/Solar%20panels%20on%20sunny%20day%20by%20andreas160578%20via%20Pixabay.jpg)

Enphase Energy (ENPH) recently soared amid rumors that President Donald Trump's administration is considering limiting the use of China-made power inverters due to national security issues. The restrictions could dramatically change the competitive landscape of one of the most crucial components in residential solar panels, pushing up the stocks of companies engaged in the sector as a result.

However, the question of whether the industry will see any demand recovery remains unanswered. While Enphase would likely be one of the main winners if restrictions are placed on Chinese competitors, the firm still needs to overcome slower residential demand, shifting tax policies, and rising interest rates. Let's take a closer look.

About Enphase Energy Stock

Enphase Energy creates microinverters, energy storage, electric vehicle (EV) charging, and energy management software solutions for residential solar panels. Headquartered in Fremont, California, the company has a market capitalization of about $5.8 billion.

Although ENPH stock experienced a strong run recently, shares still trade well below their all-time highs. At the moment, ENPH stock is down about 42% from its 52-week high of $73.74, although it is also up roughly 67% from the 52-week low. Higher financing costs have hit residential solar panel demand, which is reflected in Enphase Energy stock's weak performance over the last year.

In terms of valuation, ENPH stock trades at around 3.8 times sales and 50.5 times forward earnings. These multiples look too expensive for a firm like Enphase, which is seeing revenue drop. In my view, this premium would only be justified if the company returns to growth in the coming quarters.

The rumored Chinese inverter restrictions could help with this. In contrast to many other players in the segment, Enphase manufactures a lot of its products in Texas and South Carolina, so it would get an advantage if imports from China are restricted.

Enphase Energy Misses on Earnings But Builds a New Growth Story

In the first quarter of 2026, Enphase reported revenue of $282.9 million, which was lower sequentially compared to $343.3 million in Q4 2025. The company also delivered non-GAAP EPS of $0.47, while free cash flows were decent at $83 million. Enphase ended the quarter with $930.6 million in cash and equivalents.

Management cited the expiration of the federal residential clean-energy tax credit “under Section 25D of the Internal Revenue Code” and typical seasonality as factors behind the disappointing figures. Residential sell-through demand in the U.S. fell 48% sequentially and 18% year-over-year (YOY).

On the other hand, the company emphasized another potential opportunity in the report. Specifically, Enphase Energy recently launched development of the IQ SST platform, a distributed solid-state transformer product for artificial intelligence (AI) data centers. Although the product is still under development, it should help expand Enphase's addressable market beyond the residential segment and potentially create another growth driver.

Meanwhile, if restrictions are set on Chinese inverters, Enphase will have the opportunity not only to get political support but also potentially enter the infrastructure market.

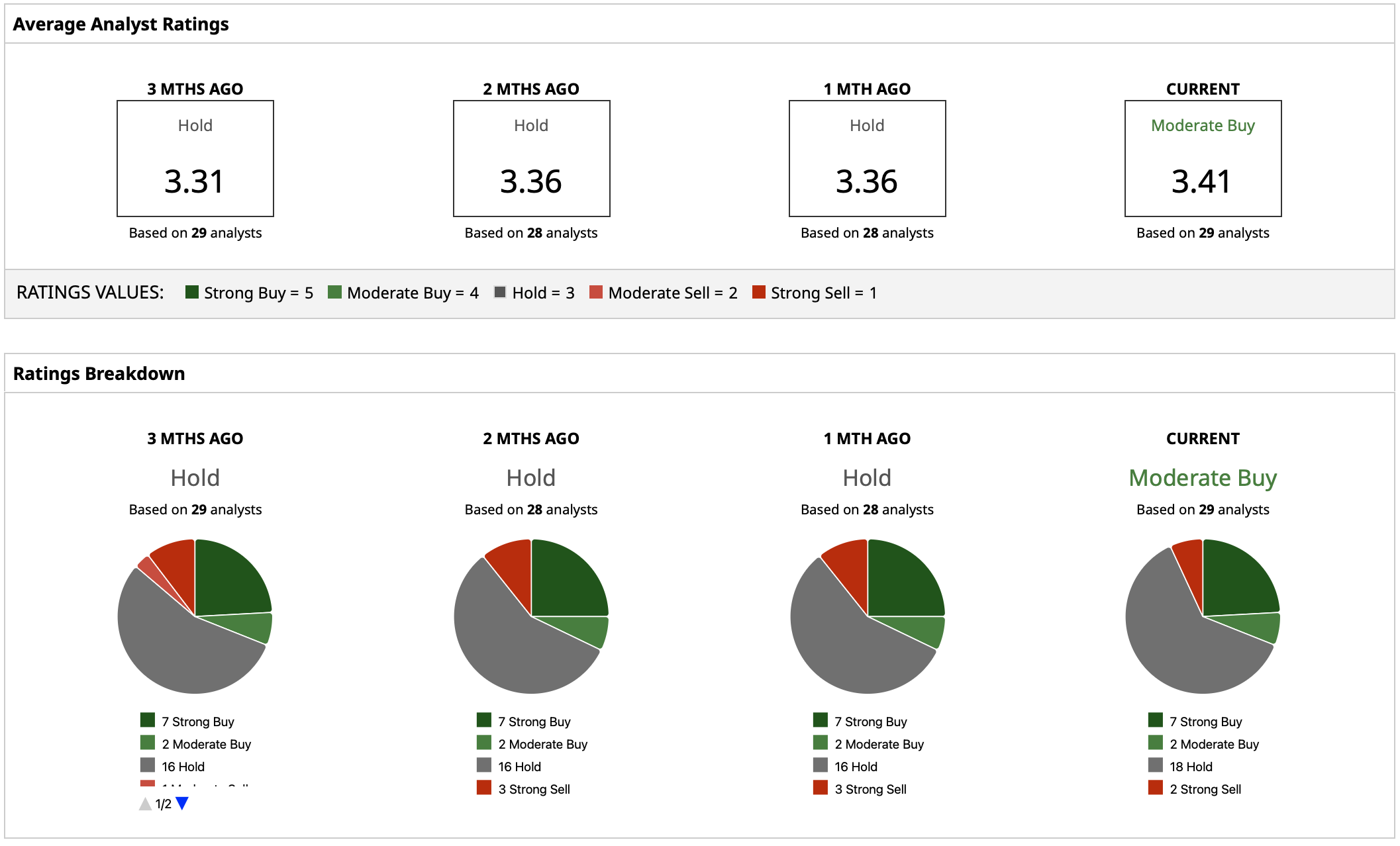

What Do Analysts Expect for ENPH Stock?

Analysts are positive on ENPH stock with a consensus “Moderate Buy” rating and a mean price target at $46.68. Although this target is only slightly higher than current levels, it still reflects potential upside of more than 8% from here.

That said, Enphase has an important problem to solve in terms of demand. If there is a recovery in residential installations, and an inherent competitive advantage arises for domestic firms due to a policy shift, the current valuation may become justified.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)

/Johnson%20%26%20Johnson%20location%20sign-by%20JHVEPhoto%20via%20iStock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)