AI infrastructure demand is picking up fast as companies race to get more computing power. Data centers are already pushing power systems to their limits, which is why there is growing attention on energy and cooling providers like Vertiv Holdings Co. (VRT), GE Vernova (GEV), Eaton Corporation plc (ETN), Bloom Energy Corporation (BE), and Constellation Energy Corporation (CEG).

Even smaller players are shifting focus, like Blockchain Digital Infrastructure Ltd., which is rebranding to AIB Data Centers (AIB) to lean into the trend. All of this points to a clear need for more advanced, high-density systems that can handle performance while keeping power and cooling in check.

Nvidia Corporation (NVDA) is still at the center of it all, supplying the GPUs and platforms behind most of this buildout. Its Kyber rack-scale system is meant to play a big role in future AI training and high-performance computing.

However, reports say Nvidia will delay its Kyber rack-scale architecture by more than 12 months, pushing it out to 2028. Even with that news, NVDA shares were still slightly up as of Monday morning.

So what does this delay really mean for Nvidia's growth and where the stock could go next?

Investors Shrug Off the Delay

Nvidia designs the chips and systems behind much of today’s AI growth, from data centers to edge devices. So when reports came out that its Kyber rack-scale architecture is being pushed to 2028, you might expect the stock to drop. But that did not happen.

Shares were slightly up Monday morning, adding to a solid run that has seen Nvidia gain 24.1% over the past year and 6.4% so far this year.

Part of that steady reaction comes down to valuation. Nvidia trades at a forward price-to-earnings of 22.49 times, which is actually below the sector average of 24.77 times, meaning investors are not overpaying for a company that is still growing much faster than most of its peers.

The financials help explain why investors are staying confident. In Q1 fiscal 2027, Nvidia reported record revenue of $81.6 billion, up 85% year-over-year (YOY). Data center revenue alone reached $75.2 billion, rising 92%. Margins stayed strong too, with gross margins at 74.9% on a GAAP basis and 75.0% non-GAAP. Earnings came in at $2.39 per share GAAP and $1.87 non-GAAP.

Looking ahead, the company expects Q2 revenue of about $91.0 billion, plus or minus 2%. Gross margins are expected to stay around 74.9% to 75.0%, while operating expenses are projected at about $8.5 billion GAAP and $8.3 billion non-GAAP.

Why the Delay May Not Hurt

The holdup comes down to manufacturing issues with the complex circuit board midplane that handles high-speed connections inside Nvidia's Kyber NVL144 rack-scale system. That problem caused a delay of more than 12 months, pushing the target launch to 2028. Some reports also say an alternative NVL72x2 design was scrapped and larger setups are being held back by optical component limits. Nvidia has pushed back on those timeline worries, saying its broader AI chip roadmap is still on schedule.

The delay probably will not sting much. Nvidia is still putting up huge numbers from its current products, and the AI infrastructure buildout is not slowing down. Partners have already built out supporting tech like 800V HVDC power systems and compact PSU designs made specifically for Kyber's liquid-cooled, blade-rack setup. Demand for existing high-density racks is still strong as hyperscalers keep pouring money into data centers and power infrastructure.

Importantly, timing matters most. Near-term sales and profits should not take much of a hit since older platforms are still selling well. Further out, the delay might give rivals a small window in large-scale deployments, but Nvidia's massive ecosystem, the progress on its Rubin platform, and its strong grip on AI factories mean it still has a lot of room to grow.

Analysts Still Back Nvidia

Nvidia reports earnings next on August 26. For the current quarter ending July 2026, analysts see earnings coming in at $2.01 per share, more than double last year’s $0.99, which points to 103% growth. For the full fiscal year 2027, estimates sit at $8.69, marking a 90.2% jump from the prior year.

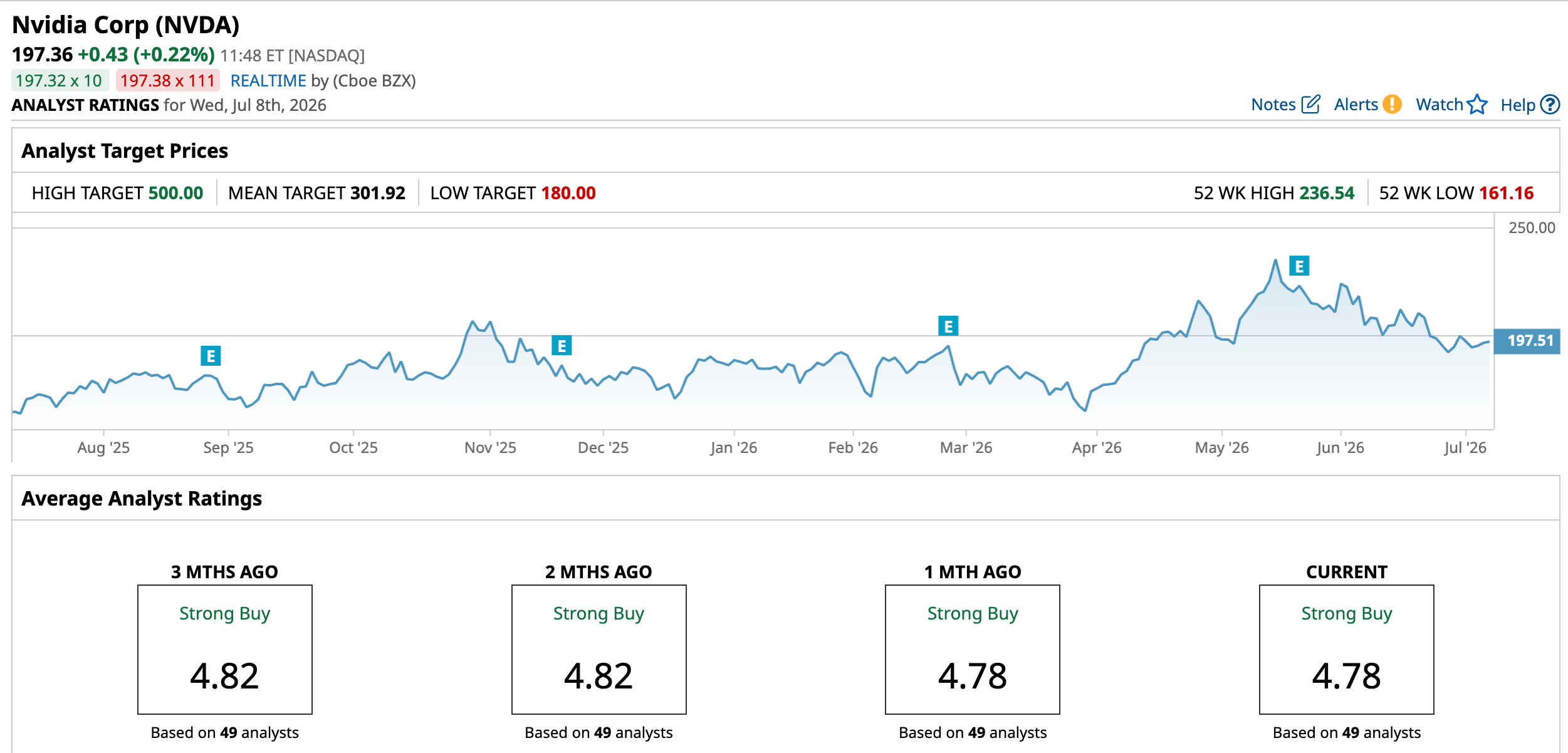

In June, Morgan Stanley kept its “Overweight” rating on Nvidia and held a $288 price target, calling it its top pick in the processor space. The firm pointed to Nvidia’s leading position across several product areas as a key reason it still sees strong value.

Around the same time, Truist Securities also maintained its “Buy” rating and $307 target after the company introduced new AI-focused products, showing continued confidence in its long-term growth story.

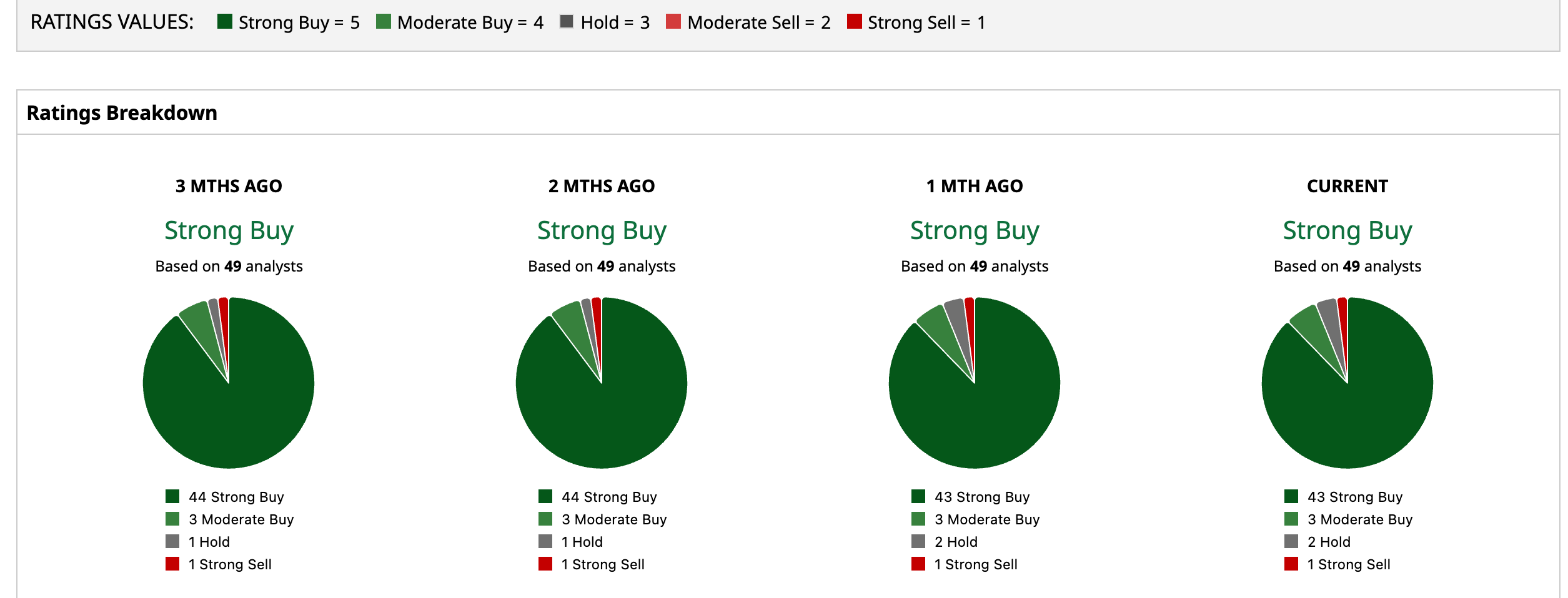

Across the board, 49 analysts have a “Strong Buy” consensus. Their average price target is $301.92, implying 53% upside from current levels.

Conclusion

Nvidia’s Kyber delay is a headline worth watching, but it does little to dent the company’s near-term momentum. With record revenue, massive earnings growth, and strong analyst support, the stock’s resilience makes complete sense. The bigger picture is that AI infrastructure spending is still accelerating, and Nvidia remains the dominant supplier powering that buildout. As long as the Rubin platform stays on track and data center demand holds firm, shares look more likely to grind higher toward that consensus price target than to stall out over a 2028 architecture shift.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)

/Johnson%20%26%20Johnson%20location%20sign-by%20JHVEPhoto%20via%20iStock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)