Buckle up; the markets are about to get a whole lot more volatile as President Trump suggests the ceasefire with Iran is over.

In midmorning European trading, Brent crude and West Texas Intermediate futures rose by 6% and 6.2%, respectively. As a result, the S&P 500 is down 0.58% in Wednesday morning trading, with the VIX volatility index up 8.25% to 17.46.

The good news is that the markets have been relatively resilient despite the four-month war with Iran. Since Feb. 28, when the bombs first started dropping, the S&P 500 is up over 9%.

In yesterday’s trading, 125 stocks on the NYSE hit new 52-week highs compared to 24 new 52-week lows. Meanwhile, on the Nasdaq, the ratio was 206 to 146.

Although there weren’t too many quality stocks to be found in the new 52-week lows, Ollie’s Bargain Outlet Holdings (OLLI) caught my attention. The discount chain hit its 33rd new 52-week low of the past 12 months, putting it down over 47% in the past year.

While the technical indicators aren’t pretty, aggressive investors might want to ignore them and consider a contrarian bet on Ollie’s stock. Here’s why.

The Technicals Aren’t Pretty

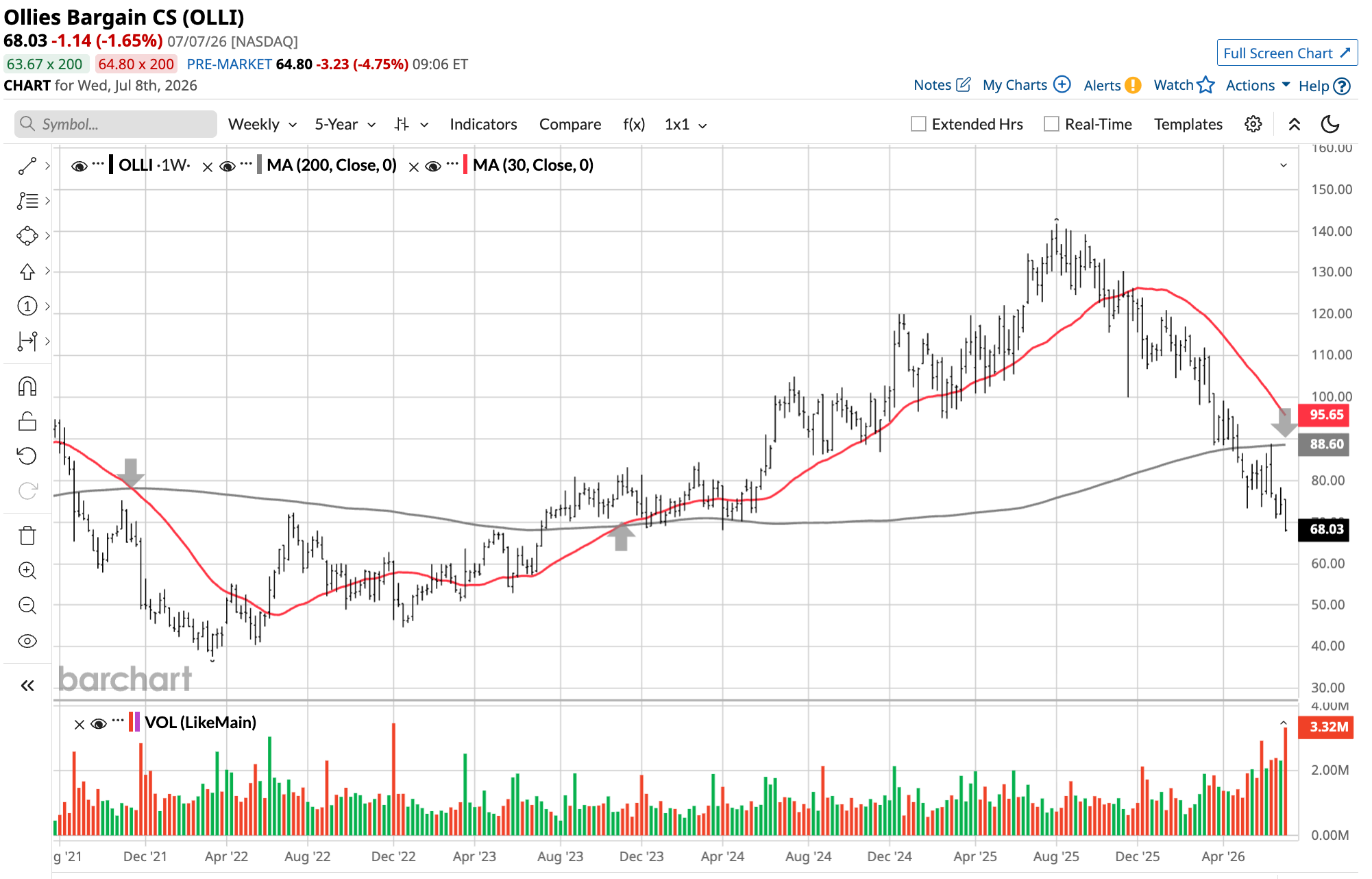

I’m not a technical analyst, but when looking at a 5-year chart, it’s hard not to think the stock is likely to keep moving lower through the summer and into the fall.

In November 2021 (the down arrow on the left side of the chart), the 30-day moving average crossed below the 200-day MA. The “Death Cross,” as it’s called, led to a further drop in its share price five-and-a-half years ago. Two years later, the 30-day MA crossed above the 200-day MA (the middle arrow up). The “Golden Cross” sent OLLI on a two-year tear to a July 2025 all-time high of $141.74. Finally, the downward-pointing arrow on the right side of the chart suggests another death cross could occur sometime later this summer or into the fall.

So, the question is not when, but how long the 30-day MA will remain below the 200-day MA? The 30-day MA in the first death cross stays below the 200-day MA for two years. However, the share price bottomed after just four months, so even if the death cross happens in September, the worst may be over by the end of the year.

The Barchart Technical Opinion for OLLI, however, is currently a 100% Strong Sell. Given the possible resumption of the war in Iran and lower stock prices ahead, it makes sense for aggressive investors to wait on buying the discount retailer’s stock until the geopolitical situation stabilizes.

Against a less-than-flattering background, there are reasons to be optimistic about Ollie’s future share price.

Same-Store Sales Growth Still Positive

OLLI stock has had an interesting five weeks since announcing its Q1 2026 results on June 3. Despite announcing a 21.3% year-over-year increase in earnings per share, four cents above Wall Street’s expectations, the shares fell after the results were released due to investor concerns about softening sales.

The stock battled back in mid-June, but it’s been mostly downhill since. This morning, JPMorgan downgraded OLLI to Neutral from Overweight, cutting its 12-month price target to $70. As I write this in morning trading, it’s off nearly 5%.

As a glass-half-full person, the fact that it delivered same-store sales growth of 1.7% in Q1 2026 is something to be happy about if you’re an Ollie’s shareholder. Sure, it was down from 2.7% a year ago, but it was positive.

Now, the retailer’s outlook for fiscal 2026 (January year-end) is for same-store sales to grow by 2%, down from 3.7% growth in 2025, but again, it’s positive, and the share price reflects the contraction over the past year.

Not only have same-store sales remained positive, but it’s also expected to open 75 new stores in 2026, down slightly from 2025, bringing its store footprint to 720 by the end of the year, with revenue of nearly $3 billion, 13% higher than in 2025.

Furthermore, it finished the first quarter with 17.5 million Ollie’s Army loyalty members, 12.6% higher than a year ago. Members account for 80% of the retailer’s sales. Adding 500,000 new members in a quarter is very positive.

All of this leads to a business that continues to grow its bottom line. In 2026, it expects to grow its adjusted net income by 17%, to $4.50 per share from $3.86.

The retailer has commendably consistent gross margins. In 2025, they were 40.5%, the highest they’ve been since 2017. That reality should make potential buyers of its stock more confident about future profits, even if there is some doubt about top-line growth.

Ollie’s Valuation Is Too Low

Based on Ollie’s 2026 EPS estimate, OLLI stock trades at 14.1 times that estimate. That’s lower than at any time in the past decade.

It’s no surprise then that Ollie’s repurchased $53.4 million of its shares in the first quarter at an average price of $98.44. Of course, we know in hindsight that its shares have fallen considerably from that average.

No matter, with nearly $200 million in free cash flow in the 12 months ended May 3, and net cash of $390 million, it has plenty to do more buying in the second quarter and beyond. It has $205 million left on its current share repurchase plan.

Can it get back to its $141.74 all-time high? It can, but not this year, or likely next either. But the 2028 estimate is $5.08, giving it a forward P/E of 27.9x based on its all-time high. Before 2022, Ollie’s forward P/E was routinely in the mid-to-high 20s or low $30s.

That would be a 125% return over 30 months, or a 50% annualized return.

I like its chances.

On the date of publication, Will Ashworth did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)

/Johnson%20%26%20Johnson%20location%20sign-by%20JHVEPhoto%20via%20iStock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)