/Engineer%20holding%20computer%20microchip%20by%20LIGHTFIELD%20STUDIOS%20via%20Adobe%20Stock.jpeg)

A class-action lawsuit filed on June 25 in a U.S. court has named Micron Technology (MU), Samsung Electronics, and SK Hynix in an anti-trust case over alleged DRAM price fixing. The claim is that these three companies, which control most of the global DRAM market, cut back production of older DDR3 and DDR4 chips while shifting focus to AI-focused High Bandwidth Memory (HBM).

According to the lawsuit, that move was meant to push prices higher, not just follow demand. DRAM prices have jumped about 700% since 2022.

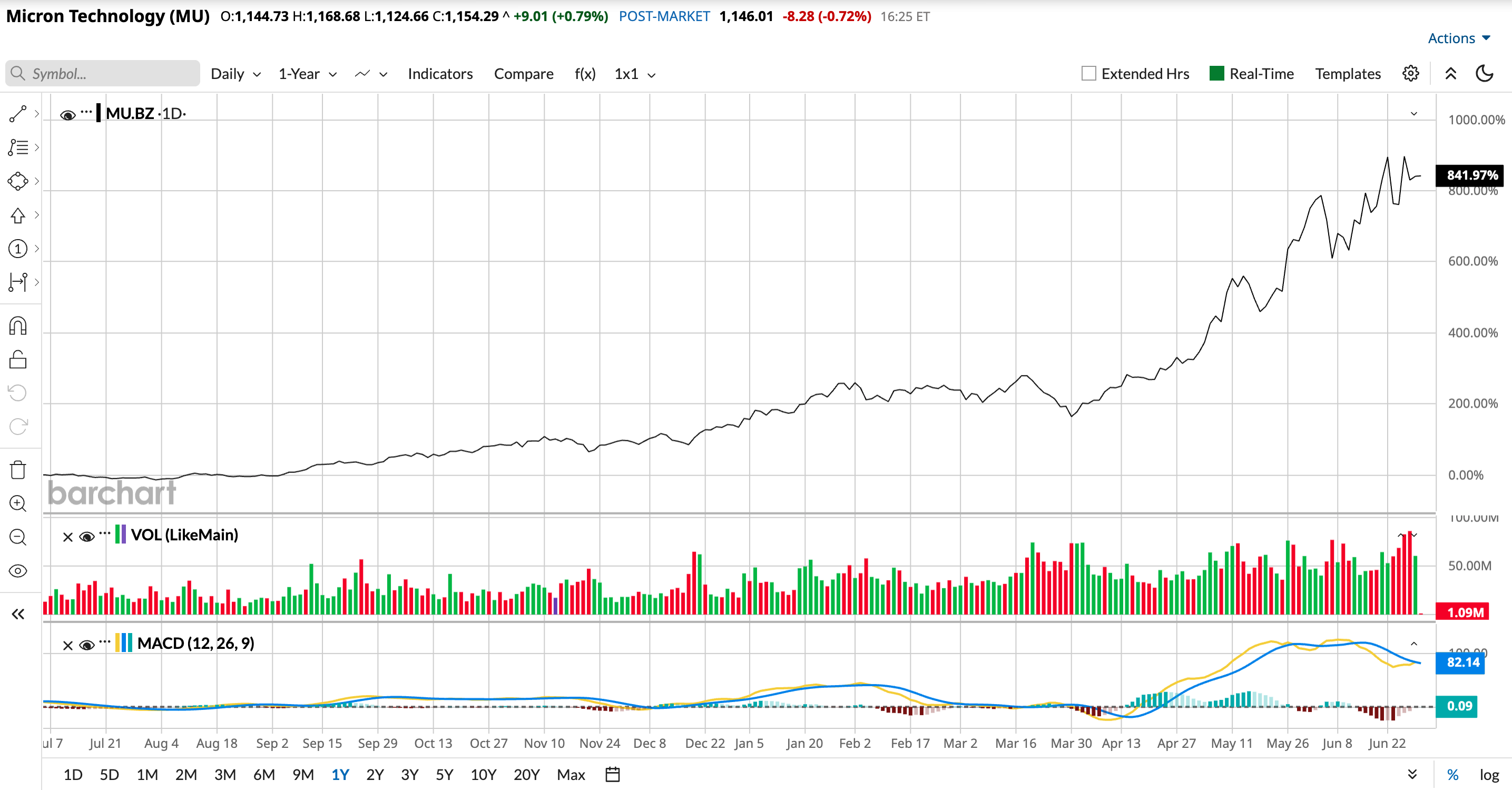

What makes this stand out is the timing. Just days before the lawsuit, Micron Technology posted its strongest quarter ever, with $41.46 billion in revenue and nearly 4x growth from a year ago. The stock had already run from a 52-week low of $103.38 to an all-time high of $1,255.00, an astounding gain of 1,114% in one year.

That rally has been driven by strong demand for HBM and a tight DRAM market expected to last through 2028, helping Micron earn its place as the top-rated growth stock in the S&P 500 Information Technology Index ($SRIT), alongside Nvidia (NVDA).

Micron Technology shares slipped on Monday intraday to a low of $1,023.65 after the news, extending a pullback from recent highs. But for a company riding one of the most powerful AI-driven earnings cycles in semiconductor history, does this lawsuit represent a genuine threat to the MU bull case?

Micron’s Numbers Remain Strong

U.S.-based chipmaker Micron produces memory and storage products like DRAM, NAND, and high-bandwidth memory used in data centers, AI systems, and everyday devices.

The stock has been on a massive run, up 842% over the past 52 weeks and another 306.79% year-to-date (YTD).

Even with that surge, valuation is still reasonable, with a forward price-to-earnings ratio of 18.40 times compared to the sector average of 24.48 times.

Also, Micron pays a quarterly dividend of $0.150, which comes out to a 0.50 (0.04%) annual yield, well below the tech sector average of 1.37%. The forward payout ratio is just 2.13%, leaving plenty of room to reinvest, and the company has only one year of dividend growth so far.

On the financial side, the turnaround has been sharp. In fiscal Q3 2026, revenue jumped to $41.46 billion, up from $23.86 billion in the prior quarter and $9.30 billion a year ago. GAAP net income came in at $28.24 billion, or $24.67 per share, while non-GAAP net income reached $28.86 billion, or $25.11 per share. Operating cash flow rose to $25.39 billion, more than double the previous quarter and far above last year’s level. For Q4, Micron expects around $50.0 billion in revenue, gross margins near 86%, and non-GAAP EPS of about $31.00, pointing to continued strength.

Growth Drivers Are Still Intact

Micron Technology is pushing deeper into AI through its recent deal with Anthropic. The partnership covers how memory and storage are designed, supplied, and used in real AI systems, including the rollout of Anthropic’s Claude within Micron. It also includes Micron taking part in Anthropic’s Series H funding.

The main focus is simple: improve the way in which memory performs in AI workloads like training and inference. Micron’s HBM, DRAM, and SSD products sit at the center of that, helping boost speed, efficiency, and overall system cost.

On the manufacturing side, Micron Technology is expanding production in the U.S. with its 1-αlpha DRAM rollout at its Virginia facility. This is the most advanced memory made in the U.S. right now and strengthens Micron’s position as the country’s only domestic memory producer. The chips are built for long-use cases like DDR4 and LP4, serving industries such as automotive, defense, aerospace, industrial, networking, and medical, where reliability matters.

The company is also moving into edge and physical AI through its investment in SiMa.ai. The focus here is on combining compute and memory to deliver strong performance with lower power use. This targets real-world systems like robotics, autonomous machines, and industrial automation, with Micron memory already built into SiMa.ai’s modules for immediate use.

Analysts See More Room Ahead

Micron Technology’s next earnings report is set for Sept. 22, 2026. For the current quarter ending August 2026, analysts expect $31.06 per share, up from $2.86 a year ago, a 986.01% jump. For full-year fiscal 2026, earnings are projected at $71.74, up from $7.68, marking an 834.11% increase.

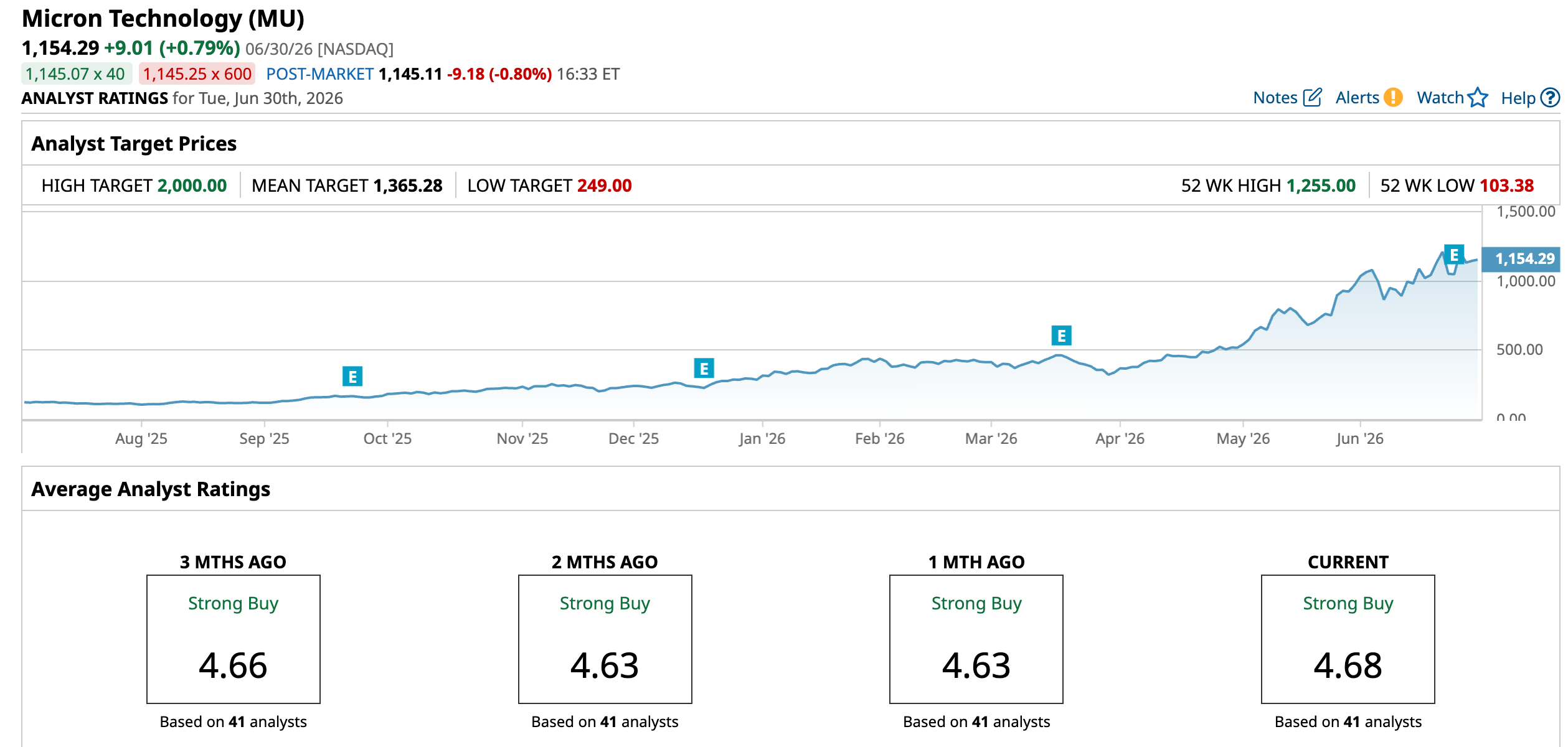

Just before the news, Deutsche Bank’s Melissa Weathers kept a “Buy” rating on Micron Technology and raised her price target to $1,500. Her view is that DRAM supply is still extremely tight and could stay that way through 2028 or longer, as supply struggles to keep up with AI demand.

She also expects the next wave of demand to come from both standard and low-power DRAM, especially as newer AI systems require more memory. Importantly, she believes this tight supply-demand setup will hold even with recent capacity expansion plans. Other firms see the same trend. Susquehanna recently lifted its target to $1,750, pointing to ongoing strength in memory and storage as HBM supply remains constrained.

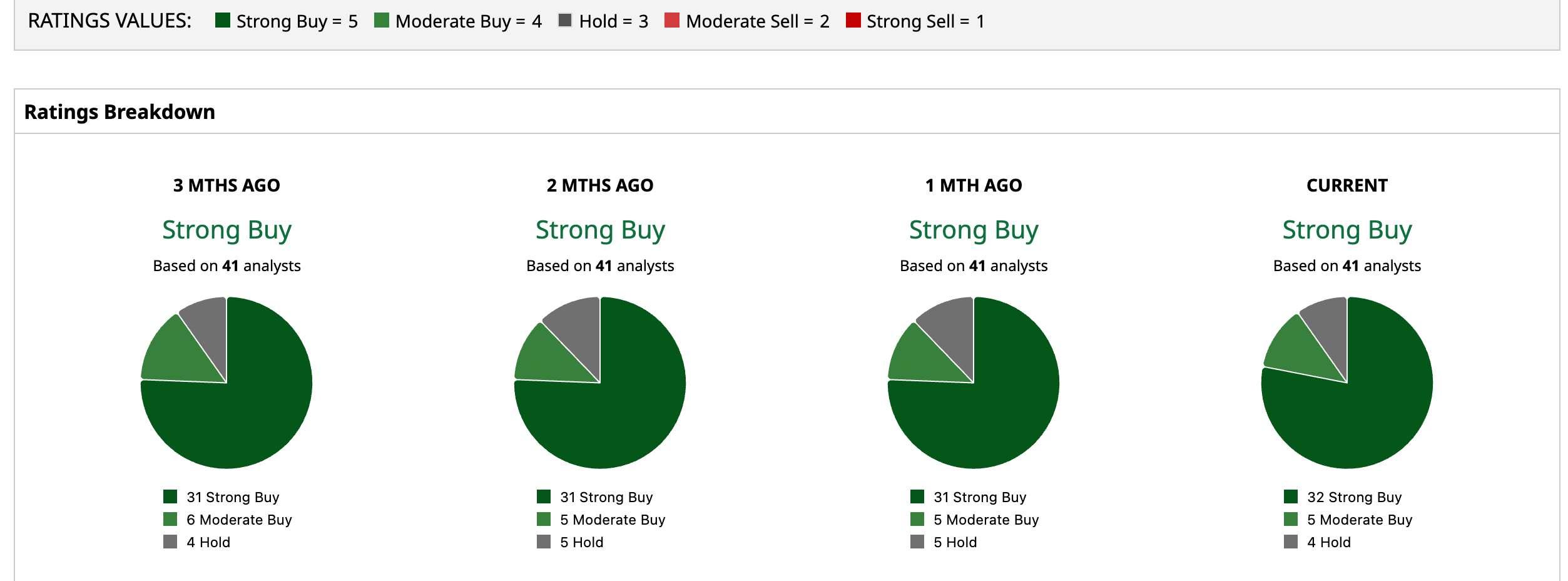

Overall, all 41 analysts covering Micron Technology rate it a consensus “Strong Buy,” with an average target of $1,365.28, suggesting 18.28% upside from current levels.

Conclusion

Right now, the lawsuit looks more like a headline risk than a fundamental break in the Micron story. The company is delivering record earnings, demand for AI memory remains tight, and analysts are still overwhelmingly bullish despite the legal noise. Antitrust cases can drag on for years and rarely disrupt near-term operations unless penalties or restrictions materialize. Given the strength in pricing, supply constraints, and forward estimates, the more likely path is continued volatility in the short term but an upward bias over time. Unless the case gains unexpected traction, fundamentals still appear to be firmly in control of the stock’s direction.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)

/Corning%20Incorporated%20on%20screen%20in%20front%20of%20website%20By%20Timon.jpeg)