/JPMorgan%20Chase%20%26%20Co_%20operations%20center-by%20jetcityimages%20via%20iStock.jpg)

The U.S. banking sector has been under severe pressure from regulators for more than 15 years. Following the 2008 financial crisis and the subsequent introduction of the Dodd-Frank Act, the largest financial institutions in the United States have been placed under a regime of strict capital austerity.

The progressive tightening of requirements forced banks to "sterilize" colossal volumes of liquidity on their balance sheets. This artificially suppressed their profitability. Consequently, the sector turned into a category of outsiders that the market grew accustomed to treating with extreme caution.

However, a macro-level event happened in the first half of 2026 — something that can be qualified as a kind of tectonic shift. After fierce criticism of the initial draft of Basel III Endgame reforms, regulators decided in March to substantially reduce reserve requirements. Following that, the sector hit a critical milestone on June 18, 2026, which marked when the key 90-day period for public comment on the Basel III changes expired.

The bureaucratic machine will inevitably drag out the process of these reforms fully being enacted until 2027. But the stock market always trades on forward-looking expectations. Accordingly, the mere fact that regulators are shifting their rhetoric from "suppression" to "stimulation" represents one of the biggest victories for the banking sector in the last two decades.

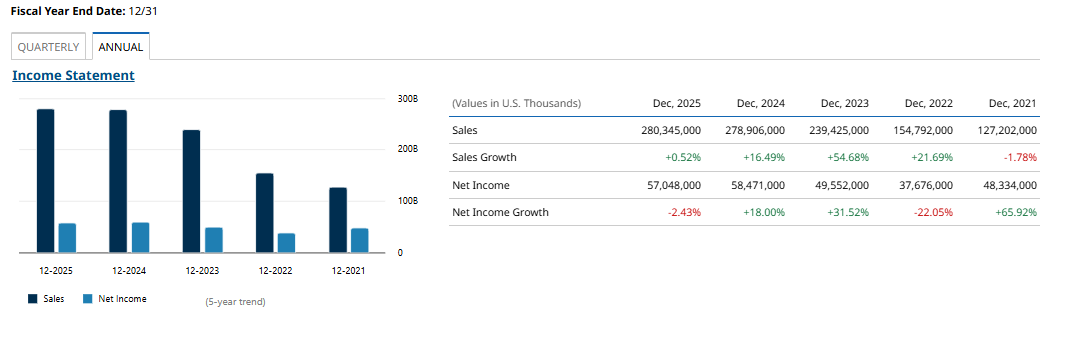

Shares of JPMorgan Chase (JPM) — a flagship of the banking industry with a market capitalization of $908 billion — have already begun reacting to this turnaround. This forms a unique entry point for investors ahead of a large-scale re-evaluation of the entire business. In my view, the fundamental growth potential of JPM stock is currently based on two powerful drivers that will reshape the bank's revenue and expense structure in the coming years.

Powerful Driver #1: Artificial Intelligence as a Margin Multiplier

Out of inertia, the market continues to perceive JPMorgan as a classic, sluggish "old" business. However, a technological revolution is taking place inside the company. JPMorgan is becoming a primary beneficiary of artificial intelligence (AI) implementation in the financial sector, with the bank's scale allowing it to invest colossal volumes of capital into AI infrastructure.

This AI expansion within the company is being realized through a radical optimization of operating expenses. Traditionally, the banking business is burdened with massive personnel costs in areas like compliance, customer support, and the back office, where billions of dollars are spent annually. But AI deployment can allow for automated document processing, legal auditing, and control. This kind of synergy will inevitably lead to a qualitative improvement in the cost-to-income ratio.

Furthermore, AI is executing a true revolution in underwriting. Algorithms analyze huge amounts of unstructured data in real time, minimizing the probability of defaults on new loans. As a result, banks like JPMorgan will likely be able to afford an aggressive credit expansion without risking degradation in asset quality.

Powerful Driver #2: The Compressed Spring of the Loan Portfolio

The second fundamental argument in favor of a long-term purchase of JPM stock lies in overcoming the imbalance between nominal U.S. GDP and lending volumes.

In the wake of the pandemic, the U.S. economy went through an inflation cycle that led to powerful growth in nominal gross product. At the same time, due to high Federal Reserve interest rates and tight internal risk-management limits imposed by Basel III, the real credit portfolios of the largest banks grew significantly slower than the economy. That resulted in a relative contraction of leverage.

Now, we are seeing the effects of a sort of "compressed spring." The nominal volume of the economy is huge. Businesses have fully adapted to new prices, but the lending base lags behind. Easing Basel III requirements will give JPMorgan Chase the ability to unlock capital. The bank will no longer need to hold redundant billions of dollars in sterile collateral accounts, meaning the money will flood into the real sector. What's more, even if the Fed interest rate remains high for a long time, it will likely not become an obstacle for JPMorgan, as the removal of regulatory barriers should provide lending with a new impulse regardless.

Still, investors should take associated risks into account. First, a potential new bout of inflation remains a threat, under which the Fed would be forced to pursue a sharp interest rate hike — potentially by more than 100 basis points. This possibility could trigger a wave of defaults. Secondly, there is the risk of a hard recession. In the event of a deep economic downturn, corporate demand for loans will collapse, completely neutralizing the positive effect of the fresh Basel III changes.

Nevertheless, given the current macroeconomic picture and the historical resilience of JPMorgan's balance sheet, the probability of a catastrophic scenario looks moderate. The balance of risks is clearly skewed toward stable growth.

Conclusion

JPMorgan stands on the threshold of a powerful transformation. The fundamental reversal of the regulatory trend, which will give the green light for unlocking capital, perfectly coincides with a technological breakthrough in the area of AI automation.

To evaluate JPM stock on only retrospective data would mean missing out on its future potential. As synergy from extensive growth in lending and an intensive reduction in costs begins to be fully reflected in quarterly reports, Wall Street will likely be forced to radically re-evaluate shares. In my view, JPM stock offers an excellent opportunity for long-term investors looking to bet that the largest U.S. banks will reclaim their status as the prime market-profit generators.

On the date of publication, Mikhail Fedorov did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/Chipset%20held%20over%20rush%20hour%20traffic%20by%20Jae%20Young%20Ju%20via%20iStock.jpg)