Shares of broadband and telecommunications company Charter Communications (CHTR) rallied by more than 9% on June 29 after a report revealed that SpaceX (SPCX) may be considering a partnership with the company to offer a new mobile phone service. Additionally, while not directly related to Charter, the proposed split of Comcast (CMCSA) lent to wider optimism around broadband and telecommunications names.

Here's what's going on with Charter Communications stock amid the SpaceX partnership rumors.

About Charter Communications

Founded in 1993, Charter Communications is one of the largest broadband and cable telecommunications companies in the United States. Operating primarily under the Spectrum brand, the company provides broadband internet, mobile, cable television, voice services, enterprise networking, and advertising solutions.

Valued at a market capitalization of $17.4 billion, CHTR stock is down 33% on a year-to-date (YTD) basis. Could a potential partnership with SpaceX lead to a reversal in fortunes for the stock? Let's take a closer look.

Charter Is Not for the Growth Junkies

In a world where doubling revenue and earnings can be a standard occurrence, Charter stands out — and not in a good way. The past five years have seen the company's top and bottom lines report compound annual growth rates (CAGRs) of roughly 2% and 7%, respectively. Moreover, results in more recent quarters have been nothing to be excited about.

Charter's most recent quarter was mixed, with a beat on the top line but a miss on the bottom line. Revenue came in at $13.6 billion, a decline of 1% year-over-year (YOY). The connectivity segment, which comprises its internet and mobile service divisions, showed marginal growth of just 0.9% in the same period to $6.9 billion. Earnings grew by 8.9% YOY to $9.17 per share. However, this failed to surpass the consensus estimate of $9.97 per share, marking another consecutive earnings miss by the company.

Total customers declined 1.5% to 31,683 from 32,160 in the corresponding period a year ago. Meanwhile, net cash from operating activities rose slightly to $4.3 billion. Free cash flow declined to $1.4 billion from $1.6 billion in the year-ago period. Overall, the company closed the quarter with a cash balance of $517 million and no short-term debt on its books. Still, Charter has long-term debt of $94.4 billion, creating pressure on its margins.

Notably, CHTR stock is trading at undervalued levels now. Its forward price-to-earnings (P/E) ratio of 3.4 times, price-to-sales (P/S) multiple of 0.33 times, and price-to-cash flow (P/CF) ratio of 1.3 times are all below the respective sector medians.

The SpaceX Push

So, why is SpaceX even considering aligning itself with a low-growth company like Charter? The answer lies in the latter's vast land-based network capabilities.

Charter is the largest provider of internet services to households in the U.S., and by routing traffic through Charter’s extensive terrestrial fiber and cable network, SpaceX can "offload" data from its satellite constellation. This allows it to handle higher traffic volumes in cities and suburbs without overloading satellite bandwidth. Thus, rather than building its own physical network from the ground up — which is prohibitively expensive and time-consuming — SpaceX can leverage Charter’s massive, pre-existing network and expand its market from a niche rural provider to a mass-market mobile carrier.

However, analyst Sam McHugh of BNP Paribas is not very enthused about the possible deal. “Charter's network of urban hotspots and small cells could help Starlink Mobile narrow the structural coverage gap associated with a direct-to-cell satellite network. However, Charter can't offer a solution that entirely closes the gap because it can't provide Starlink Mobile subscribers with access to [Verizon's (VZ)] wireless network,” McHugh wrote in a note to clients.

While the jury is out on the partnership with SpaceX, Charter is chartering its path toward growth rates that are not languishing in the low single-digits.

To that end, Invincible Wifi can be a key offering. The company positions the product as an advanced WiFi 7 router equipped with integrated 5G backup connectivity and an eight-hour battery that ensures continued home internet access during power disruptions. This combination of reliable connectivity through a battery-supported 5G solution is likely to appeal to existing customers considering upgrades and could attract new users.

But the real game changer may be the $34.5 billion acquisition of Cox, which received clearance from the Federal Communications Commission (FCC) on Feb. 27, 2026. The combined company will be the largest broadband provider in the U.S. with almost 36 million internet subscribers and around 70 million homes once it fully closes.

Finally, Charter is roughly midway through a multi-phase plan to upgrade its hybrid fiber coax plant, with the first 15% of the footprint moving to higher capacity and a high split that boosts upload speeds, and about 35% eventually getting a full DOCSIS 4.0 upgrade. Early markets already offer up to 2 gigabits per second downstream and 1 gigabit per second upstream, and the network portion runs about $100 per home passed, a relatively cheap way to defend share against fiber and fixed wireless rivals.

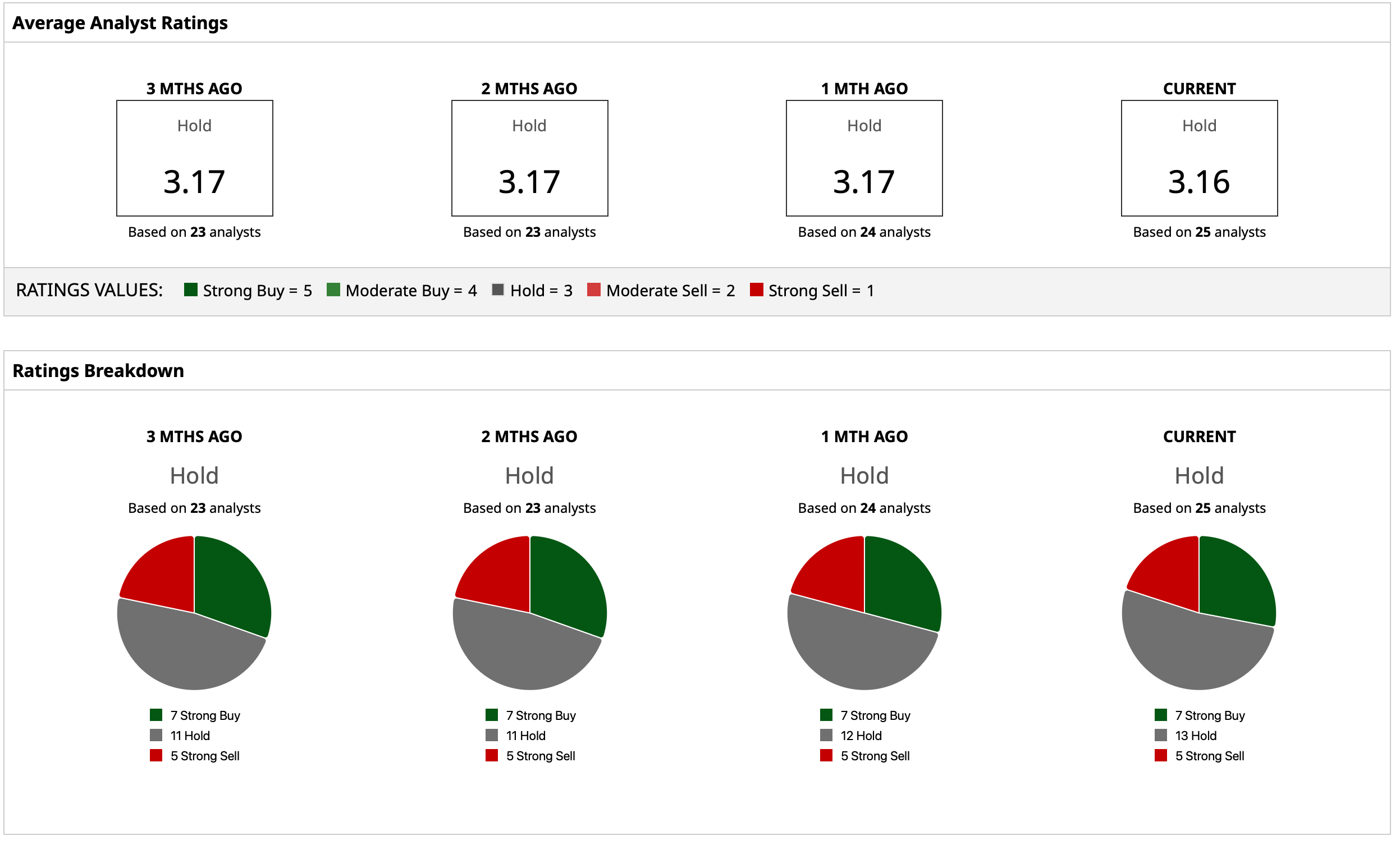

What Do Analysts Think of CHTR Stock?

Analysts have a consensus “Hold” rating for CHTR stock. The mean target price of $242.89 indicates potential upside of about 74% from current levels. Out of 25 analysts covering the stock, seven have a “Strong Buy” rating, 13 have a “Hold” rating, and five have a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)