/A%20concept%20image%20of%20space_%20Image%20by%20Canities%20via%20Shutterstock_.jpg)

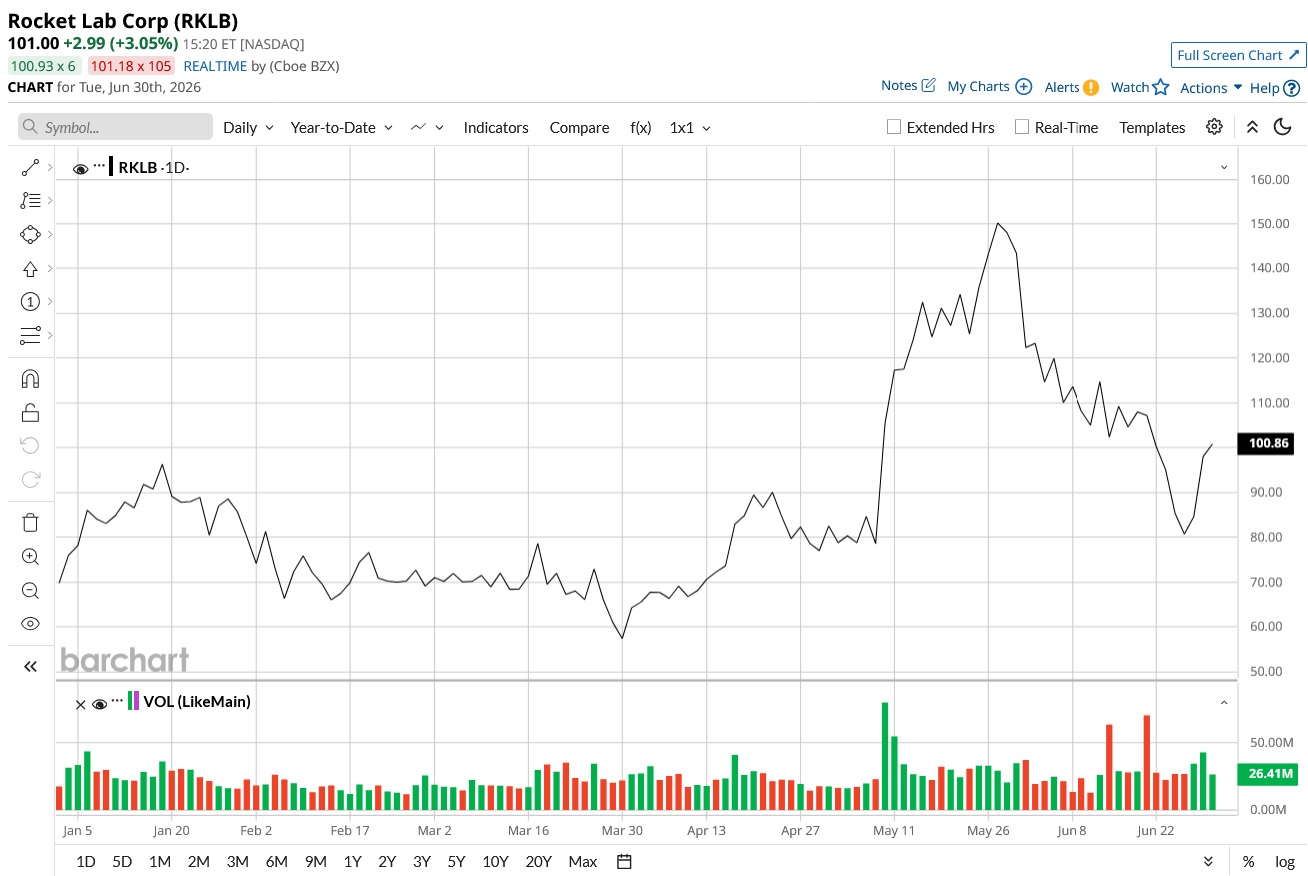

Shares of commercial space company Rocket Lab (RKLB) ended 16% higher in yesterday's trading session after it announced the acquisition of satellite services company Iridium (IRDM) in a deal worth $8 billion. Rocket Lab will pay $54 a share for Iridium, with half in cash and half in RKLB stock.

With the impending acquisition, Rocket Lab will become an end-to-end space company, having launch and deployment capabilities, along with providing satellite communications services.

Sounds familiar? Yes, that is what SpaceX (SPCX) does.

And this acquisition of Iridium signals that Rocket Lab will not be a pushover in the space race. Thus, with its newfound, well, space in the Nasdaq-100, what will Iridium bring to the table for Rocket Lab so that it remains a serious competitor to SpaceX? Let's find out.

About Rocket Lab

Founded in 2006, Rocket Lab has evolved into a vertically integrated space infrastructure company that designs rockets, satellites, spacecraft components, solar panels, flight software, and national-security space systems. In fact, it is widely viewed as the strongest pure-play competitor to SpaceX.

Valued at a market cap of $48.9 billion, RKLB stock is up 45% year-to-date (YTD).

Will Iridium Be the Fuel for Rocket Lab’s Rocket?

Well, to answer the question quite simply, it very well could be.

For starters, Rocket Lab today is fundamentally a launch and satellite manufacturing company, profitable in neither category yet, still scaling its Neutron rocket toward its maiden flight. Iridium, by contrast, is profitable.

Moreover, the deal gives Rocket Lab control over Iridium's 66-satellite low Earth orbit network, globally licensed L-band spectrum, and a customer base of more than 2.55 million subscribers spanning government, defense, aviation, maritime, and commercial markets. The transaction merges Rocket Lab's launch capabilities and satellite manufacturing with Iridium's global satellite communications network, spectrum, and 500 plus strong partner ecosystem, creating a vertically integrated space company that designs, builds, launches, and operates its own constellations, and gives Rocket Lab an immediate foothold in satellite Internet of Things, direct-to-device communications, positioning and navigation timing, and critical safety of life services.

Also, the deal will bring Rocket Lab a position, navigation, and timing layer that works when GPS is jammed or degraded, a feature the U.S. Space Force already pays for, including a December 2025 contract worth up to $85.8 million.

Building these assets independently, meaning a global L-band network, an established 66 satellite constellation, and a multi-million subscriber base, would likely take years and billions of dollars in investment. Spectrum licenses in particular are scarce, regulatory-bottlenecked assets that cannot simply be purchased off the shelf or rushed through approval. Thus, Rocket Lab effectively just skipped a decade of spectrum negotiation and constellation buildout in a single transaction.

Finally, the acquisition positions Rocket Lab to compete more directly with SpaceX and its Starlink unit, which combines launch services with a satellite communications business. This strategic move aims to challenge SpaceX by bypassing years of infrastructure development, with Rocket Lab securing mature spectrum resources and steady cash flow as a critical competitive advantage.

Got to Reach Profitability Soon

Rocket Lab is an unprofitable company, and that is a concern.

In Q1 2026, revenues increased 63.5% year-over-year (YoY) to $200.3 million as gross margins expanded to 43% from 33.4% in the prior year period. Both product and service revenues posted healthy gains, advancing 57.8% and 74.5%, respectively, to $127.5 million and $72.9 million.

The backlog reached a record high of $2.2 billion, marking a 20.2% sequential improvement.

Losses narrowed to $0.07 per share from $0.12 per share in the year-ago quarter. This represented the third consecutive period of improving profitability, a milestone not seen in the past two years.

Looking ahead, the company projects second-quarter 2026 revenue between $225 million and $240 million. Analysts currently forecast $231.7 million for the period.

Net cash used in operating activities moderated to $50.3 million in the first quarter of 2026 from $54.2 million a year earlier. Rocket Lab closed the March 2026 quarter with $1.2 billion in cash and no short-term debt on its balance sheet.

However, with the company still unprofitable, RKLB shares trade at exceptionally high multiples relative to sales. The forward P/S ratio of 53.43 times sits dramatically above the sector median of 1.90 times.

Analyst Opinion of RKLB Stock

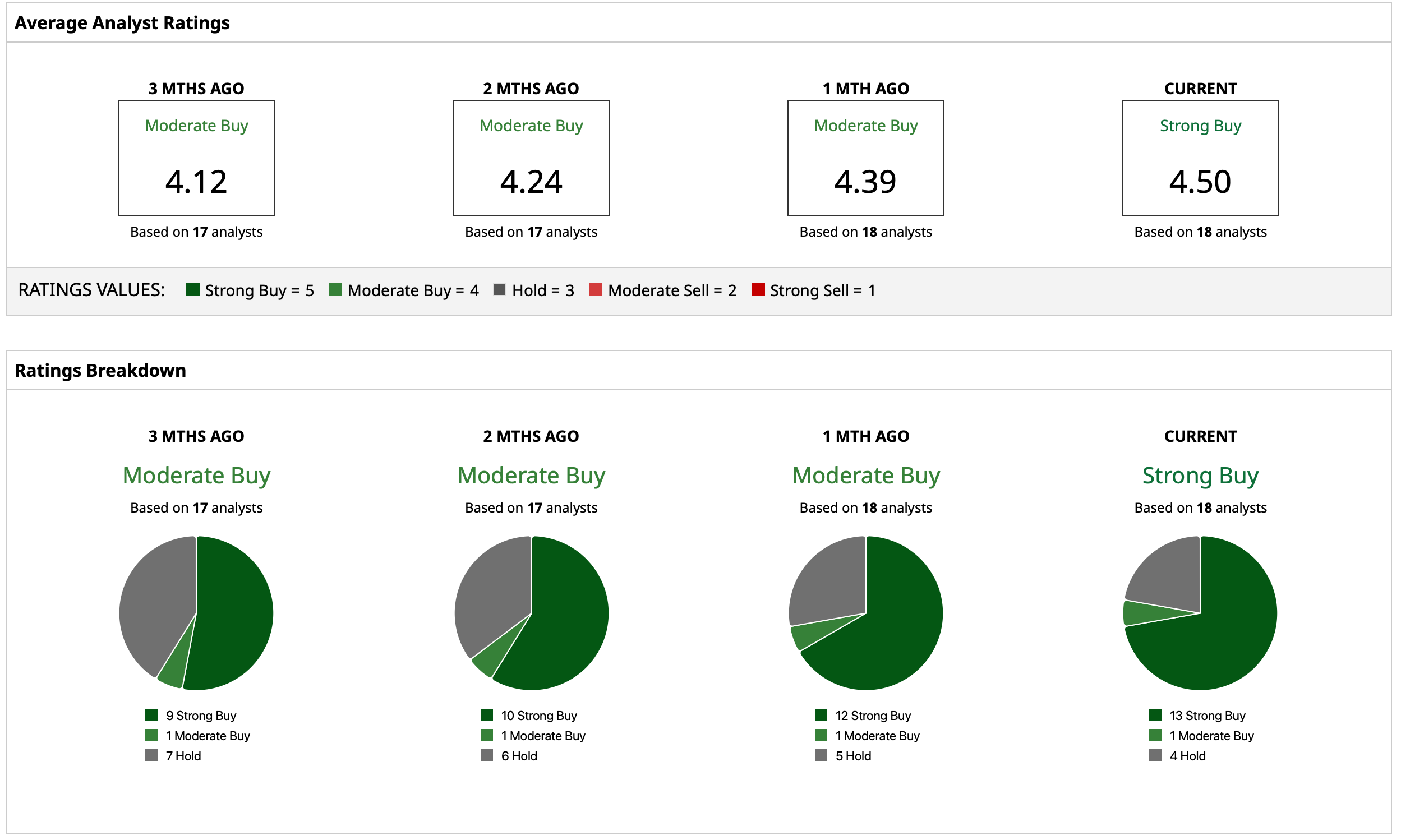

Overall, analysts have attributed to RKLB stock a consensus rating of “Strong Buy.” The mean target price of $109.18 indicates an upside potential of 8% going forward. Out of 18 analysts covering the stock, 13 have a “Strong Buy” rating, one has a “Moderate Buy” rating, and four have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/A%20game%20controller%20in%20front%20of%20a%20Roblox%20computer%20screen%20by%20Miguel%20Lagoa%20via%20Shutterstock.jpg)

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)