/Meta%20Platforms%20by%20Primakov%20via%20Shutterstock.jpg)

Recently, Meta Platforms (META) unveiled its new smart glasses in partnership with EssilorLuxottica (ESLOY), the parent company of Ray-Ban. What’s more important is that the glasses cost $299, which is at least $80 less than the price of the company’s entry-level second-generation Meta Ray-Ban glasses. Further, it’s much cheaper than last year's $800 premium Ray-Ban Display glasses.

This is another step in the company’s push into wearables as competition in the eyewear space heats up. The marketing has been aggressive, with Meta partnering with social media personality Kylie Jenner to promote the product's prescription lenses. On top of that, the glasses will be sold under Meta's own branding rather than established eyewear brands and will be laden with AI technology.

Against this backdrop, we take a closer look at Meta Platforms.

About Meta Platforms Stock

Meta Platforms is one of the world’s largest and most popular technology companies, operating major platforms like Facebook, Instagram, WhatsApp, and Messenger. Based in Menlo Park, California, it is investing heavily in artificial intelligence to improve products, strengthen infrastructure, and shape the future of digital communication and online engagement. The company has a market capitalization of $1.41 trillion.

Meta’s stock has been under pressure mainly because investors are questioning whether its heavy AI spending will deliver returns quickly enough, especially as capital expenditure continues to rise. The sell-off has also been tied to margin pressure and a large one-time tax hit last year.

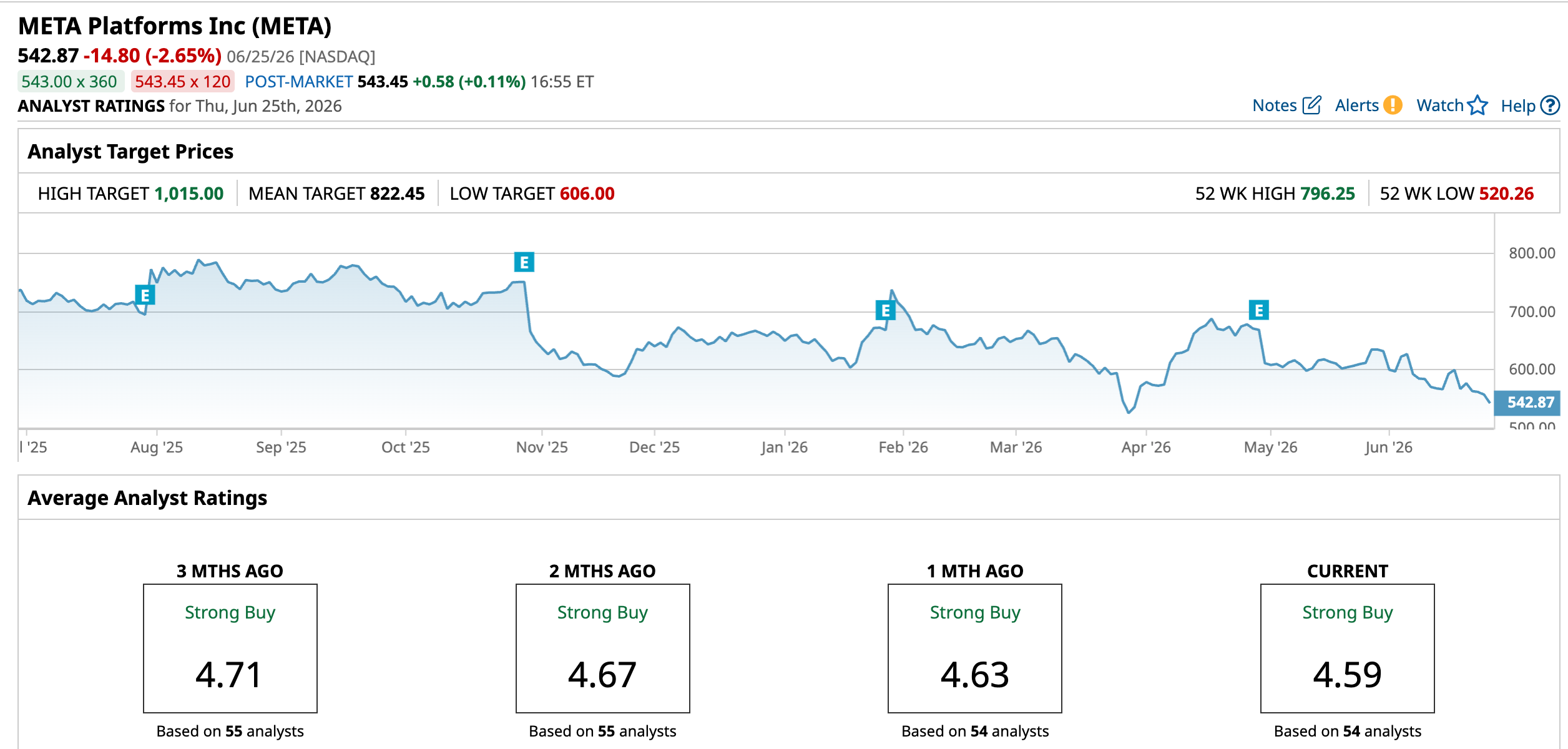

Over the past 52 weeks, Meta’s stock has dropped 23.4%, and it is down 17.76% year-to-date (YTD). For comparison, the broader Nasdaq Composite ($NASX) index is up 26.96% and 9.11% over the same periods, respectively. Meta’s shares reached a 52-week low of $520.26 on March 27, but are up 4.4% from that level.

On a forward-adjusted basis, Meta’s price-to-earnings Non-GAAP ratio of 17.33 times is higher than the industry average of 12.71 times.

Meta Platforms Reported Stellar Q1 Results Driven by Ad Growth

For the first quarter of 2026, Meta reported 33% year-over-year (YOY) revenue growth to $56.31 billion, while its advertising revenue climbed 33% YOY to $55.02 billion. Family daily active people averaged 3.56 billion in March 2026, up 4% from a year earlier. Revenue over its family of apps (which includes advertising revenue) also increased by 33% YOY to $55.91 billion.

Its Ad impressions across its Family of Apps rose 19% compared with the same period last year, while the average price per ad increased 12% YOY. Its EPS grew 62% YOY to $10.44. Its total income from operations increased by 30% from the prior-year period to $22.87 billion. However, its Reality Labs segment continues to report quarterly operating losses.

Meta’s capital expenditures also persist in growing. For fiscal 2026, the company increased its planned capex to $125 billion to $145 billion, up from its prior range of $115 billion to $135 billion, reflecting additional data center costs to support capacity.

Wall Street analysts have mixed feelings about Meta’s future earnings. For the current fiscal year, EPS is projected to decrease 1.2% annually to $29.35, followed by a 19.3% growth to $35.02 in the next fiscal year. Moreover, analysts expect the company’s EPS to decline marginally YOY to $7.10 for the current quarter.

What Do Analysts Think About Meta Platforms’ Stock?

RBC Capital recently kept its “Outperform” rating on Meta and maintained an $810 price target, saying the company sits at the intersection of two growth themes: more specialized computing power and rising AI-led entrepreneurship. Rosenblatt also reiterated a “Buy” rating and a Street-high $1,015 target after Meta outlined plans to launch subscription options for its key consumer products under the Meta One brand.

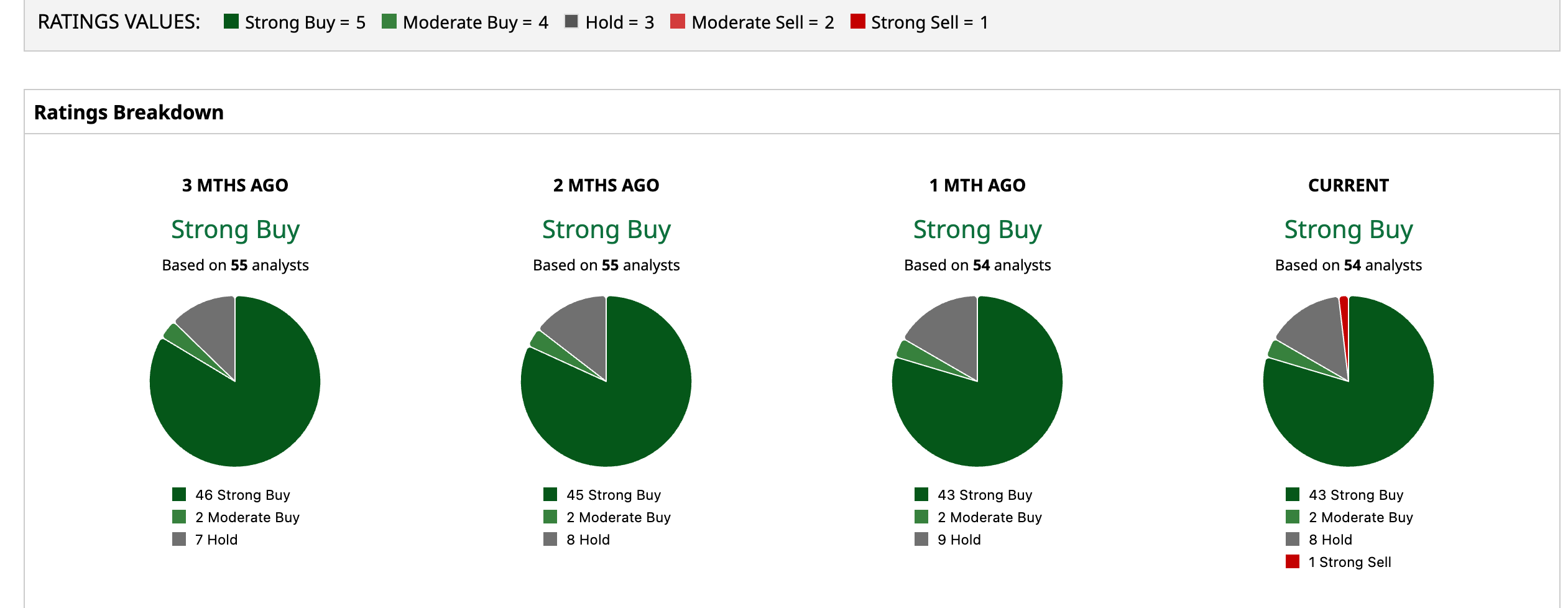

Meta has been in the spotlight on Wall Street, with analysts awarding it a consensus “Strong Buy” rating. Of the 54 analysts rating the stock, a majority of 43 analysts have rated it a “Strong Buy,” two analysts suggest a “Moderate Buy,” while eight analysts are playing it safe with a “Hold” rating, and one suggested “Strong Sell.” The consensus price target of $822.45 represents a 51.5% upside from current levels. The Street-high price target of $1,015 indicates an 87% upside.

Bottom Line

Meta is seeing more success in selling smart glasses rather than VR headsets at the moment. With RayBan's backing and a lower price tag, the smart glasses might be a hit with customers.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/United%20Parcel%20Service%2C%20Inc_%20logo%20on%20truck-by%20100pk%20via%20iStock.jpg)

/A%20close-up%20of%20the%20SpaceX%20sign%20on%20a%20black%20building%20by%20IanDewarPhotography%20via%20Adobe%20Stock.jpeg)