/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

Shares of Micron Technology (MU) have been on an extraordinary run, rising about 800% over the past year. Micron’s explosive rally has been driven by soaring artificial intelligence (AI)-led demand for its high-bandwidth memory (HBM) chips and data-center storage products.

Moreover, an industry-wide supply shortage has strengthened memory pricing and boosted profitability. Those powerful tailwinds have helped transform MU into one of the market's top-performing stocks.

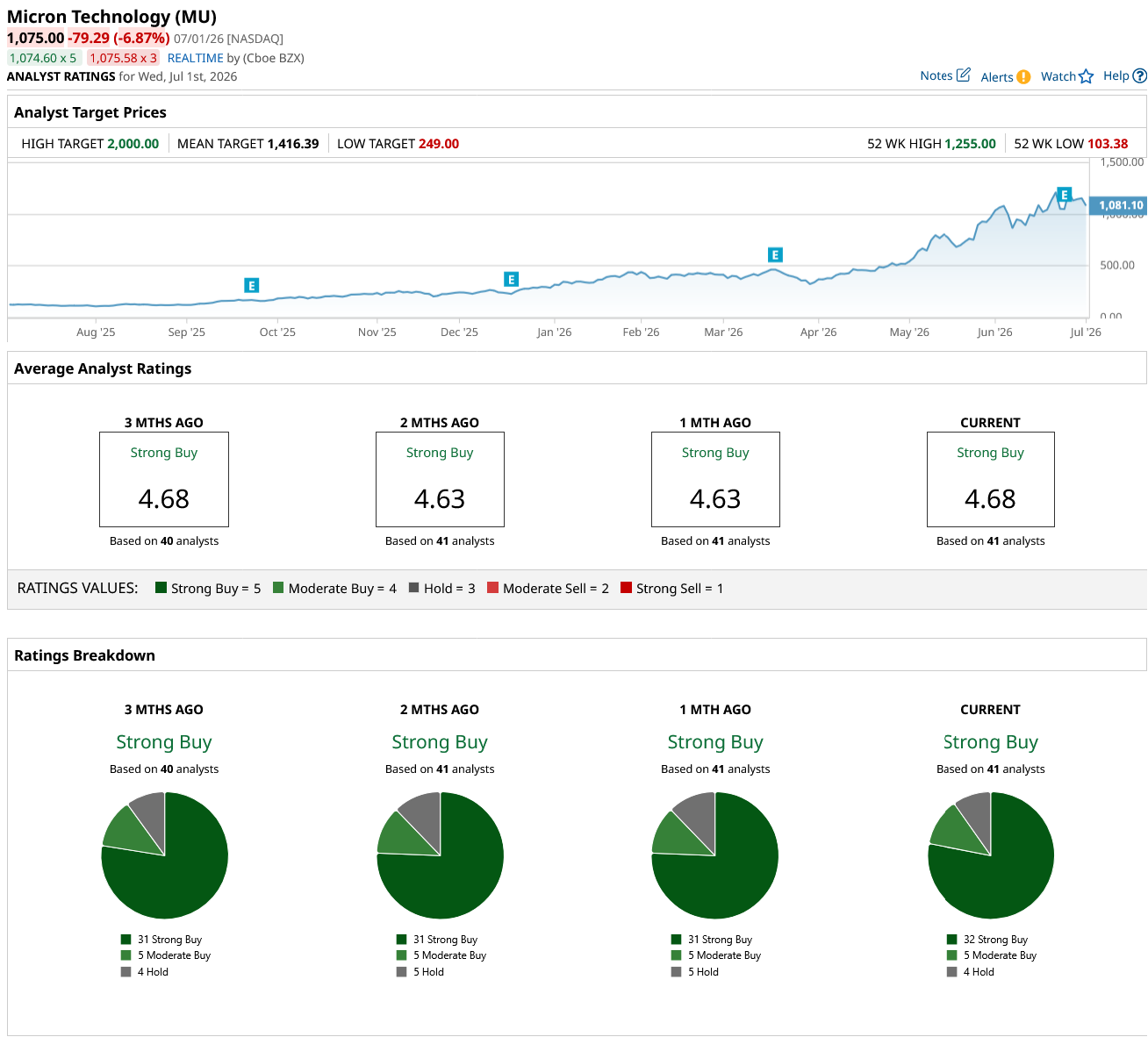

Despite the surge, some Wall Street analysts believe the rally may be far from over. The Street's highest price target stands at $2,000, implying about 73% upside from MU stock's June 30 closing price of $1,154.29.

While the price target looks steep, especially after the massive rally in Micron's stock, there are three strong reasons MU stock could hit $2,000.

Reason #1: Supply Conditions Continue to Favor Micron

Micron is operating in one of the strongest memory markets the industry has experienced in years. Tight supply and booming AI-driven demand have driven a sharp increase in prices across both DRAM and NAND, and those favorable conditions could persist through 2027 and potentially beyond.

Micron recently delivered outstanding fiscal third-quarter results as demand for HBM, DRAM, and NAND products used in AI servers and data centers continued to outpace supply. The bigger contribution came from the significant price increase, which drove record revenue and higher profitability.

DRAM remained Micron's biggest growth engine. In the latest quarter, DRAM revenue surged to $31.3 billion, up 343% year-over-year (YoY). While bit shipments increased only by a low single-digit percentage, average selling prices jumped in the low-60% range amid industry-wide supply constraints and its solid product mix.

NAND delivered similarly impressive growth. Fiscal third-quarter NAND revenue reached a record $9.9 billion, increasing 361% YoY. Revenue nearly doubled from the previous quarter, rising 99% sequentially. Bit shipments increased by a mid-single-digit percentage, while average selling prices jumped in the mid-80% range as tight market conditions continued to support pricing.

Looking ahead, the favorable industry backdrop is far from over. Supply growth for both DRAM and NAND is expected to remain tight while AI infrastructure spending continues to expand, creating a market where demand is likely to exceed supply well into 2027. If that outlook holds, Micron could continue benefiting from elevated memory prices, supporting further revenue growth, expanding margins, and stronger earnings in the coming years.

Overall, Micron’s strong earnings growth potential strengthens its investment case and could continue to support its rally.

Reason #2: Micron’s SCAs Are a Big Catalyst

Micron's strategic customer agreements (SCAs) could become a major long-term catalyst for the stock. During the quarter, Micron signed 16 new agreements covering a significant portion of its DRAM and NAND production through 2030, with management expecting additional contracts over time.

Most of these SCAs are structured as take-or-pay agreements, providing Micron with predictable demand and greater earnings visibility. Many also include pricing mechanisms that protect the downside while allowing the company to maintain healthy profit margins.

Management said that for SCAs with price bands, the floor price alone would generate gross margins that are well above Micron's peak quarterly margins from any previous industry cycle.

Importantly, 14 of these agreements represent roughly $100 billion in guaranteed minimum revenue. In short, these SCAs will boost Micron’s earnings and add stability, supporting its share price rally.

Reason #3: Micron’s Valuation Supports Further Upside

Tight supply and higher pricing, solid AI-driven demand, and multi-year agreements strengthen Micron’s growth prospects.

While MU stock has rallied significantly, it still trades at 18.4x forward earnings, which appears inexpensive relative to its projected earnings growth. Analysts expect Micron’s earnings per share (EPS) growth of 834.1% in fiscal 2026, followed by 110.6% in fiscal 2027. MU’s solid earnings growth and compelling valuation could push its stock higher.

Can MU Stock Really Reach $2,000?

While a $2,000 share price may seem high, Micron has several factors working in its favor. Strong supply-demand dynamics, long-term customer agreements, and its relatively low valuation suggest MU stock has the potential to reach that milestone over time.

Wall Street also remains optimistic about Micron, with analysts assigning the stock a “Strong Buy” consensus rating.

On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)