SpaceX (SPCX) has not simply captured the imagination of the investing folk, but its IPO has consequently resulted in an unusual casualty: shares of other space-related companies. Shares of the Tema Space Innovators ETF (NASA) are down 3.14% over the past five trading days, while one of its largest holdings, Rocket Labs (RKLB), is down by a slightly sharper 3.91% in the same period.

However, an impending development may halt the decline in RKLB stock.

Notably, Rocket Lab will enter the Nasdaq-100 Index before trading commences on June 22. Not only will this be a reputational boost to the company, but RKLB stock will also receive a substantial influx of passive funds.

About Rocket Lab

Founded in 2006, Rocket Lab has evolved into a vertically integrated space infrastructure company that designs rockets, satellites, spacecraft components, solar panels, flight software, and national-security space systems. In fact, it is widely viewed as the strongest pure-play competitor to SpaceX.

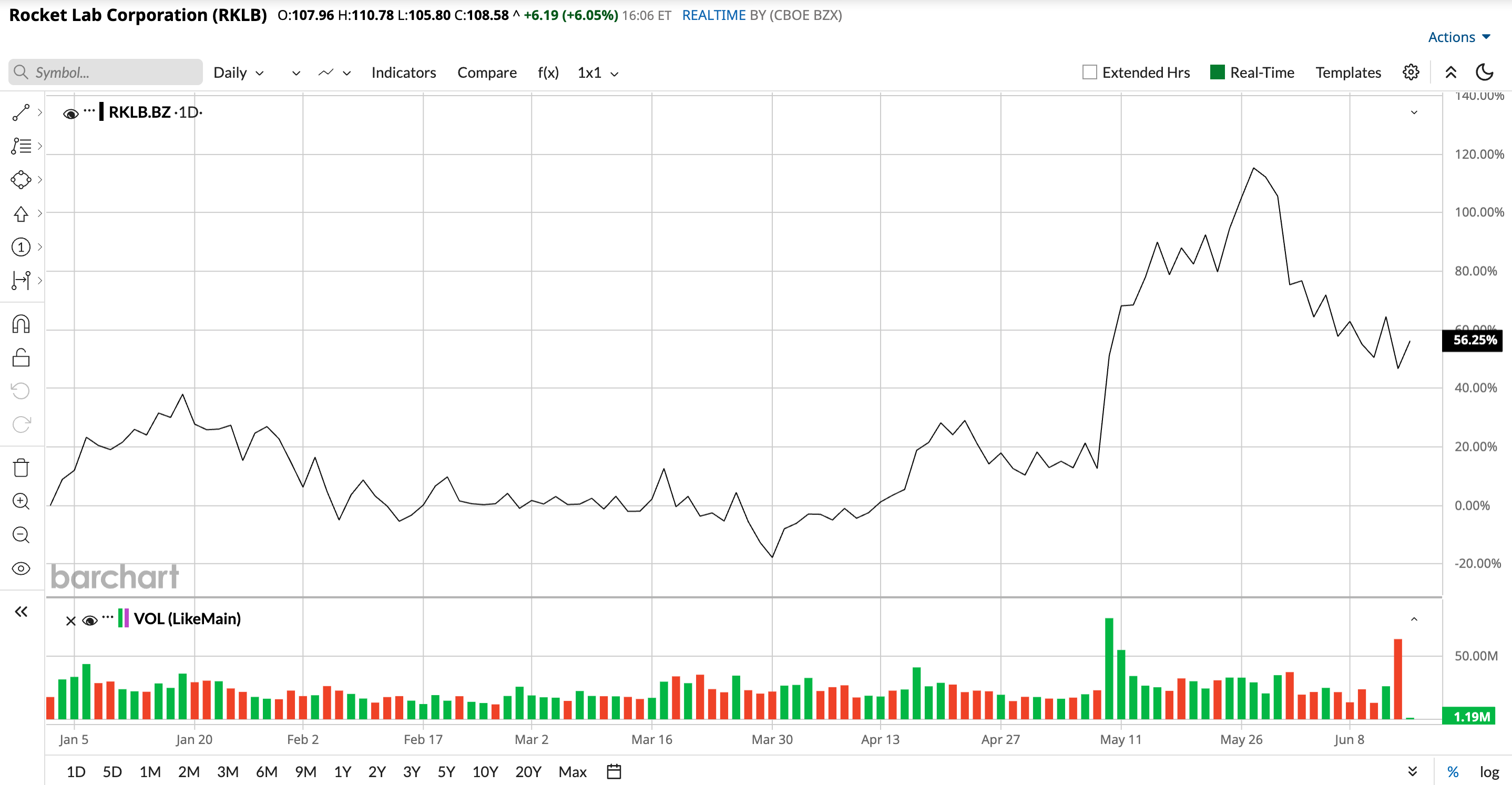

Valued at a market cap of $59.26 billion, RKLB stock is up 56.55% year-to-date (YTD).

So, can Rocket Lab find its space in the SpaceX era? Let's analyze.

Profits Look Farther Than Near

Rocket Lab has been in existence for two decades and has been a listed company for five years. So, expecting it to report at least modest profits is not a tall ask, is it? Yet, the company remains unprofitable. And unlike SpaceX, the company is solely focused on space. It has no other businesses. Thus, funding its rocket initiatives will continue to be either dilutive to existing shareholders or the company has to take the debt route, which it has primarily avoided so far.

Yet, positive signs are there, such as losses remaining stable or narrowing in some cases, coupled with revenue and backlog growth. The company also has a sizable cash balance to act as a bulwark against any unforeseen circumstances.

Notably, results for Q1 included all this. Revenues grew by 63.5% from the previous year to $200.3 million as gross margins improved to 43% from 33.4% in the year-ago period. Both product and service revenues rose at a healthy rate, growing by 57.8% and 74.5% year-over-year (YOY) to $127.5 million and $72.9 million, respectively.

Also, the backlog rose to record levels of $2.2 billion, up 20.2% sequentially.

Meanwhile, losses narrowed to $0.07 per share from $0.12 per share in the year-ago period. Notably, this was the third consecutive quarter of losses narrowing, a first-time occurrence in the past two years.

Overall, the company expects revenue to land between $225 million and $240 million in Q2 2026. Analysts are expecting the same to be at $231.7 million.

Net cash outflow from operating activities slowed down to $50.3 million in Q1 2026 from $54.2 million in Q1 2025. Rocket Lab exited the March '26 quarter with a cash balance of $1.2 billion and no short-term debt on its books.

However, with no earnings, RKLB trades at obscene levels on its sales, akin to the distance its rockets cover from earth to space. Its forward price-to-sales ratio of 64.84 times is miles above the sector median of 1.89.

Neutron Bet

Rocket Lab's emergence as a vertically integrated space player is a strategic move that is already showing its positive reflection on the numbers in the form of a rise in gross margins. Along with keeping costs under control, this strategy ensures that Rocket Lab has an ample supply of all the critical components, a critical feature in a world riddled with numerous geopolitical conflicts.

Acquisitions are also a major part of this strategy, and two recent transactions stand out clearly. The first involves Mynaric AG, which brings advanced laser optical communications terminals designed for air, space, and mobile uses into the technology portfolio. The deal recently closed with a total value of roughly $155.3 million paid through a mix of cash and stock. Laser communications represent a vital element for large satellite groups because they enable effective coordination across many units operating as one integrated network. Without this capability, achieving seamless collaboration among satellite constellations becomes significantly more challenging.

The second key acquisition is Motiv Space Systems, a specialist in space-based robotics, motion control systems, and precision mechanisms for spacecraft. This move broadens Rocket Labs' service range and strengthens its position to pursue sophisticated planetary exploration as well as national security projects. Notably, Motiv has played an important role in major programs such as NASA's Mars Perseverance rover and the CADRE lunar rovers. As efforts to return to the moon and Mars increasingly intersect with national security priorities, this addition positions Rocket Labs to compete effectively for participation in those initiatives.

Meanwhile, much like SpaceX, Rocket Lab already serves as a trusted mission partner for multiple national security and defense programs. The company has supported more than 1,700 missions overall, and its Electron rocket remains the most frequently launched small orbital vehicle worldwide. Additionally, Rocket Lab has been chosen to showcase advanced technologies for the United States Space Force Space Based Interceptor program, known as Golden Dome. As space-based threats emerge as a potential future domain of conflict, the technologies and expertise held by Rocket Labs become highly valuable national security assets, and hence its addition in the Golden Dome program.

However, anticipation and perhaps a large part of the company's growth in the future hinges on Neutron.

Neutron is the latest medium lift launch vehicle currently under development by Rocket Lab. Engineered to challenge the existing commercial space paradigm, Neutron is targeting a highly anticipated initial launch in the final quarter of 2026. The rocket stands out because it can deliver up to 15000 kilograms to low Earth orbit when fully expended, or 13000 kilograms when the booster lands downrange. Recent developments show strong market confidence as Rocket Lab successfully secured a five-launch contract in May 2026, even after a first-stage tank ruptured during a January 2026 hydrostatic pressure test.

What makes Neutron truly unique is its revolutionary aerodynamic architecture and material science. Instead of shedding its payload fairings into the ocean like traditional rockets, Neutron features a captive hungry hippo fairing design. The fairing is permanently attached to the reusable first stage and simply opens up to release the second stage and payload before snapping shut and returning to Earth. This eliminates the need to fish expensive components out of the water and drastically reduces turnaround time. Additionally, the entire rocket is constructed from advanced carbon composites rather than traditional aluminum alloys, making it incredibly lightweight and resilient for multiple atmospheric reentries.

In a direct competition with SpaceX's Falcon 9, Neutron is deliberately tailored for the specific needs of modern satellite constellation deployment at a leaner price point of roughly $50 million per flight, compared to SpaceX $67 million. However, at 22,000 kilograms, Falcon 9's load capacity is higher than that expected of Neutron at 13,000 kilograms.

Analyst Opinion

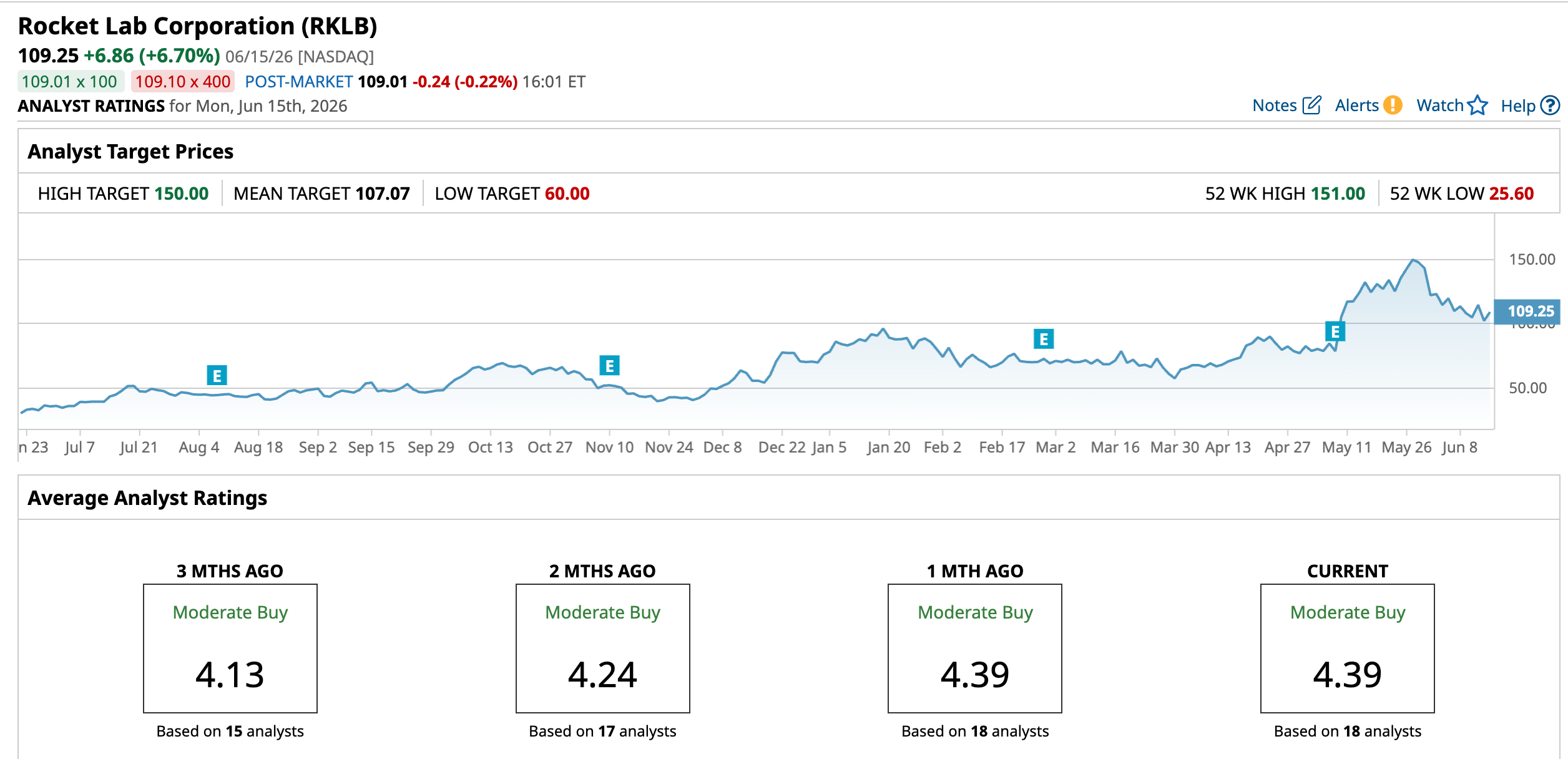

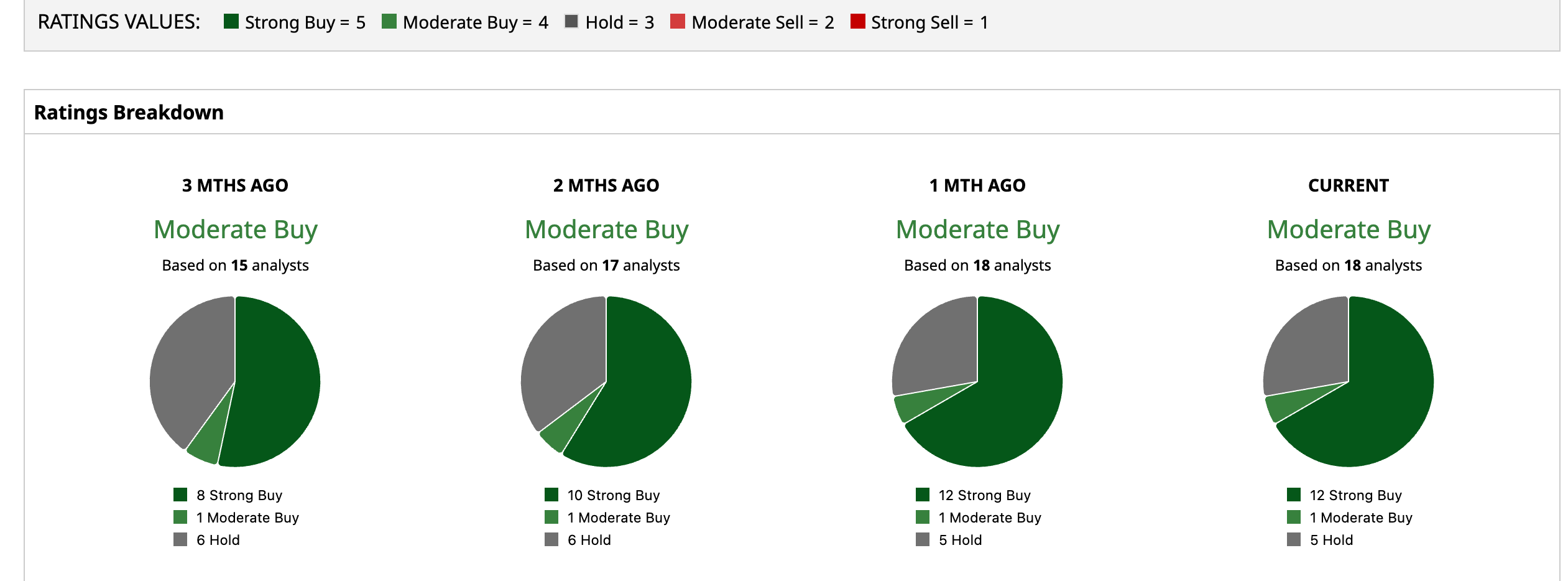

Thus, analysts remain cautiously optimistic about RKLB stock, attributing to it a rating of “Moderate Buy”. The mean target price of $$107.07 has already been surpassed, but the Street-high price of $150 indicates an upside potential of 37.3% going forward. Out of 18 analysts covering the stock, 12 have a “Strong Buy” rating, one has a “Moderate Buy” rating, and five have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)