderate Buy,” and four recommend a “Hold” rating. The average price target is $1,421.94, which implies potential upside of 50% from current levels.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)