/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

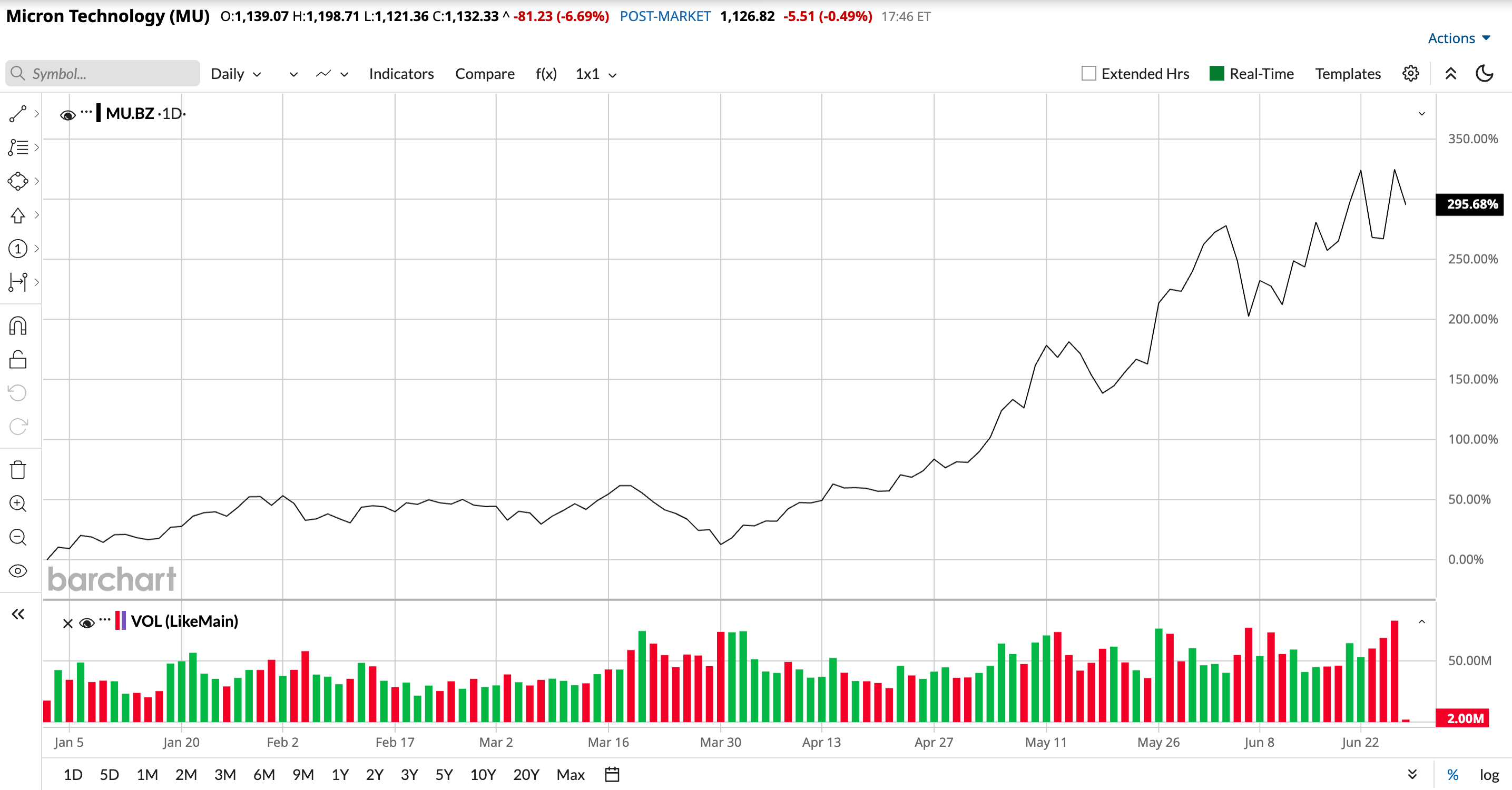

In different points of the market, investors find their new favorites. While in recent years it has been Nvidia (NVDA) or Alphabet (GOOGL) (GOOG), the wider AI trade has anointed a new darling: Micron (MU). Undoubtedly, with a rally of 296.74% year-to-date (YTD), shares of the memory chip major have been a massive hit with investors. In fact, the hype around the company was eclipsed only by those who were not even listed on the exchanges, like SpaceX (SPCX), OpenAI, and Anthropic.

Now, following a sensational set of numbers for its fiscal Q3, leading brokerages on Wall Street are reinforcing their bullish views about the company. One of them is the reputed broker, Stifel.

Reiterating its “Buy” rating and a price target of $1,500 for MU stock, analysts led by Brian Chin at the firm said, "Even more impressive are the terms, with committed volumes but also a favorable pricing structure designed to keep ASP/bit (and GMs) within prescribed, historically high ranges. Micron expects 50%+ of revenue to be covered under SCAs, in our view a best-of-both-worlds blend of fixed and floating ASP [average selling price] exposure."

So, should investors heed Stifel's case for Micron and add to the stock? Or has the rally left no room for new investors to enjoy another round of substantial upside on the stock?

Q3: Strength Beyond The Numbers

Micron's results for its fiscal Q3 2026 had all the usual hallmarks of a solid company, including a double beat on both revenue and earnings.

Revenues for the quarter came in at $41.46 billion, up a remarkable 346% from the previous year, as gross margins more than doubled to a heady 84.9% from 39% in the year-ago period. Unsurprisingly, all the major revenue segments reflected this growth. With revenues of $13.8 billion, $11.5 billion, $11.5 billion, and $4.6 billion, the cloud, data center, mobile, and automotive segments witnessed strong year-over-year (YOY) growth rates of 306%, 667%, 248.5%, and 318.2% with gross margins of 58%, 38%, 24%, and 26%, respectively.

Thus, the company is firing on all cylinders and is not solely dependent on any particular one for growth, even after raising DRAM and NAND prices by low-60s percentage and mid-80s percentage on a QoQ basis, respectively.

Meanwhile, earnings multiplied to $25.11 per share from just $1.91 per share in the prior year. Further, it easily outpaced the consensus estimate of $20.86 per share, marking the ninth consecutive quarter of earnings beat from the company.

For Q4, Micron is expecting revenues to be between $49-$51 billion and earnings to be between $30-$32 per share, which were above analyst estimates.

However, what took the cake in terms of Micron's Q3 results were the 16 Strategic Customer Agreements or SCAs it signed with customers operating in the data center, consumer, and automotive markets. Encouragingly, the company has received financial commitments of $22 billion for these deals, with $18 billion in cash deposits. This is crucial as it makes up more than 80% of the company's capital expenditure, amounting to $27 billion in fiscal 2026.

Also, the company revealed that the production of its HBM4E memory architecture, built on its 1-gamma technology, is expected to reach volume production in 2027. By utilizing the advanced 1-gamma node, Micron aims to deliver significant improvements in power efficiency and bandwidth compared to previous generations, ensuring it remains a key supplier for hyperscalers and AI chip designers.

Coming back to the Q3 numbers, for the nine months ended May 28, 2026, net cash from operating activities soared to $45.7 billion from $11.8 billion in the prior year. Overall, Micron ended Q3 2026 with a cash balance of $25 billion, with short-term debt of just $582 million.

Finally, even after such a potent rally, MU stock is trading at undervalued levels. Its forward price-to-earnings, price-to-sales, and price-to-cash flow of 16.58 times, 10.58 times, and 16.52 times are all below the sector medians of 23.72 times, 3.27 times, and 18.63 times, respectively.

For Micron, Stars Are Aligned

Some skeptics hint towards the cyclicality of the memory business and the impending listing of SK Hynix on U.S. exchanges as headwinds for Micron in the near future. Well, they do not need to be, as the macro scenario, coupled with Micron's inherent strengths, gives substantial growth visibility for the company.

In terms of the overall market, this report estimates that the demand-supply mismatch for memory chips will persist till 2028. Moreover, the demand for HBM or High Bandwidth Memory among hyperscalers is adding to the pressure, as HBM requires a wafer area per gigabyte of about three times more than standard DRAM.

So, demand is going nowhere.

For Micron, what works in its favor, apart from its Western presence, is its 1-gamma technology, touched upon briefly earlier. Micron's 1-gamma DRAM node is achieving mature yields roughly 50% faster than prior process generations, providing the company with both a cost and performance lever heading into 2026.

On the resulting HBM4 product itself, Micron's HBM4 achieves pin speeds over 11 gigabits per second, enabling bandwidth greater than 2.8 terabytes per second, a 2.3 times bandwidth improvement, and more than 20% better power efficiency compared to HBM3E. Micron began high-volume shipment of its HBM4 36GB 12-high configuration in the first quarter of calendar 2026, specifically designed for Nvidia's Vera Rubin platform, and has also demonstrated 16-die stacking by shipping samples of an HBM4 48GB 16-high variant to customers, a 33% capacity increase over the 12-high offering.

Notably, to service this demand, Micron is ramping up its production facilities across the globe, with the same moving aggressively outside the U.S., with a new plant in Tongluo, Taiwan expected to make product shipments by mid-2027.

Beyond Taiwan, Micron is investing $24 billion in a new Singapore plant, on top of a separate $7 billion advanced packaging facility being built specifically to produce high bandwidth memory. The new Fab 10B sits within Micron's existing 3D NAND campus at North Coast Wafer Fab Park, will eventually deliver up to 700,000 square feet of cleanroom space, more than double the combined 500,000 square feet of the existing Fab 10A and Fab 10X, and will be Singapore's first double-story wafer fab, configured to support next-generation 3D NAND nodes with over 500 active layers.

Japan is the other major new front. Micron is planning a $9.6 billion HBM fab at its Hiroshima site, with construction reportedly beginning in May 2026 and first HBM chip shipments targeted for 2028, a facility explicitly framed as Micron's attempt to close the gap with SK Hynix's current HBM leadership.

Domestically, beyond the well-known Idaho and New York megaprojects, Micron has been quietly expanding legacy capacity too. Micron began 1-alpha DRAM production at its Manassas, Virginia, fab in May 2026, a move designed to quadruple DDR4 wafer output at the site and secure long lifecycle DDR4 and LP4 memory supply for automotive, industrial, networking, medical, and defense customers. That Virginia expansion is backed by a non-binding $275 million Preliminary Memorandum of Terms with the Department of Commerce under the CHIPS Act, supporting a roughly $2 billion modernization of the facility.

Analyst Opinion

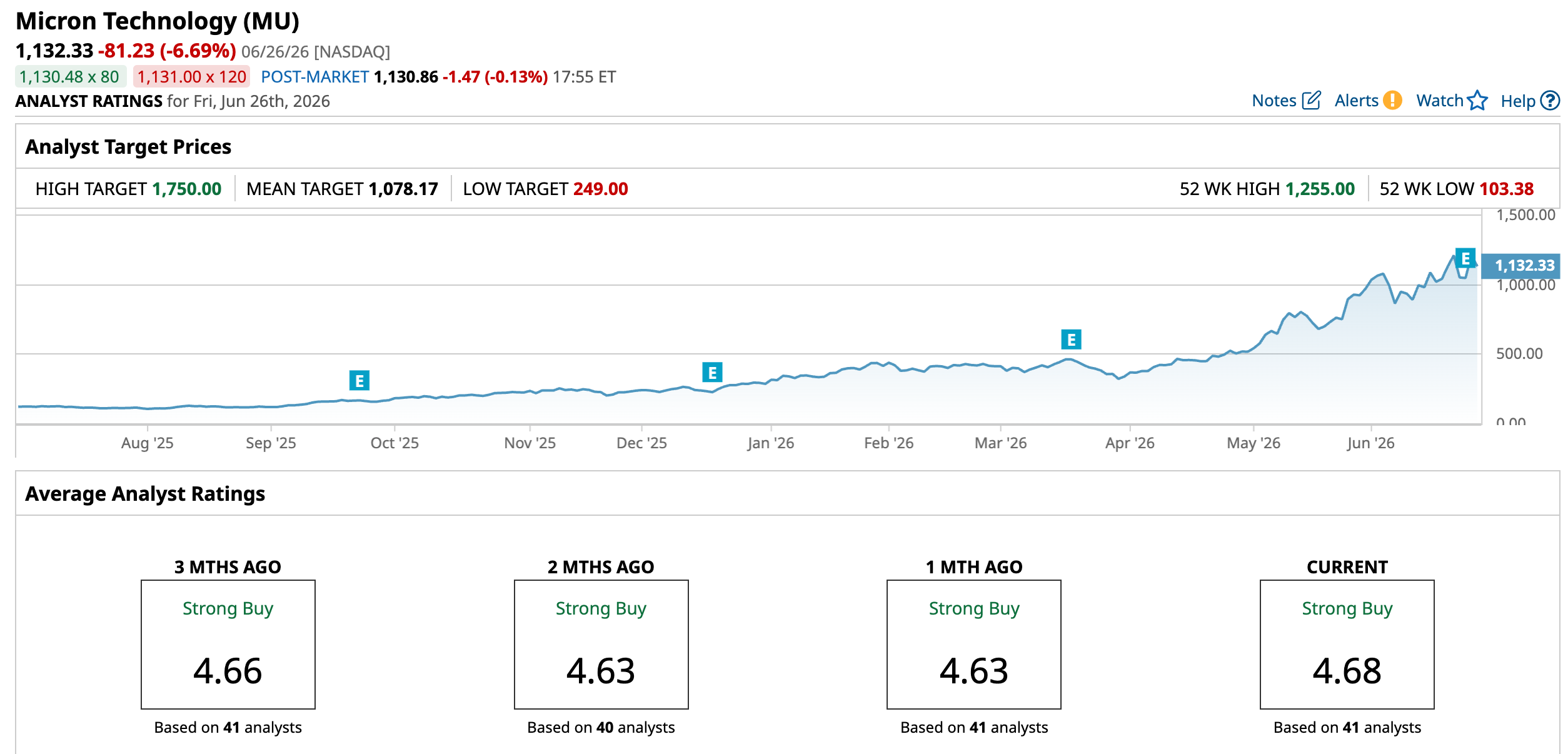

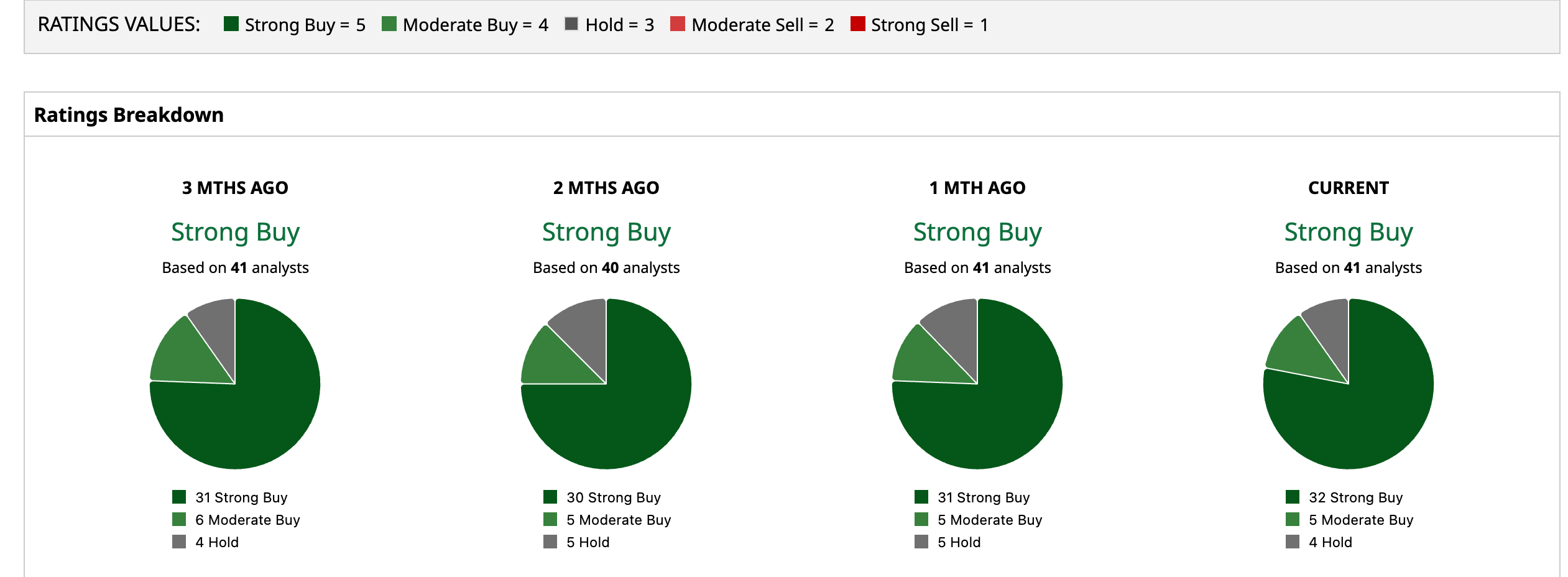

Overall, analysts continue to remain bullish on Micron and, as such, have assigned its stock a rating of “Strong Buy”. The mean target price has already been surpassed, and the high target price of $1,750 indicates an upside potential of 54.6% from current levels. Out of 41 analysts covering the stock, 32 have a “Strong Buy” rating, five have a “Moderate Buy” rating, and four have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)