Drone stocks such as AeroVironment (NASDAQ: AVAV), Red Cat Holdings (NASDAQ: RCAT), and Kratos Defense & Security Solutions (NASDAQ: KTOS) are down significantly in 2026, driven by macroeconomic and sector-specific headwinds and company-specific hurdles that mask the mounting potential. While near-term events have weighed on their stock prices, backlogs continue to swell. Record-breaking backlogs and funded contracts are the story in 2026, pointing to revenue and earnings strength in the upcoming quarters.

Looking at the industry from a 30,000-foot view, there are two robust tailwinds that will support business going forward. The first is a global shift away from Chinese-backed defense technology. Western powers are unilaterally shifting to domestic supply chains, which positions U.S. companies in prime placement. The second is the Pentagon's shift to unmanned systems. Unmanned systems provide superior performance at a lower cost of life and are central to next-gen warfare. The 2027 defense budget request includes nearly $75 billion for unmanned systems and counter-drone technology, a substantial potential infusion for the industry.

AeroVironment: Lost Contract Versus New Business

AeroVironment’s biggest hurdle is a lost contract that cut $1.7 billion out of its long-term outlook. Bad as it is, the loss is already being partly offset by new business, which is expected to continue growing. Highlights from the fiscal Q4 2026 earnings release include a $1.2 billion fully-funded backlog and a 1.4 book-to-bill ratio that provides clarity and visibility into future growth. As it stands, the consensus forecasts a modest double-digit growth pace over the coming years, compounded by margin improvement.

Among AeroVironment’s strengths is its counter-drone technology. Focused on three systems, the technology provides protection against autonomous attack, rogue aircraft, and layered defense for small-scale applications. Reasons to believe the upcoming results could outperform guidance include contracts awarded since its fiscal year 2027 outlook was initially released, such as the $500 million indefinite Delivery/Indefinite Quantity contract for counter-drone systems awarded by the Domestic Shield Program.

Analysts and institutional activity highlight the opportunity ahead. While analysts have trimmed their price targets, they remain solidly bullish, with the consensus at a Moderate Buy rating, implying about 67% upside. Institutional support is also solid, with the group owning more than 85% of the stock and buying at a pace greater than $2 to $1.

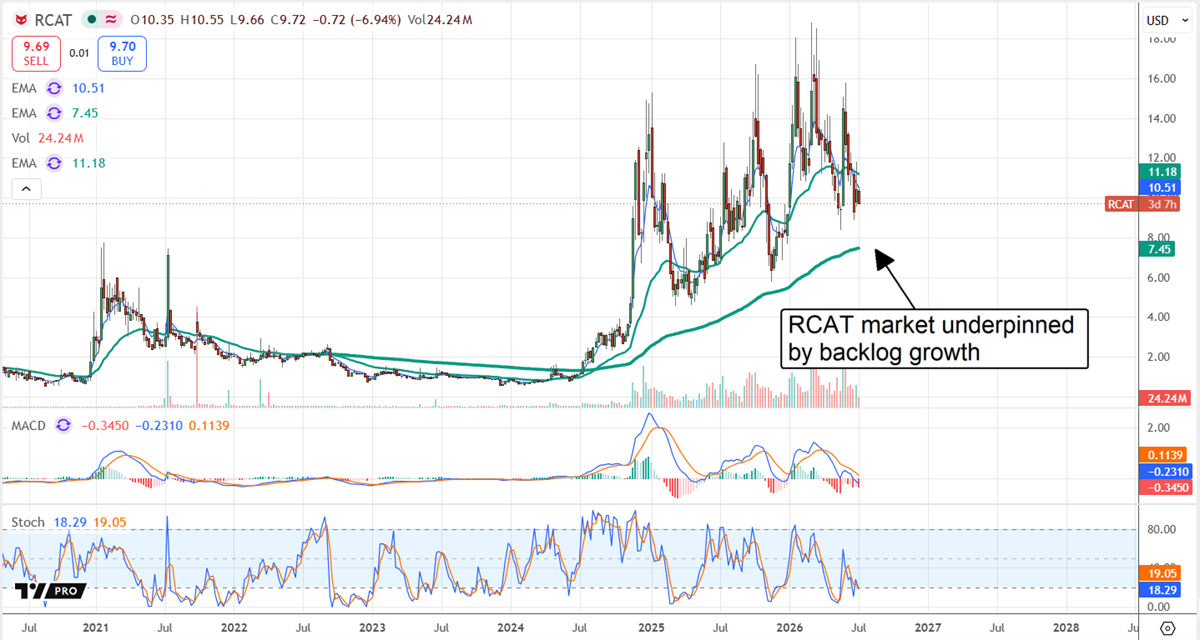

Red Cat Holdings: China Says No, So What?

Red Cat Holdings' primary hurdle is China, which banned exports of critical components to it and several other US-based companies. However, the impact may be limited, as it highlights the drone industry's primary problem and efforts to mitigate it: reliance on China.

Red Cat Holdings, for its part, is working to secure NDAA-compliant components and has, in fact, increased production rather than curbed it.

Other headwinds include shareholder dilution. The company has used share sales to bolster its balance sheet, setting it up for success. The dilution is offset by hundreds of millions in contract opportunities and disclosed allied orders, including NATO ally orders, Asia-Pacific orders, and a 173-system order tied to Japan’s Ministry of Defense. Seven analysts tracked by MarketBeat rate RCAT as a consensus Buy, with roughly 125% upside at the midpoint target.

Kratos Defense Systems Ramps Production to Match Orders

Kratos Defense Systems suffers from a combination of persistently high valuations and lumpiness linked to DoD budget award timing. The silver lining is that budget awards from the DoD and other sources continue to grow. Backlog topped $2 billion as of the end of Q1 2026, with approximately 72% funded.

The takeaway is that KTOS has a solid baseline for near-term growth, which has been accelerating and is expected to remain strong in the upcoming years. Long-term forecasts suggest revenue growth will sustain a 20%+ pace for at least the next four years, with margin expansion compounding the effect. In this scenario, the high multiple at which it trades relative to current-year forecasts could fall to more reasonable levels by the decade's end, setting the stage for share price appreciation, with only execution standing in the way.

Analysts are robustly bullish on KTOS stock. The 24 tracked by MarketBeat rate it as a consensus Moderate Buy with nearly 100% upside relative to long-term moving averages. Catalysts for the move include the Q2 earnings release expected in early August. Analysts are expecting another strong quarter with modest double-digit revenue growth and wider margins, but have lowered the bar, so outperformance is likely. Assuming another quarter of backlog growth and healthy book-to-bill ratios, these stock prices could quickly regain ground lost since their 2025 peaks.

Where Should You Invest $1,000 Right Now?

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

The article "Drone Stocks Are Down, But Defense Backlogs Tell a Different Story" first appeared on MarketBeat.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)