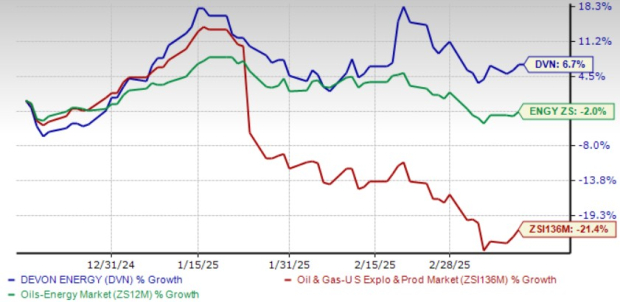

Devon Energy Corporation’s DVN shares have gained 6.7% in the past three months, outperforming the Zacks Oil & Gas- Exploration and Production- United States industry’s decline of 21.4% and the broader Zacks Oil and Energy sector’s decline of 2%.

While the three-month performance paints a positive picture for investors, looking at the past one-year performance is crucial for a fuller understanding. DVN’s stock has declined 26.7% in the past year, suggesting that it is on a gradual path to recovery. Another stock from the same industry, EQT Corporation EQT, registered a 43.9% gain in share price in the past year.

Price Performance (Three Months)

Image Source: Zacks Investment Research

Should you consider adding DVN stock to your portfolio only based on positive price movements? Let’s delve deeper and find out factors that can help investors decide whether it is a good entry point to add the stock to their portfolio.

Factors Acting as Tailwind for DVN Stock

Devon Energy has a multi-basin portfolio consisting of high-margin oil and gas assets. The assets DVN owns have significant long-term growth potential. The company continues to expand its asset holdings through strategic acquisition.

The acquisition of the Williston Basin business of Grayson Mill Energy has increased DVN’s net acre position in Williston Basin to 430,000 acres from 123,000 acres while production volume is expected to triple to 150,000 barrels of oil per day (Boe/d) from 50,000 Boe/d from this region, The acquired assets has started to contribute to DVN’s production volumes and will continue to do so in the long-run.

Devon Energy also has a diverse commodity mix, with a balanced exposure to oil, natural gas and natural gas liquids production volumes. The company continues to evaluate opportunities to add more high-quality resources to its portfolio. Courtesy of DVN’s exploration initiatives, in 2024, the company achieved a production replacement rate of 154%. The strong reserve addition will allow the company to maintain its production volumes over a long period.

A low-cost operating structure boosts the company’s margins. DVN has been reducing its costs by selling higher-cost assets and bringing new lower-cost production assets online. Devon Energy is also working to reduce its drilling and completion costs and is better aligning personnel with the go-forward business.

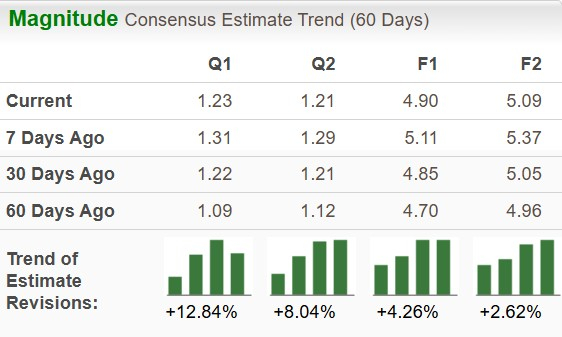

Devon Energy’s Earnings Estimates Move Up

The Zacks Consensus Estimate for Devon’s 2025 and 2026 earnings per share has moved up 4.3% and 2.6%, respectively, in the past 60 days.

The Zacks Consensus Estimate for 2025 and 2026 earnings per share of its peer Occidental Petroleum OXY has gone up by 12.8% and 2.6%, respectively, in the past 60 days.

Image Source: Zacks Investment Research

DVN Stock’s Earnings Surprise

The company’s earnings in the last four reported quarters were better than estimates. Devon Energy reported an average positive earnings surprise of 8.63% in the last four quarters.

Image Source: Zacks Investment Research

Devon Energy Raises Value of Shareholders

The company has been operating in a manner that generates sustainable free cash flow. It is utilizing cash flow to reduce outstanding debts, pay dividends and buy back shares. The company generated free cash flow in the last 17 straight quarters.

Devon Energy’s management raised quarterly dividends by 9% for the first quarter of 2025. The new quarterly rate will be 24 cents per share. The company’s capital allocation will now focus on strengthening the balance sheet and returning capital to its shareholders through fixed dividends and share buybacks. It repurchased shares worth $301 million in the fourth quarter of 2024. Subject to the approval of the board, Devon Energy might buy back shares in the range of $200-$300 million per quarter of 2025.

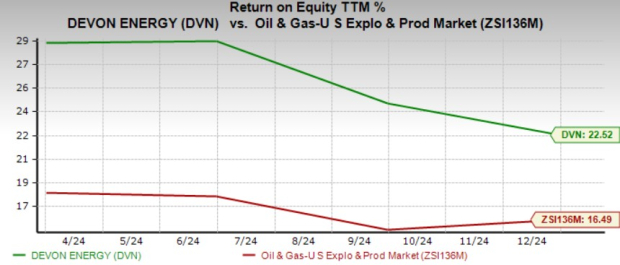

DVN Stock Returns Better Than Industry

Devon Energy’s return on equity (ROE) has outperformed the industry average in the trailing 12 months. ROE of DVN was 22.52% compared with the industry average of 16.49%. The company has been investing shareholders’ funds effectively in profitable projects compared to its peers in the industry, which is evident from its ROE.

Image Source: Zacks Investment Research

DVN Shares Are Trading at a Discount

Devon Energy’s shares are inexpensive on a relative basis, with its current trailing 12-month Enterprise Value/Earnings before Interest Tax Depreciation and Amortization (EV/EBITDA TTM) being 4.09X compared with its industry average of 11.44X.

Image Source: Zacks Investment Research

Wrapping Up

Devon Energy continues to have a very strong portfolio of high-quality assets. The strategic acquisitions and contribution from its multi-basin assets boost production volumes. The company has a balanced exposure to oil, natural gas and NGL production, which adds to its advantage.

The rising earnings estimates, positive share price movement in the past three months and ROE better than the industry, investors can consider adding the stock to their portfolio as it currently has a VGM Score of B and is trading at a discount.

Devon Energy currently carries a Zacks Rank of 2 (Buy).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +24.3% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Devon Energy Corporation (DVN): Free Stock Analysis Report

Occidental Petroleum Corporation (OXY): Free Stock Analysis Report

EQT Corporation (EQT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

/Technology%20abstract%20by%20TU%20IS%20via%20iStock.jpg)