/Nvidia%20logo%20and%20sign%20on%20headquarters%20by%20Michael%20Vi%20via%20Shutterstock.jpg)

DeepSeek has already rattled Nvidia Corporation (NVDA) investors once with its low-cost artificial intelligence (AI) models. Now, the Chinese startup may be posing a far more direct competitive threat. Reports that DeepSeek is developing its own inference-focused AI chip could reduce its reliance on Nvidia’s GPUs, highlighting a broader industry trend in which leading AI developers are increasingly designing custom silicon to lower costs, improve efficiency, and gain greater control over their AI infrastructure.

The project is still in its early stages, with the company engaging chip design, foundry, and memory partners while quietly expanding its chip engineering team, but the implications could be significant.

Nvidia has built its AI dominance on supplying the computing power behind the world’s largest AI models, but the rise of custom chips from major AI players raises questions about the durability of that business model over the long term. Although experts note that DeepSeek’s move is unlikely to materially impact Nvidia’s near-term revenue, particularly given China’s shrinking contribution to Nvidia’s sales, it reinforces concerns that custom silicon could gradually erode the company’s pricing power and margins.

Now it remains to be seen whether this represents an isolated response to U.S. export restrictions or another sign that the AI industry is entering a new phase where more customers choose to build rather than buy their most critical AI hardware.

About Nvidia Stock

Nvidia Corporation is a global leader in accelerated computing and AI, renowned for pioneering the GPU that revolutionized gaming, data centers, and AI-driven computing. Headquartered in Santa Clara, California, Nvidia’s technology now powers everything from high-performance gaming and cloud computing to autonomous vehicles and generative AI applications. With a market cap of $4.8 trillion, Nvidia stands among the world’s most valuable companies, driven by its dominance in AI infrastructure and continued innovation in next-generation chip design.

Nvidia has been one of the market’s standout long-term performers, evolving from a gaming GPU manufacturer into the world’s leading provider of AI infrastructure. Surging demand for AI accelerators and data center chips has fueled a remarkable 984.4% gain in the stock over the past five years, far outpacing the broader market and helping Nvidia become one of the world’s most valuable companies. Its dominant position in AI chips and deep partnerships with hyperscale cloud providers have reinforced investor confidence in its long-term growth prospects.

However, that momentum has eased in recent months. Despite continuing to deliver strong operating performance, the stock is up just 9.45% year-to-date (YTD) and 27.57% over the past 52 weeks, lagging the broader technology sector.

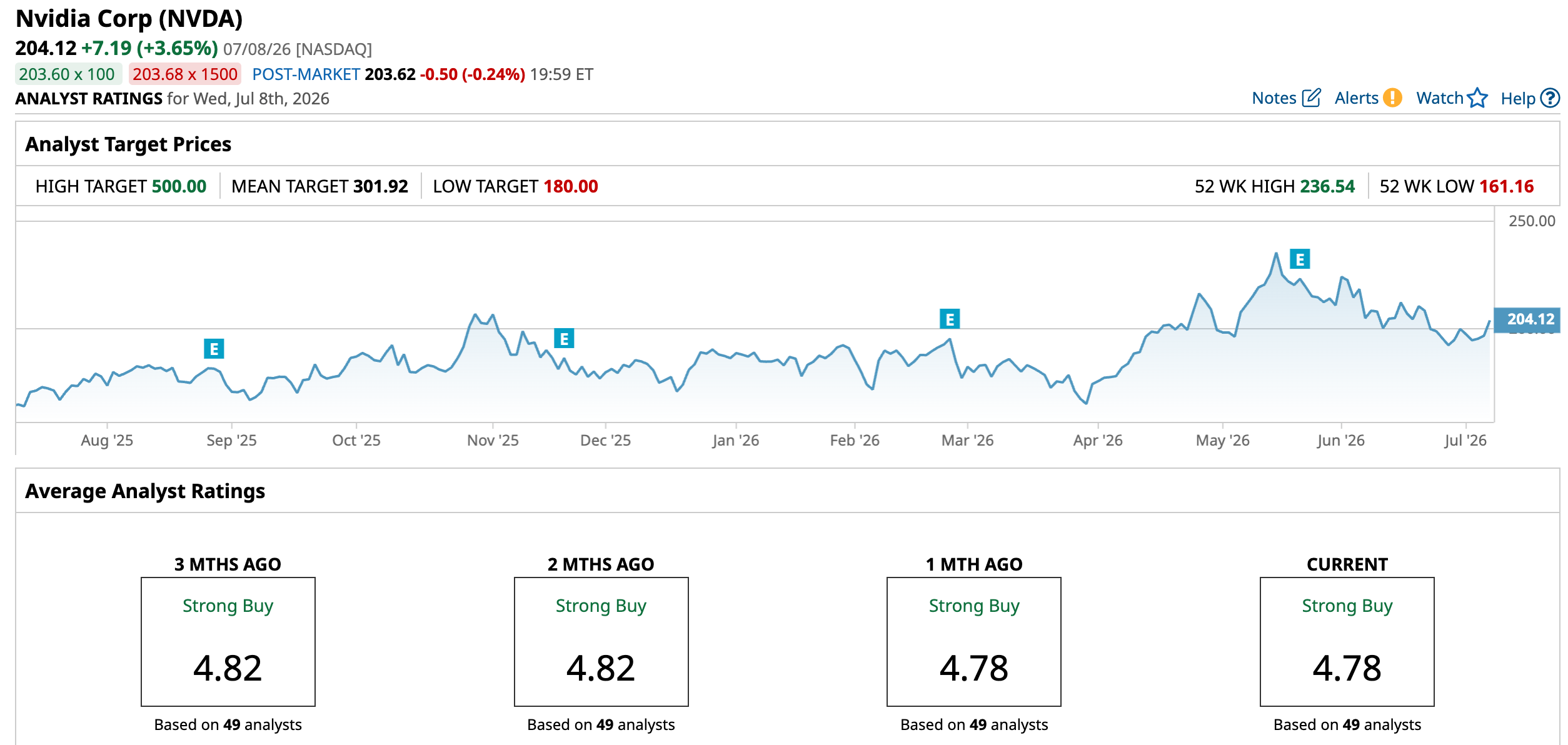

The stock is currently trading 13.7% below its 52-week high of $236.54 reached on May 14. Investor sentiment has been pressured by concerns over the sustainability of AI infrastructure spending, intensifying competition, U.S. export restrictions, and uncertainty surrounding the rollout of next-generation AI platforms, including Rubin and Kyber.

Recently, Nvidia faced reports that suggested its next-generation Kyber rack-scale AI infrastructure could be delayed until 2028. However, the company denied the speculation, maintaining that its roadmap remains on track. Designed for the Rubin Ultra platform, Kyber is expected to launch in 2027 as an integrated AI infrastructure system and a key component of Nvidia’s long-term AI infrastructure strategy.

Nvidia trades at 22.49 times forward earnings, which is currently a discount compared to industry peers and the historical average.

Q1 Earnings Beat Expectations

Nvidia delivered another exceptional quarter when it reported first-quarter fiscal 2027 results on May 20, further cementing its leadership in the rapidly growing AI infrastructure market.

For the quarter ended April 26, Nvidia posted record revenue of $81.6 billion, an 85% year-over-year (YOY) increase, while net income jumped 211% YOY to $58.32 billion. On a non-GAAP basis, earnings per share (EPS) rose 140% from the prior-year period to $1.87, beating analyst estimates. Non-GAAP gross margin expanded to 75% from 60.8% a year earlier, underscoring the company’s strong pricing power and favorable AI product mix.

Moreover, the Data Center segment remained Nvidia’s biggest growth driver, with revenue surging 92% YOY to a record $75.2 billion. Data Center networking revenue soared 199% YOY to $14.8 billion, while computing revenue accounted for the remaining $60.4 billion.

Its Edge Computing revenue increased 29% YOY to $6.4 billion, supported by demand across gaming GPUs, autonomous driving, robotics, and AI-enabled edge devices.

Management also pointed to accelerating adoption of Blackwell systems and highlighted expanding opportunities in agentic AI and enterprise AI infrastructure.

Additionally, Nvidia issued another optimistic outlook for the second quarter of fiscal 2027, forecasting revenue of $91 billion, plus or minus 2%, and a non-GAAP gross margin of about 75%. The guidance assumes no contribution from China Data Center compute revenue due to ongoing U.S. export restrictions.

Street expects Nvidia’s momentum to continue, with analysts forecasting EPS growth of 90.2% YOY to $8.69 in fiscal 2027, followed by another 34.3% increase to $11.67 in fiscal 2028.

Wall Street Remains Optimistic About Nvidia’s Prospects

Despite the soaring competition in the industry, NVDA’s dominance and prowess makes it a no-brainer choice for many.

Last month, Morgan Stanley reaffirmed its “Overweight” rating on the stock and maintained its $288 price target, reiterating Nvidia as its top pick in the processor space.

Plus, Truist Securities reiterated its “Buy” rating and $307 price target after Nvidia unveiled several next-generation AI products at GTC Taipei.

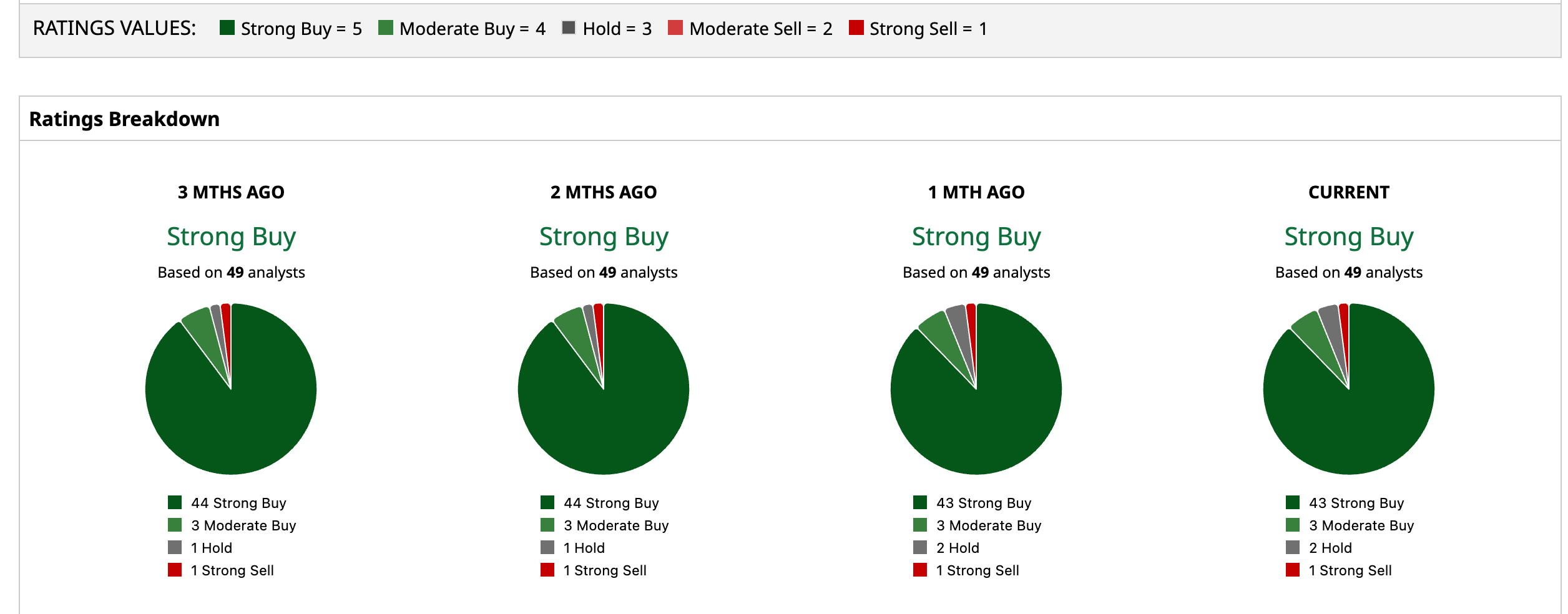

Overall, NVDA has a consensus “Strong Buy” rating. Of the 49 analysts covering the stock, 43 advise a “Strong Buy,” three suggest a “Moderate Buy,” two analysts give it a “Hold” rating, and one offers a “Strong Sell” rating.

The average analyst price target for NVDA is $301.92, indicating a potential upside of 47.9%. Also, the Street-high target price of $500 suggests that the stock could rally as much as 145%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)