We're seeing a utilities boom like we haven't in quite some time. Indeed, since the rise of the internet, I don't think we've seen this many infrastructure and utilities companies in the limelight as we're seeing now.

One company that's starting to grab investor attention in a big way is National Grid (NGG), a U.K.-based electricity and gas utility company. Serving much of the United Kingdom, National Grid is a company that's not often on investors' radar screens, but that could mean that it's an interesting opportunity to consider.

Why is that, you might ask? Well, National Grid just announced a big move on Wednesday to invest $1.75 billion in a U.S. artificial intelligence (AI) power infrastructure company, supporting the data center buildout.

Let's dive more into this deal and why NGG stock has been seeing so much volatility following the news.

The Data Center Boom Will Require a Lot of Power

This $1.75 billion deal is significant in that it signals to investors that global utility players want a piece of what the U.S. market has to offer. Indeed, the data center buildout that's happening in the U.S. (and around the world) will inevitably result in a surge of power demand.

The particular company National Grid is investing in is Joulent, a company that's currently looking to undertake a massive 2.67 gigawatt (GW) project in Texas. In combination with Chevron (CVX), which is part of the joint venture to put this project together, National Grid looks to increase its exposure to the U.S. market and grab a slice of the tech-driven power demand many investors are after.

Notably, this project should benefit from its geographic proximity to cheaper natural gas in the Permian Basin. Additionally, the fact that Microsoft (MSFT) is the key player looking to ultimately utilize the power generated by this facility in a long-term contract means that the sorts of long-term cash flows this project looks to generate should be increasingly stable.

How Could This Deal Impact National Grid's Fundamentals?

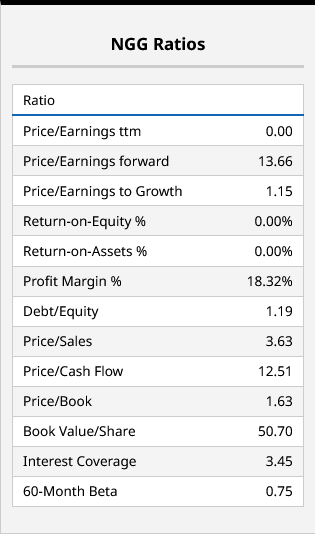

Looking at National Grid's underlying balance sheet and income statement strength below, one could argue this is a company that doesn't need to take this deal on.

Trading at almost 14 times forward earnings and with a price-earnings-to-growth (PEG) ratio of just 1.15, that's dirt cheap in the world of utility stocks today. Undoubtedly, utilities have been among the leading companies in recent years in terms of outperformance, due in part to expectations that the kind of demand we're about to see could unleash remarkable cash flow for decades to come.

Now, one might argue that this deal is one that could be too capital-intensive and could result in lower free cash flow for the coming quarters and years. I think that's the case, and that's specifically why we're seeing NGG stock battered around the stock chart on this news.

That said, I do think the market will ultimately come to some sort of rationalization of what this deal will mean in terms of cash flows three, four, or five years out. When that happens, and if demand expectations remain stable (or continue to increase), this is a stock that could be well-positioned for a big bump.

And, given that this deal is small in comparison to National Grid's $70 billion expansion plans long-term (which in and of itself could be cause for concern for some investors), we are probably talking about small potatoes here.

The European energy complex is very different from that of North America. Indeed, I've seen some analysts argue that this is a better market to invest in, given the price differential between European energy prices and American or Canadian prices.

That said, the market appears to view this deal cautiously. Let's see what the experts have to say.

What Does Wall Street Think of This Deal?

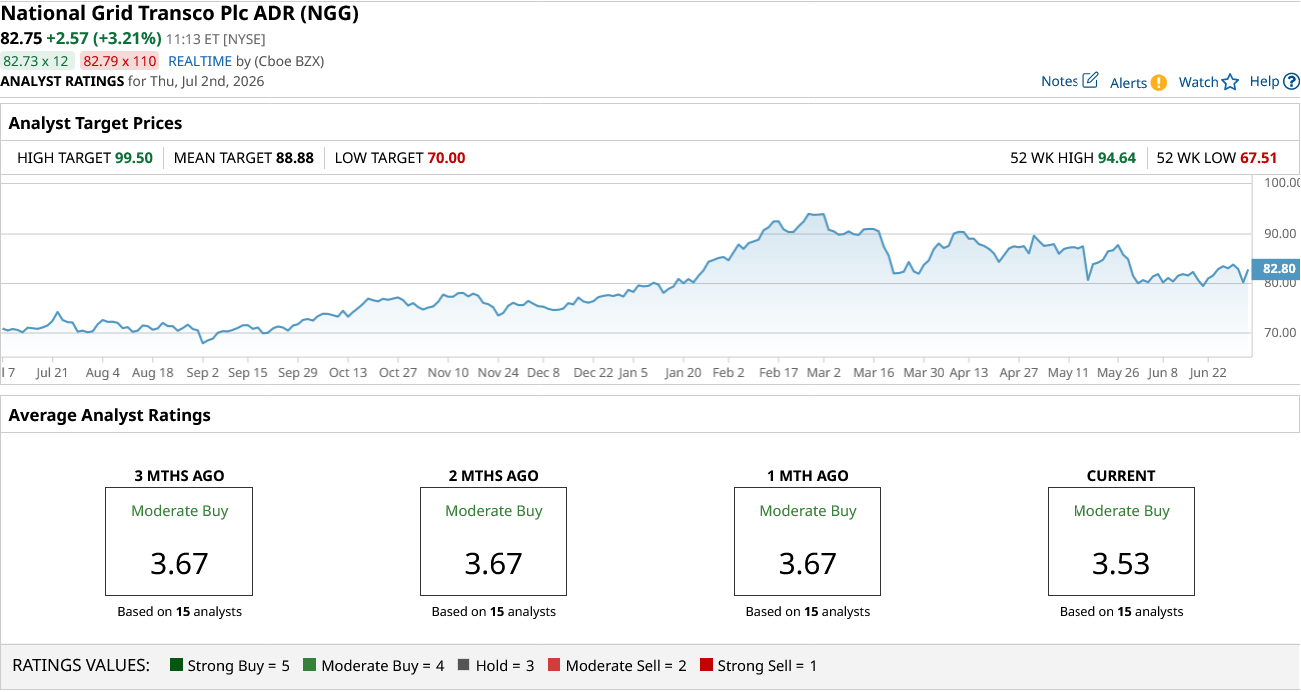

Overall, the consensus on Wall Street appears to be that National Grid is actually relatively fairly valued. At least, it was much closer to fair value before this deal was announced and doesn't have much upside from here.

The $88.88 price target analysts agree on is right around 7% higher than current levels, but also lower than where this stock traded for much of the first and second quarters of this year. In other words, the market appears to be souring on the idea that more capital spending is better in this environment, even if that means this extra capacity could serve a utility giant like National Grid well over the long term.

Personally, NGG stock is one that's starting to look attractive to me. I like the geographical diversification this deal provides and do think that this is one utility stock that could be due for a nice bounce, and today's 3% so far is a good start, if we do see market sentiment improve further.

Of course, if sentiment continues to wane around the AI and data center buildout, this is a stock that could be headed lower. Perhaps some investors are waiting to pull the trigger, but this is one watch list stock I think could be worth legging into at current levels.

On the date of publication, Chris MacDonald did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)