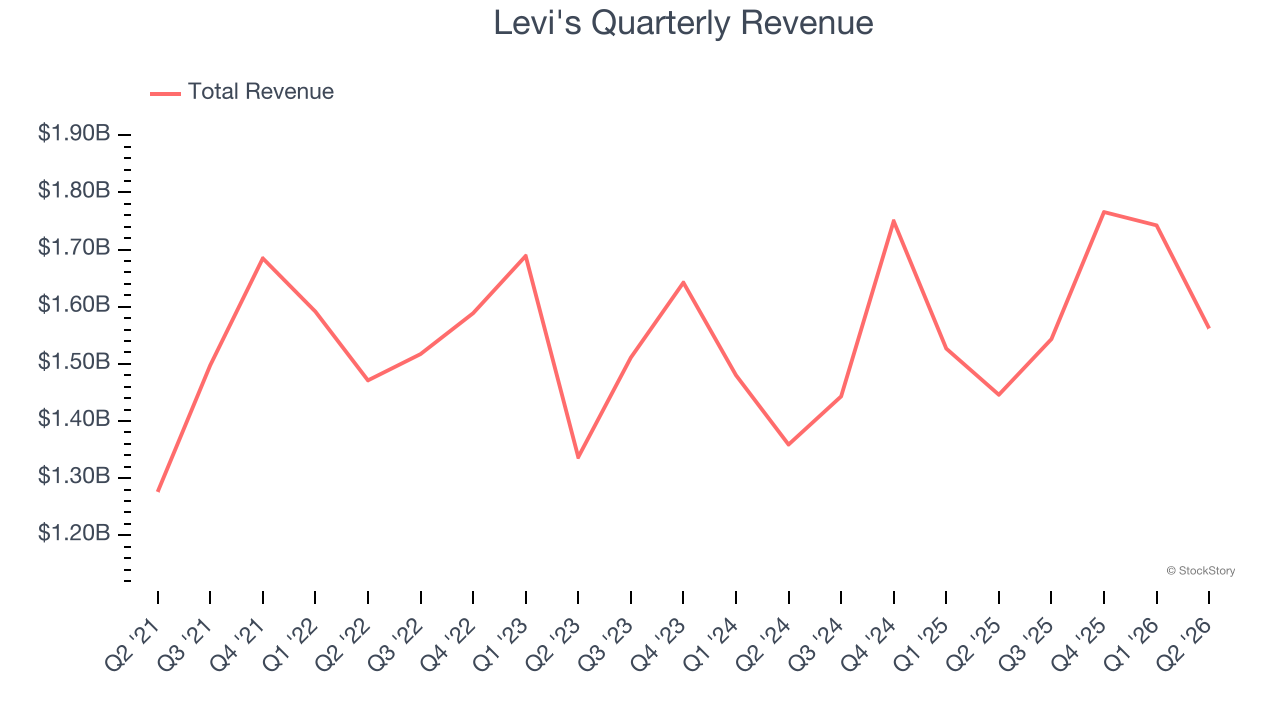

Denim clothing company Levi's (NYSE:LEVI) reported Q2 CY2026 results topping the market’s revenue expectations, with sales up 8% year on year to $1.56 billion. Its non-GAAP profit of $0.28 per share was 16.3% above analysts’ consensus estimates.

Is now the time to buy Levi's? Find out by accessing our full research report, it’s free.

Levi's (LEVI) Q2 CY2026 Highlights:

- Revenue: $1.56 billion vs analyst estimates of $1.52 billion (8% year-on-year growth, 2.9% beat)

- Adjusted EPS: $0.28 vs analyst estimates of $0.24 (16.3% beat)

- Adjusted EBITDA: $198.3 million vs analyst estimates of $185.2 million (12.7% margin, 7.1% beat)

- Management raised its full-year Adjusted EPS guidance to $1.49 at the midpoint, a 2.8% increase

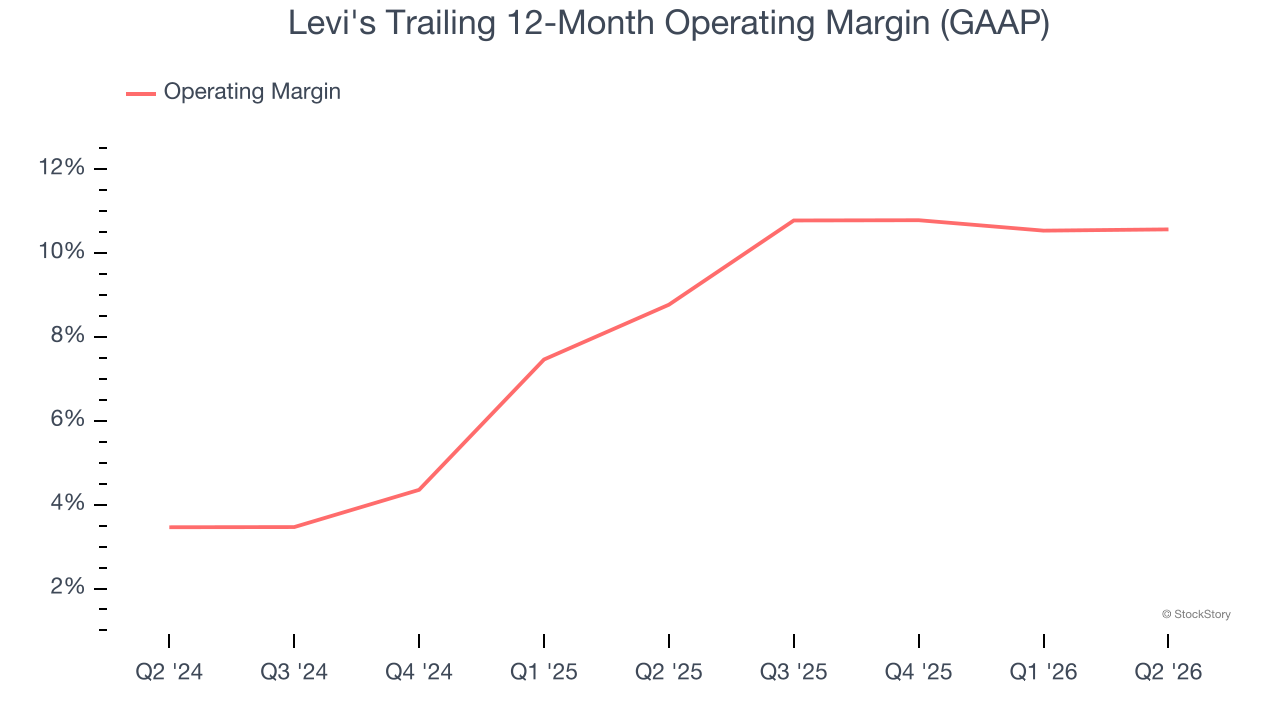

- Operating Margin: 7.8%, in line with the same quarter last year

- Free Cash Flow Margin: 14.8%, up from 10.1% in the same quarter last year

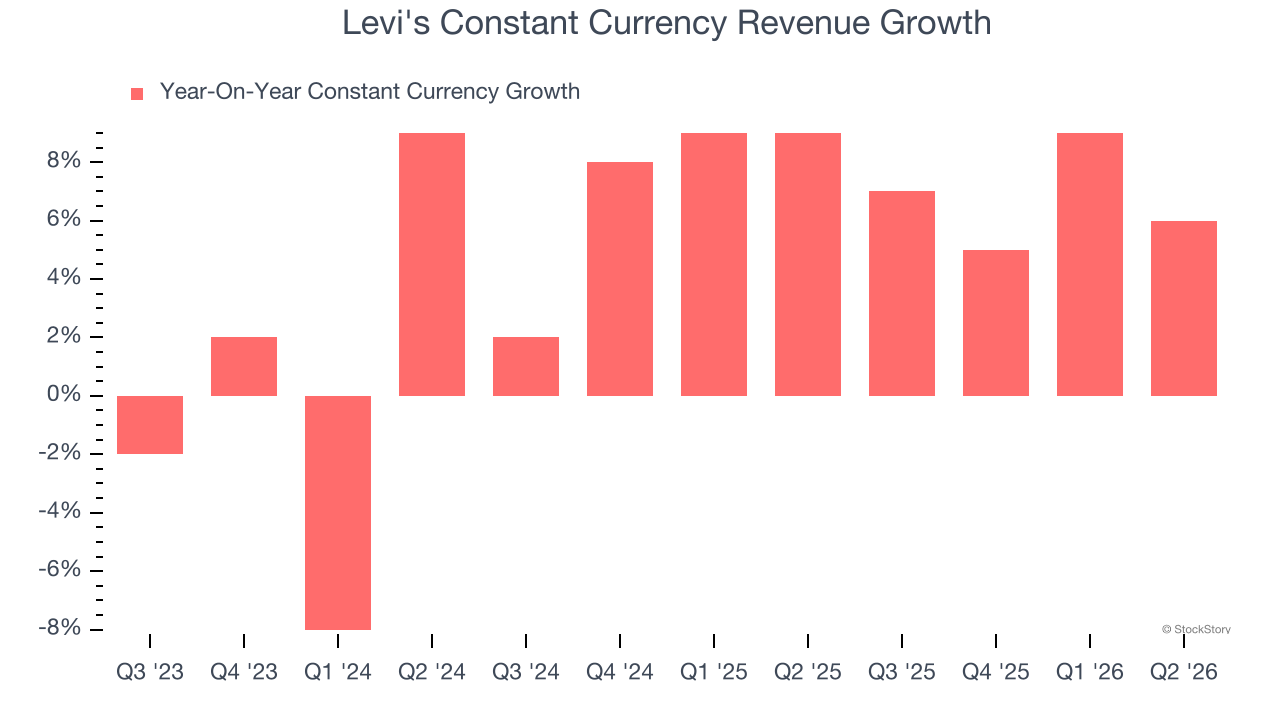

- Constant Currency Revenue rose 6% year on year (9% in the same quarter last year)

- Market Capitalization: $9.32 billion

Company Overview

Credited for inventing the first pair of blue jeans in 1873, Levi's (NYSE:LEVI) is an apparel company renowned for its iconic denim products and classic American style.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Levi’s sales grew at a weak 5.6% compounded annual growth rate over the last five years. This was below our standard for the consumer discretionary sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Levi’s annualized revenue growth of 5.1% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

We can better understand the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 6.9% year-on-year growth. Because this number is better than its normal revenue growth, we can see that foreign exchange rates have been a headwind for Levi's.

This quarter, Levi's reported year-on-year revenue growth of 8%, and its $1.56 billion of revenue exceeded Wall Street’s estimates by 2.9%.

Looking ahead, sell-side analysts expect revenue to grow 3.4% over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and indicates its products and services will face some demand challenges.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Operating Margin

Levi’s operating margin has risen over the last 12 months and averaged 9.7% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

In Q2, Levi's generated an operating margin profit margin of 7.8%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

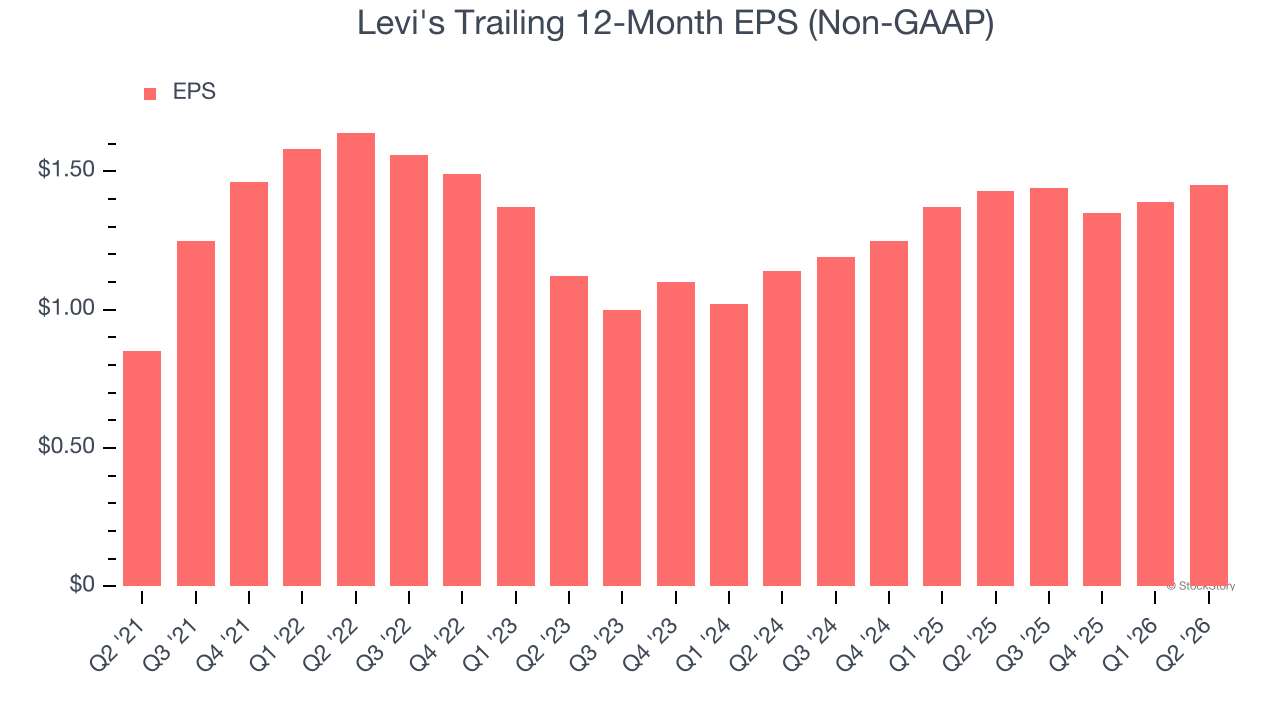

Levi’s EPS grew at 11.3% compounded annual growth rate over the last five years. This performance was better than its revenue growth but doesn’t tell us much about its business quality because its operating margin improvement was less than peers.

In Q2, Levi's reported adjusted EPS of $0.28, up from $0.22 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Levi’s full-year EPS to grow 9.1% from $1.45 to $1.58.

Key Takeaways from Levi’s Q2 Results

It was good to see Levi's beat analysts’ EPS expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Overall, this print had some key positives. The market seemed to be hoping for more, and the stock traded down 5.3% to $23.17 immediately following the results.

Is Levi's an attractive investment opportunity at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Uber%20Technologies%20Inc%20logo%20outside%20offices-by%20Sundry%20Photography%20via%20iStock.jpg)

/Space%20Technology%20by%20Rini_%20com%20via%20Shutterstock.jpg)