/A%20SoFi%20logo%20on%20an%20office%20building%20by%20Tada%20Images%20via%20Shutterstock.jpg)

Ark Invest’s Cathie Wood is known for her bold stock picks and backing companies that she invests in. Earlier this week, her flagship Ark Innovation ETF (ARKK) added positions in fintech stocks like Robinhood (HOOD), Coinbase (COIN), Circle (CRCL), and SoFi (SOFI).

Notably, after outperforming the markets by a handsome margin for three consecutive years, SoFi has had a rough ride in 2026. While the shares have gained over 23% from their 2026 lows, they are down over 30% for the year. Incidentally, it's not only Wood who sees value in this beaten-down fintech stock; SoFi CEO Anthony Noto has also been accumulating shares through open-market purchases.

Most recently, he bought 13,888 shares at $18.06 last month, which took his direct stake to almost 12 million shares. A CEO raising his “skin in the game,” particularly when chips are down, sends a positive signal to the market. In my previous article, I noted that SoFi looked like a bargain following the Iran peace deal. As I have been arguing, the peace in the Middle East would always be fragile, and there are risks of occasional flare-ups. However, it's in the interest of both the U.S. and Iran to tone down the rhetoric. Markets have read the sign, as reflected in energy prices, with crude oil dipping to levels last seen before the conflict began earlier this year.

SOFI Stock Forecast

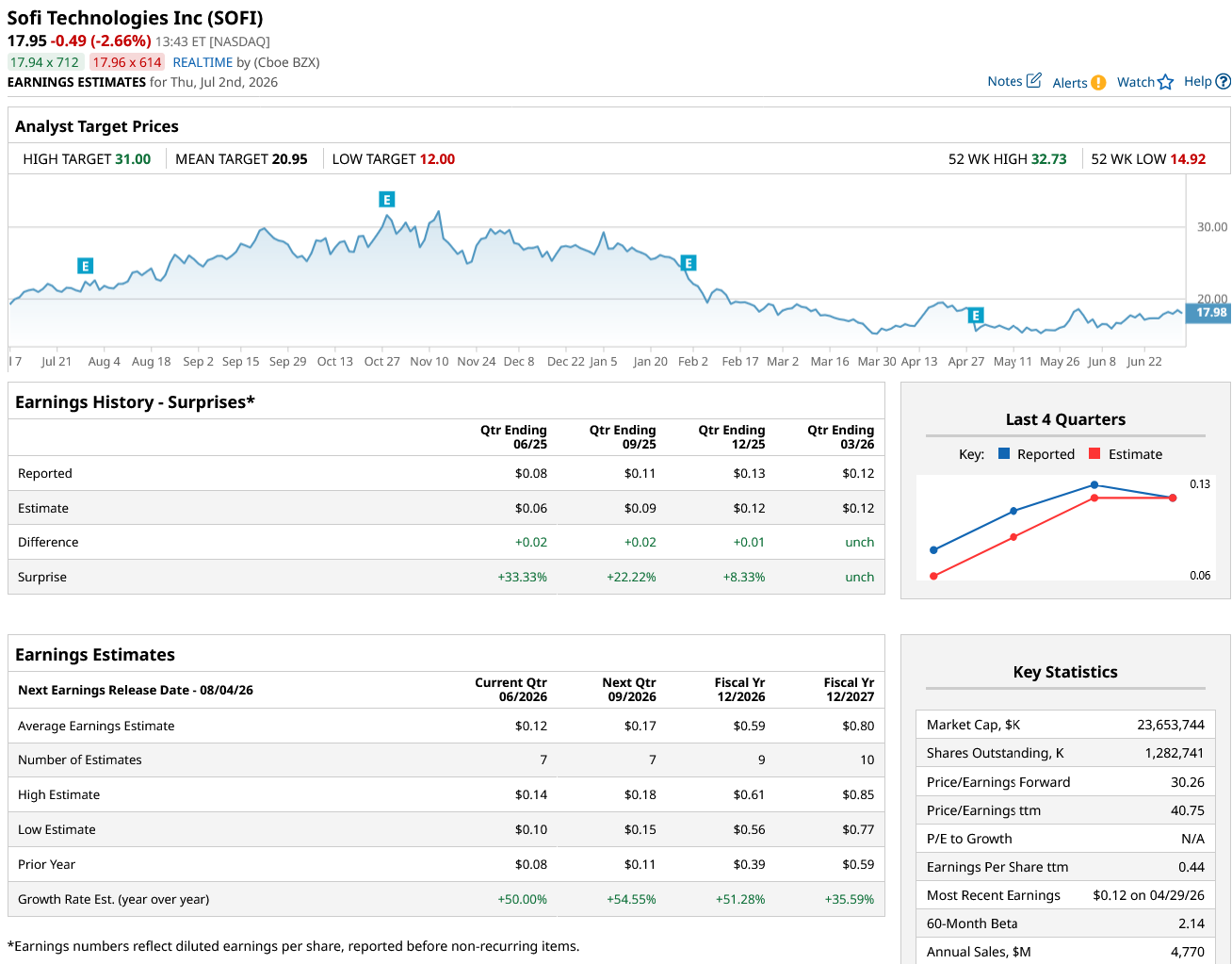

Meanwhile, even though Noto and Wood see value in SoFi, analysts have a differing view. Brokerages have gradually lowered SOFI stock’s target price over the last couple of months, particularly following the company’s Q1 2026 earnings in April. While SoFi reported better-than-expected earnings in the March quarter, it did not raise its annual guidance, which some read as a sign that the company expects the business to weaken in the back half of the year. Overall, SoFi has a consensus rating of “Hold” from the 26 analysts polled by Barchart. Its mean target price of $20.95 is 13.6% higher than the closing prices on July 1, 2026.

SoFi's Business Model Is Attractive

I, however, find SoFi’s business model quite attractive. The company focused on student loans in the initial years but has since branched out to different financial products. It also has a bank charter, which has helped it reduce funding costs and reduce reliance on high-cost wholesale borrowings.

SoFi keeps adding new loads of members every quarter and ended Q1 with a total of 14.7 million members. The company added over a million new members each in the previous two quarters and expects at least 30% annual growth in its member count this year. These members are the growth funnel for SoFi, and the company can then cross-sell them more products from its arsenal of ever-rising products.

Most recently, it started a loan program for small business owners. While that business might not move the needle much for SoFi, at least in the near term, a growing portfolio of products makes SoFi’s platform stickier for its members.

Cross-selling has incidentally been key to SoFi’s success, and the cross-sell rate increased to 43% in Q1 as compared to 40% in the previous quarter. Its SoFi Plus subscription is also fueling cross-buying, with the management pointing out during the Q1 earnings call that half of the people signing up for the subscription also buy another product on its platform.

Additionally, while SoFi has a lending business of its own and offers products like personal and home loans, it also operates a loan platform business (LPB) that originates personal loans for third parties. These are customers who don’t meet SoFi’s credit standards, but by originating loans for other lenders, SoFi gets low-risk, high-margin revenues. These members are also cross-sell targets for SoFi. There is also the tech platform business, and while it lost a major client in Chime, the company has been expanding its capabilities through acquisitions.

SOFI Stock Still Looks Like a Buy

SoFi’s valuation multiples have expanded amid the rally over the last month. It now trades at a price-to-book multiple of 2.13x. The multiples might be higher than what traditional banks trade at, but I believe they are reasonable for a high-growth company like SoFi, whose tech and loan platform segments warrant a much higher multiple given their asset-light business model.

The forward price-to-earnings (P/E) multiple of 40.75x also looks attractive, especially as the company's earnings are expected to rise by over 51% in 2026 and 35% in 2027. There are genuine concerns over the sustainability of SoFi’s growth as the company cannot keep adding a million members and growing its topline in the 30s every quarter, but I believe the fears are overblown and the company has ample scope to grow, particularly through cross-selling and international expansion.

Overall, I am on the same page as Noto and Wood and see value in SOFI stock at these levels.

On the date of publication, Mohit Oberoi had a position in: SOFI, ARKK. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)