NVIDIA Corporation NVDA has once again delivered a stellar earnings report, reinforcing its dominance in the artificial intelligence (AI) and semiconductor markets. On Feb. 26, the company reported fourth-quarter fiscal 2025 revenues of $39.33 billion, marking a 78% year-over-year surge and surpassing the consensus estimate of $37.72 billion.

With a record-breaking data center segment and strong demand for AI-driven computing solutions, NVIDIA's growth story remains compelling. Strong fundamental growth drivers, along with an attractive valuation, make NVDA stock a prudent investment choice right now.

Data Center Segment: NVIDIA’s Growth Powerhouse

NVIDIA’s Data Center business remains the backbone of its financial strength. In the fourth quarter, the segment generated $35.58 billion in revenues, representing 90.5% of total sales. This marked a staggering 93% year-over-year increase and 16% sequential growth, driven by the rapid adoption of artificial intelligence (AI) workloads.

The demand for NVIDIA’s Hopper 200 and Blackwell GPU computing platforms has been a key catalyst as cloud providers and enterprises scale their AI infrastructure. Large cloud service providers contributed nearly 50% of Data Center revenues, indicating continued hyperscale investment in AI-driven computing.

With AI adoption accelerating across industries, NVIDIA's stronghold in data centers makes it a critical beneficiary of this trend. The company’s leadership in AI chip development positions it well for sustained revenue growth in this segment.

NVIDIA’s Strong Financial Execution and Profitability

Beyond revenue growth, NVIDIA demonstrated exceptional financial discipline. The company reported non-GAAP gross margins of 73.5%, maintaining profitability despite rising operational expenses. Non-GAAP operating income jumped 73% year over year to $25.52 billion, reflecting the company’s ability to convert strong revenue growth into bottom-line gains.

NVIDIA’s cash flow generation also remains robust. The company ended the fourth quarter with $43.2 billion in cash, cash equivalents and marketable securities, up from $38.4 billion in the previous quarter. This strong liquidity position enables NVIDIA to reinvest in research & development, expand manufacturing capabilities and return capital to shareholders.

AI Momentum: A Multi-Year Growth Catalyst for NVIDIA

NVIDIA’s earnings call emphasized the transformative potential of AI across industries. CEO Jensen Huang highlighted the growing adoption of reasoning AI models, which require significantly higher computational power. The Blackwell architecture, with its up to 25x higher token throughput for AI inference compared to Hopper 100, is expected to play a crucial role in shaping the next phase of AI-driven computing.

The upcoming launch of NVIDIA’s Blackwell Ultra and Vera Rubin platforms could further strengthen the company’s technological lead. With AI infrastructure investments accelerating globally, NVIDIA is well-positioned to capitalize on these expanding opportunities.

NVIDIA Q1 Guidance: Another Strong Quarter Ahead

NVIDIA’s outlook for the first quarter of fiscal 2026 remains upbeat. The company projects first-quarter revenues of $43 billion, reflecting continued momentum in AI-driven demand. Gross margins are expected to remain strong at 71% despite increasing costs associated with ramping up Blackwell production.

Additionally, NVIDIA is witnessing strong traction in emerging AI applications, including enterprise AI, autonomous vehicles and robotics. This diversification of AI-driven revenue streams reinforces the company’s long-term growth potential.

The Zacks Consensus Estimate for first-quarter revenues is pegged at $43.28 billion, indicating 66.2% year-over-year growth. The consensus mark for non-GAAP earnings stands at 92 cents per share, calling for a 50.8% increase from the year-ago quarter.

NVIDIA has a strong history of beating earnings estimates. It surpassed the Zacks Consensus Estimate for earnings in each of the trailing four quarters, the average surprise being 7.9%.

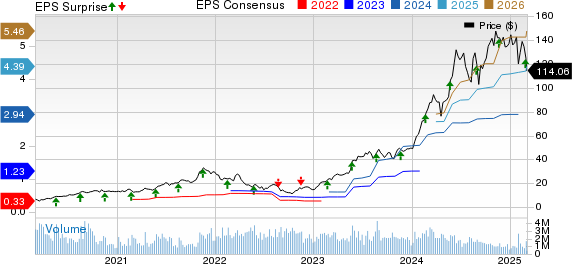

NVIDIA Corporation Stock Price, Consensus and EPS Surprise

NVIDIA Corporation price-consensus-eps-surprise-chart | NVIDIA Corporation Quote

NVIDIA’s Discounted Stock Valuation: A Buying Opportunity

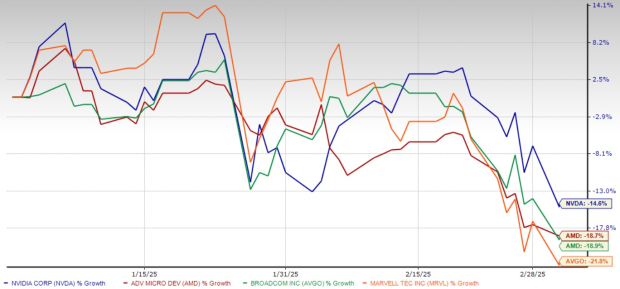

Despite strong fundamentals and robust quarterly performances, NVIDIA shares have plunged 14.6% year to date due to broader market volatility. The decline reflects the impact of an exaggerated fear that DeepSeek’s innovation could reduce demand for NVIDIA’s high-end AI chips. Also, the broader market sell-off due to the imposition of new import tariffs on Canada, Mexico and China weighed on NVIDIA’s share price performance.

Other major players in the semiconductor space, including Advanced Micro Devices AMD, Broadcom AVGO and Marvell Technology MRVL, are also trading in the red zone due to the recent broader market sell-off.

YTD Stock Price Return Performance

Image Source: Zacks Investment Research

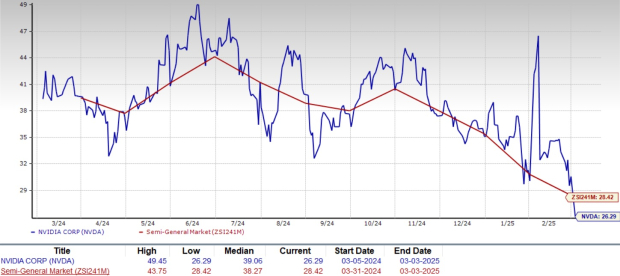

However, the recent sell-off has provided a buying opportunity for investors as NVDA now trades at an attractive valuation multiple. The stock trades at a trailing 12-month price-to-earnings (P/E) ratio of 26.29, below the Zacks Semiconductor – General industry average of 28.42. This suggests the stock is trading at a relative discount, offering potential upside for investors.

NVDA Forward 12-Month P/E Ratio

Image Source: Zacks Investment Research

Conclusion: Buy NVIDIA Stock Now

NVIDIA's outstanding fourth-quarter earnings results reaffirm its position as a leader in AI-driven computing. The company’s record Data Center revenues, strong profit margins and optimistic guidance for the first quarter of fiscal 2026 highlight its continued growth trajectory. NVIDIA’s long-term potential in AI computing and data center dominance and attractive valuation make it a stock worth buying. Currently, NVDA carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Only $1 to See All Zacks' Buys and Sells

We're not kidding.

Several years ago, we shocked our members by offering them 30-day access to all our picks for the total sum of only $1. No obligation to spend another cent.

Thousands have taken advantage of this opportunity. Thousands did not - they thought there must be a catch. Yes, we do have a reason. We want you to get acquainted with our portfolio services like Surprise Trader, Stocks Under $10, Technology Innovators,and more, that closed 256 positions with double- and triple-digit gains in 2024 alone.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Advanced Micro Devices, Inc. (AMD): Free Stock Analysis Report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

Marvell Technology, Inc. (MRVL): Free Stock Analysis Report

Broadcom Inc. (AVGO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

/amazon%20holiday%20delivery%20boxes%20by%20Cineberg%20via%20iStock.jpg)

/NVIDIA%20Corp%20logo%20on%20phone%20and%20AI%20chip-by%20Below%20the%20Sky%20via%20Shutterstock.jpg)

/Palo%20Alto%20Networks%20Inc%20HQ%20sign-by%20Tada%20Images%20via%20Shutterstock.jpg)

/Lululemon%20Athletica%20inc_%20leggings%20by-%20Sorbis%20via%20Shutterstock.jpg)