/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

New managed services for cloud governance and continuous compliance are launching to cover multi-cloud environments, including Microsoft Corporation's (MSFT) Azure, with a focus on data residency and regulatory requirements in hybrid setups.

Microsoft is building out capabilities under its AI sovereignty vision, creating ecosystems that span AI agents, platforms, and data control. Businesses want systems that let them keep innovating while staying on top of regulations as AI use grows.

Kyndryl Holdings (KD) stepped into this on July 1, announcing an expansion of its Sovereignty Solutioning in partnership with Microsoft. The collaboration pairs Kyndryl’s mission-critical services with Microsoft Sovereign Cloud capabilities, including Azure public cloud and Azure Local for private and hybrid environments, to support data residency, compliance, and AI workloads. Shares of KD rose 6.10% to close at $12.00 on the announcement day.

Does this partnership help Kyndryl Holdings grab real growth in sovereign cloud and AI work, or will older business issues hold it back? Let’s find out.

Breaking Down KD’s Financials

Kyndryl Holdings is the world’s largest provider of mission-critical IT infrastructure services. It helps big companies manage and update their applications, data, AI, cloud, and core systems with consulting, setup, and day-to-day management.

The stock has taken a beating lately. It’s down 71.1% over the past 52 weeks and 53.9% year-to-date (YTD).

Even so, the numbers look cheap. The forward price-to-earnings is 7.34 times versus the sector’s 24.85 times.

Results are mixed. For the quarter ended March 31, 2026 (Q4 FY2026), revenue came in at $3.8 billion, down 1% year-over-year (YOY) on a reported basis and 5% in constant currency, landing right in line with Wall Street estimates. Adjusted earnings per share of $0.18 missed the $0.47 consensus, but adjusted EBITDA reached $688 million, beating forecasts for an 18.3% margin.

Free cash flow improved to $388 million from $353 million a year earlier, even as cash from operations fell. For the full fiscal year, sales totaled $15.092 billion, flat on a reported basis but down 3% in constant currency. Adjusted pretax income rose 21% to $581 million, and adjusted EBITDA grew 6% to $2.672 billion with a 17.7% margin. These gains came largely from Kyndryl Consult revenue jumping 18% and hyperscaler-related business nearing $2 billion, up 59% YOY.

The Case for Stronger Fundamentals

Kyndryl has also been deepening its partnership with Amazon.com (AMZN) through a multi-year agreement focused on helping customers move and scale AI workloads on AWS. The company has over 11,000 AWS-certified professionals, and Amazon.com is investing in Kyndryl Holdings’ training, joint solutions, and industry-specific capabilities to support that push.

This focus on AI is already showing up in client work. In its expanded deal with Broadridge Financial Solutions (BR), Kyndryl Holdings is using its Bridge platform and AI tools to help improve trading systems, modernize wealth platforms, and simplify operations. At the same time, it is upgrading Broadridge Financial Solutions' infrastructure, including data centers and networks, while adding more automation to fix issues faster and reduce complexity.

A similar trend is playing out in its work with Alphabet (GOOG) (GOOGL). Through an expanded agreement with Google Cloud, Kyndryl Holdings is helping companies run applications across private data centers, on-premises systems, and edge environments using Google Distributed Cloud and Kubernetes. The setup companies run their systems according to specific rules or performance needs, while keeping full control over placement of data and its management.

Analysts Weigh KD’s Upside

Kyndryl Holdings is expected to report its next results on August 3, for the June quarter. Wall Street is not expecting much in the near term, with estimates pointing to a loss of $0.06 per share, down sharply from a $0.29 profit a year ago. Looking further out, analysts see earnings reaching $1.54 in fiscal 2027, a 25.20% increase from $1.23 in fiscal 2026.

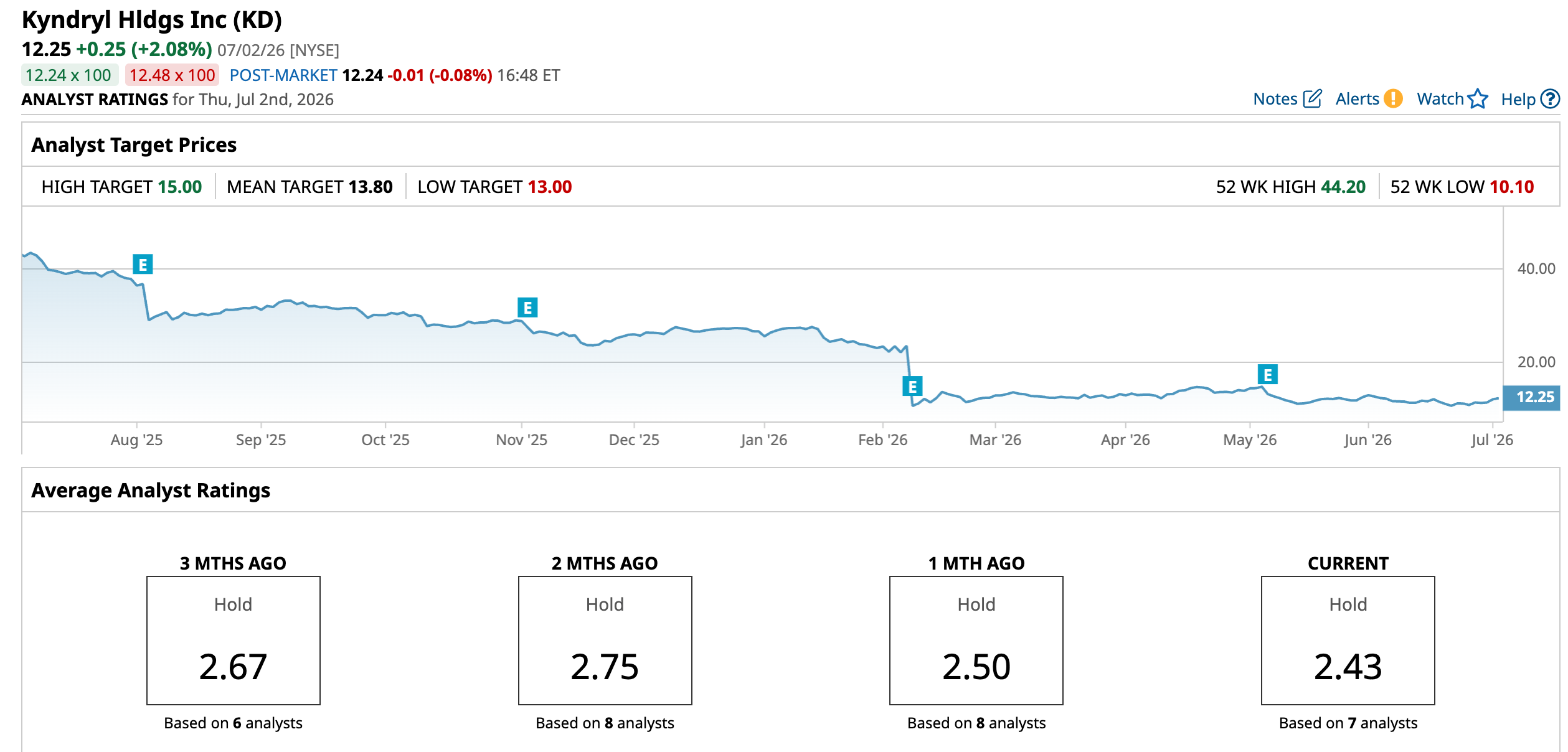

Analyst sentiment has been cautious. In May 2026, Susquehanna lowered Kyndryl Holdings to “Neutral” from “Positive” and cut its price target to $13 from $16, pointing to ongoing business challenges. Around the same time, Scotiabank also reduced its target to $15 from $16.50 while keeping a “Sector Perform” (or “Hold”) rating.

Overall, the seven analysts covering Kyndryl Holdings have a consensus “Hold” rating. Their average price target of $13.80 suggests 12.65% upside from current levels.

Conclusion

Kyndryl’s Microsoft partnership is a meaningful step in the right direction, especially as sovereign cloud and AI governance become real spending priorities for enterprises. It strengthens KD’s positioning and could help drive higher-value deals over time, but it does not fully offset the company’s weak earnings momentum and ongoing execution challenges. For now, this looks more like a gradual tailwind than a game-changing catalyst. Most likely, shares drift modestly higher in the near term on improved sentiment, but a sustained re-rating will depend on clearer earnings growth and consistent margin expansion.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

/Robot%20arm%20industrial%20automation%20manufacturing%20by%20Eakrin%20via%20Adobe%20Stock.jpeg)