/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

The insurance industry is now putting AI to work. A 2026 outlook from Alpha FMC shows insurers are now using AI across underwriting, claims, and pricing to improve results. And the pace is picking up.

A report from Zscaler (ZS) found that finance and insurance make up 23% of all AI and machine learning traffic, the highest of any sector, with activity jumping 91% year-over-year (YOY). At the same time, Information Services Group (III) has launched a new study focused on insurers using AI and analytics to improve pricing, risk decisions, and claims outcomes, showing just how serious this shift has become.

This is where Palantir Technologies (PLTR) steps in. Its software is already used in U.S. defense, works with Airbus (EADSY), and supports hundreds of companies. Now, it has signed a multi-year, multimillion-dollar expansion deal with GNP Seguros, Mexico’s largest insurer. This also marks its first publicly announced commercial customer in Latin America.

So, is this just one deal, or is Palantir Technologies starting to gain real traction outside the U.S.?

Inside Palantir’s Financial Strength

Palantir Technologies (PLTR) builds software that helps governments and companies make sense of large amounts of data. Its main platforms, Foundry and Gotham, are used to organize and analyze data so teams can make better decisions.

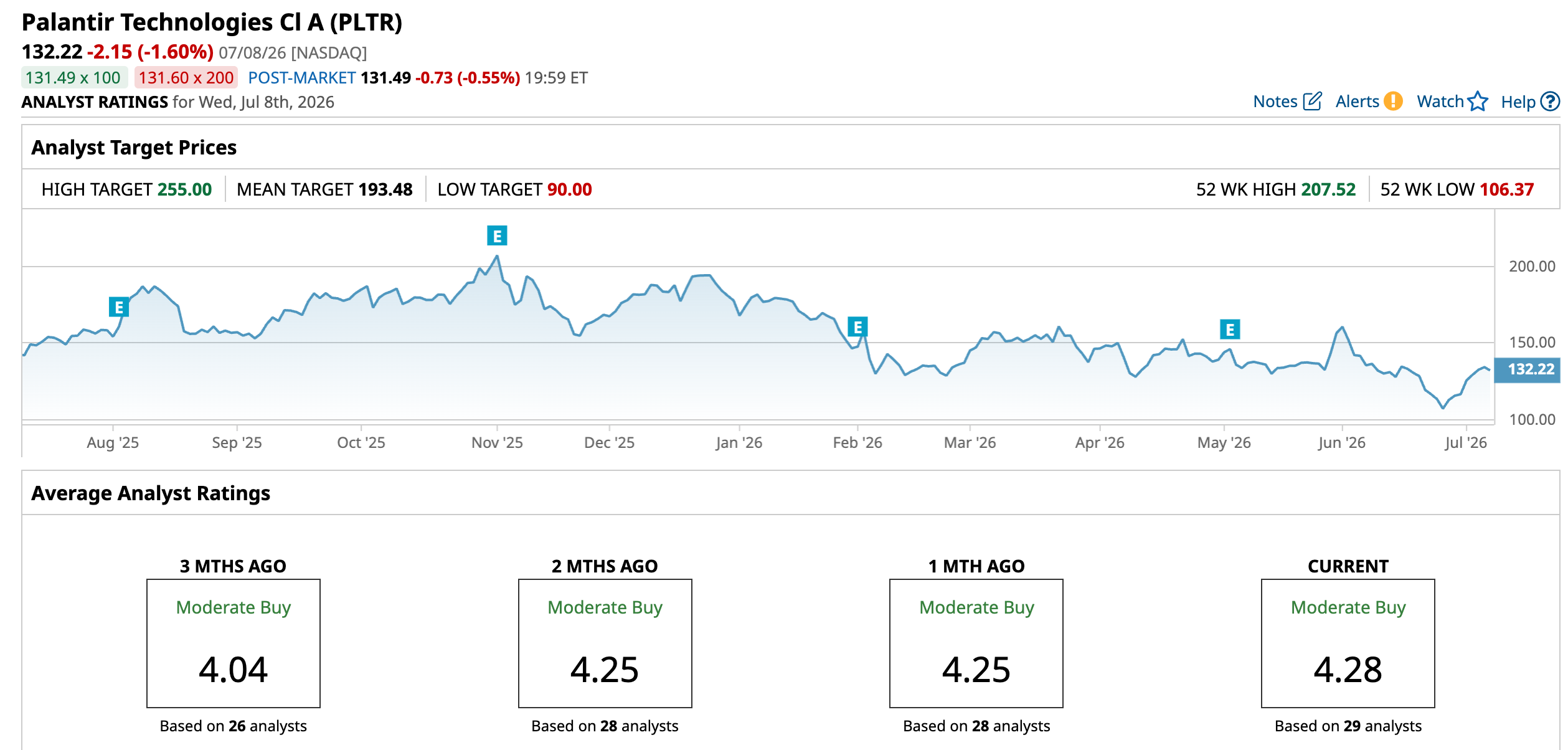

The stock has been under some pressure lately, down 5.36% over the past 52 weeks and off 25.61% so far this year.

Still, it trades at a much higher valuation than most peers, with a forward price-to-earnings ratio of 113.20 times versus the sector average of 24.77 times, showing that investors are still betting on strong growth ahead.

That optimism is backed by its latest results. In Q1 2026, revenue jumped 85% to $1.63 billion, with U.S. revenue leading the way, up 104% to $1.28 billion. U.S. commercial revenue rose 133% to $595 million, while government revenue grew 84% to $687 million, showing strength on both sides of the business. The company also closed 206 deals worth over $1 million, pushing total contract value to $2.41 billion, up 61%. Margins remained strong too, with a 46% operating margin, 53% net income margin, and 57% free cash flow margin.

Breaking Down the GNP Partnership

Palantir Technologies signed a multi-year, multimillion-dollar expansion deal with GNP Seguros, Mexico’s largest insurer under Grupo Nacional Provincial. The deal is notable because it makes GNP Palantir Technologies’ first publicly disclosed commercial customer in Latin America, a region where it has had limited visibility compared to its strong U.S. government and domestic business.

As part of the agreement, Palantir Technologies will roll out Foundry and its AI platform across GNP’s health, life, auto, and property insurance units, bringing claims, underwriting, operations, and risk data into one system.

This is not a brand-new relationship. GNP Seguros was already using Palantir Technologies’ tools for specific tasks like spotting fraud, tracking risk, and improving underwriting. What this new deal does is expand that usage across the entire business, connecting data that was previously scattered. With millions of customers, GNP can now use the platform to catch unusual claims early, flag possible fraud before payouts, and get clearer insights into risk while still keeping human oversight in place.

That matters because Palantir Technologies’ international commercial revenue rose just 2.5% in 2025, raising doubts about its ability to scale outside the U.S. This deal does not solve that overnight, but it does show that its software can handle large, real-world operations in other markets, especially in tightly regulated industries like insurance.

Analysts Weigh the Growth Story

Palantir Technologies is set to report its next earnings on August 3. Analysts see EPS coming in at $0.28 for the June quarter, up from $0.13 a year ago. For the full year, earnings are projected at $1.17, which would mark an 85.71% jump from $0.63.

Wolfe Research recently resumed coverage with a “Peer Perform” rating, moving up from “Underperform,” and called Palantir Technologies “too big to ignore” in enterprise AI. The firm points to its Ontology system as a key strength, helping companies actually use AI in day-to-day operations. It also flagged strong numbers behind the story, including 150% net sales retention, 85% revenue growth, a 97% jump in backlog, and a 40% rise in average revenue per customer.

But not everyone is fully convinced. Benchmark started coverage with a “Hold” rating and a $150 price target, arguing that Palantir Technologies needs to keep revenue growth in the 60% to 70% range to support its valuation. The firm also pointed to a weak spot, noting international commercial revenue grew just 2.5% in 2025, and questioned whether overseas markets can drive the next phase of growth.

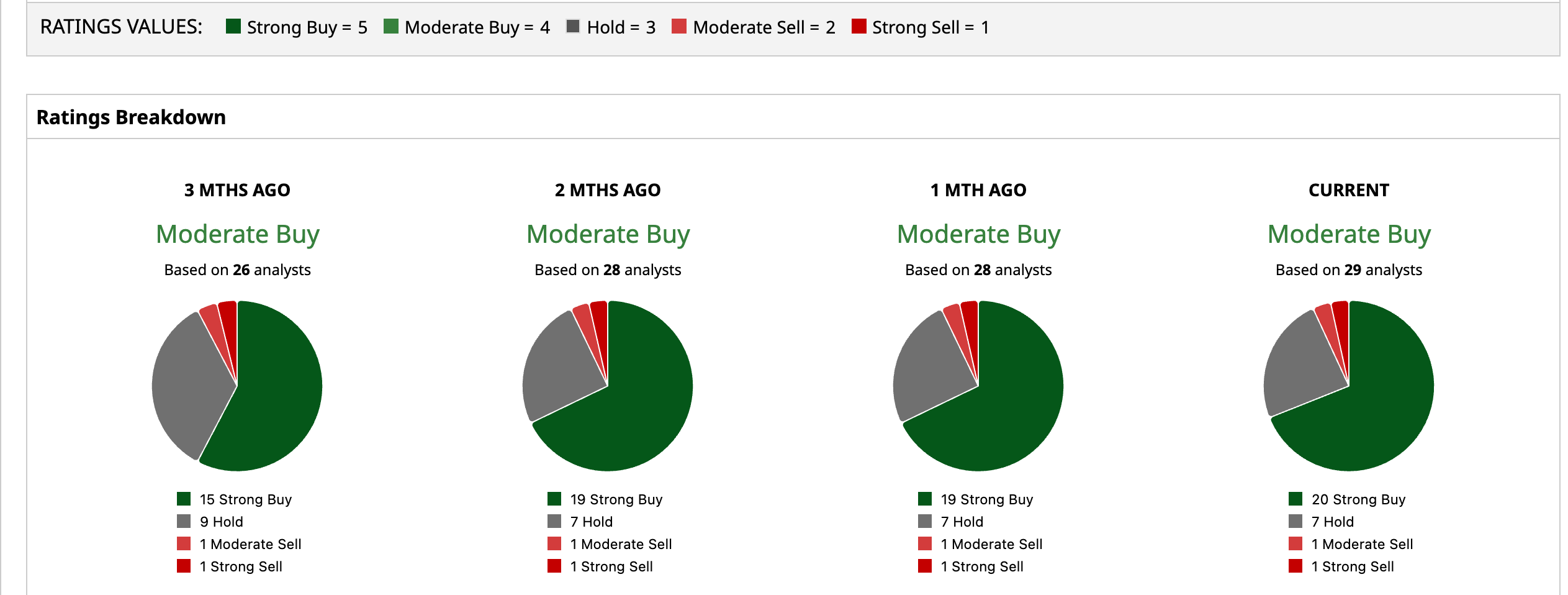

Even with that split, of 29 analysts covering the stock, a consensus rates it a “Moderate Buy”, with an average price target of $193.48, suggesting about 46.3% upside from current levels.

Conclusion

The GNP Seguros deal does not fully settle the debate, but it does move the needle. After a period where international commercial growth lagged, this marks a credible step into a large, real-world deployment outside the U.S., suggesting Palantir’s platform can translate across markets. It is likely too early to call it sustained global momentum, but it clearly strengthens that case. With strong fundamentals and rising AI demand, shares still look biased to the upside over the medium term, though volatility is likely as investors watch whether more international deals follow.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)