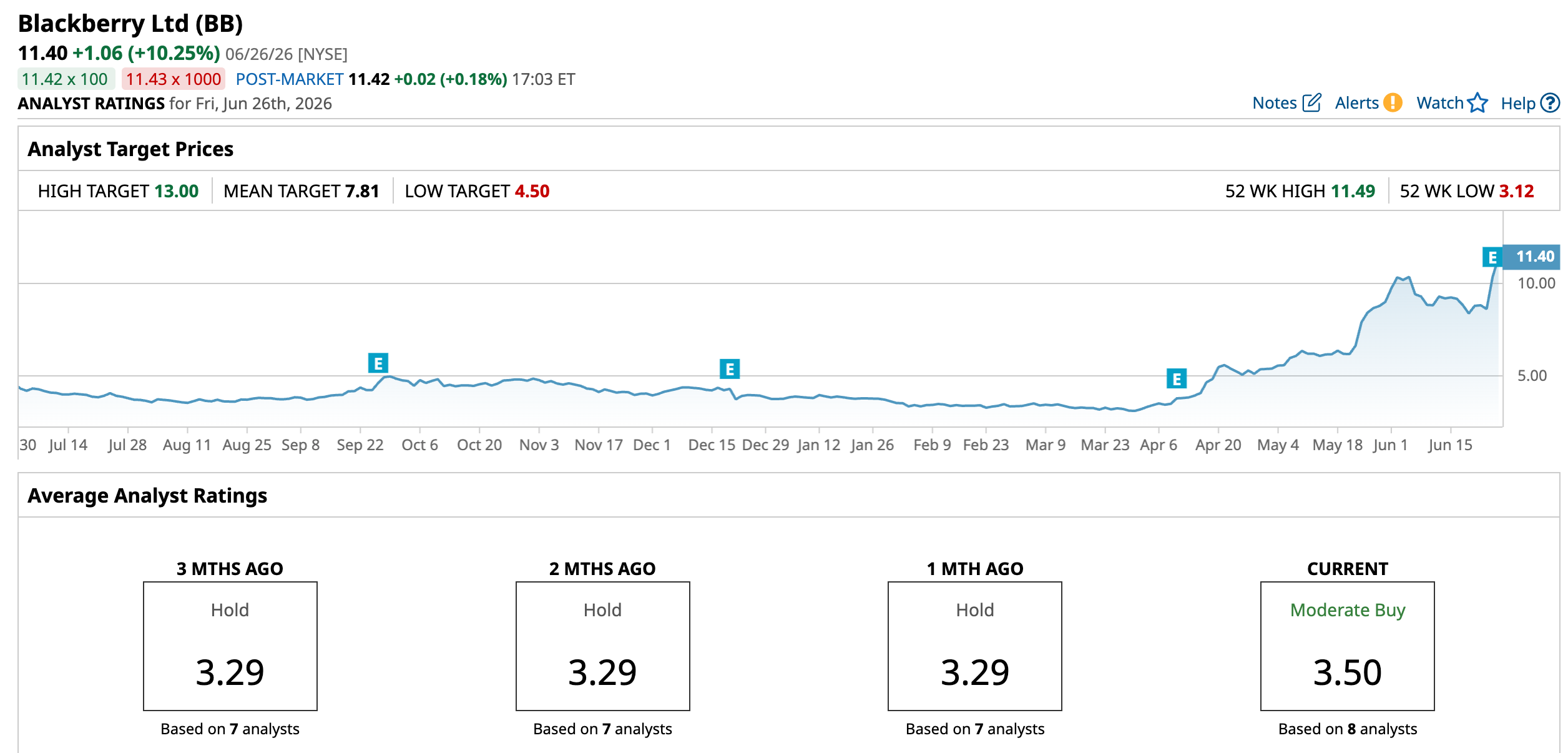

When a once‑famous tech name posts an earnings beat that sends the stock up double digits, people pay attention. BlackBerry’s (BB) shares jumped 19.95% after its June 25 earnings report, even though the stock is still more than 60% below levels from twenty years ago. The company reported revenue of $152.9 million, up 25.6% year‑over‑year (YOY), which suggests its shift toward software might finally be gaining real traction.

Those numbers have turned what was mostly a nostalgia ticker into a real turnaround debate. For a company still tied in many minds to its old smartphone days, a double‑digit post‑earnings move and steadily better fundamentals naturally raise a big question for investors. Is this the point where years of transformation finally start to pay off, or just another quick spike that fades away?

BlackBerry’s Post‑Earnings Snapshot

BlackBerry is a Canada‑based software company that builds automotive embedded operating systems, secure communications tools, and cybersecurity solutions for governments and businesses around the world.

It is headquartered in Waterloo, Ontario, and its shares are up a massive 200% YTD gain and 141.5% surge over the past 52 weeks.

The company is now valued at $6.06 billion, and investors are already paying a clear premium with a trailing price‑to‑earnings ratio of 60.82 times versus a sector median of 25.34 times and a forward multiple of 58.37 times compared with a sector median of 23.72 times.

Their most recent earnings update on June 25 tried to back up that optimism with better numbers on both revenue and profit. This report showed non‑GAAP earnings per share of $0.04, beating consensus by $0.01 and pointing to better operating leverage.

It also detailed revenue of $152.9 million, a 25.6% YOY increase that was more than $15 million above expectations. The QNX unit sat at the centre of that performance, with QNX revenue up 26% to $72.3 million in fiscal Q1.

This growth is supported by a royalty backlog of roughly $950 million, which gives good visibility into future auto‑related software revenue. Their Secure Communications arm helped as well, with the division coming out of years of decline as revenue rose 24% YOY to $73.6 million, helped by wins with customers such as the U.S. Internal Revenue Service and Germany’s Bundesbank.

BlackBerry’s QNX And Security Deals

BlackBerry’s pivot rests on two main areas that are actually moving the needle right now. QNX embedded software is doing most of the heavy lifting. The company has essentially rebuilt its operating system strategy around QNX, a real‑time operating system that has become a standard in the global automotive and critical‑systems space.

QNX sits inside the safety and infotainment systems of more than 275 million vehicles worldwide. It now brings in over half of BlackBerry’s total revenue and is pushing further into robotics, industrial automation, medical devices, and aerospace.

Secure Communications is the other key pillar, especially in defense and government. In April 2026, the company partnered with The IP Company to integrate its SecuSUITE platform into The IP Company’s Wireless Communication & Messaging System (WCMS). The platform is certified to top international security standards, including CSfC and NATO Restricted.

This communication system has been used across naval fleets for more than 20 years. The new collaboration targets naval and military environments worldwide, adding highly secure, certified voice and messaging in tough operating conditions.

Together, these moves show BlackBerry leaning into high‑margin, recurring software revenue in markets with slow but sticky sales, where contract wins can support growth for years.

What The Street Is Signaling On BB

Analysts are starting to treat BlackBerry less like a relic and more like a real earnings story again. For the quarter ending in August 2026, the Street is looking for $0.03 in EPS, a small number on its own but a useful marker for whether the recent progress can stick.

Stifel’s move before the latest results stood out. The firm kicked off coverage with a “Buy” rating and a $12 price target, which implies 5.3% upside from current levels and signals real conviction in the turnaround. That call also pegs fiscal 2027 revenue at about $602 million, close to 10% growth and a noticeable shift for a business that spent years stuck in neutral.

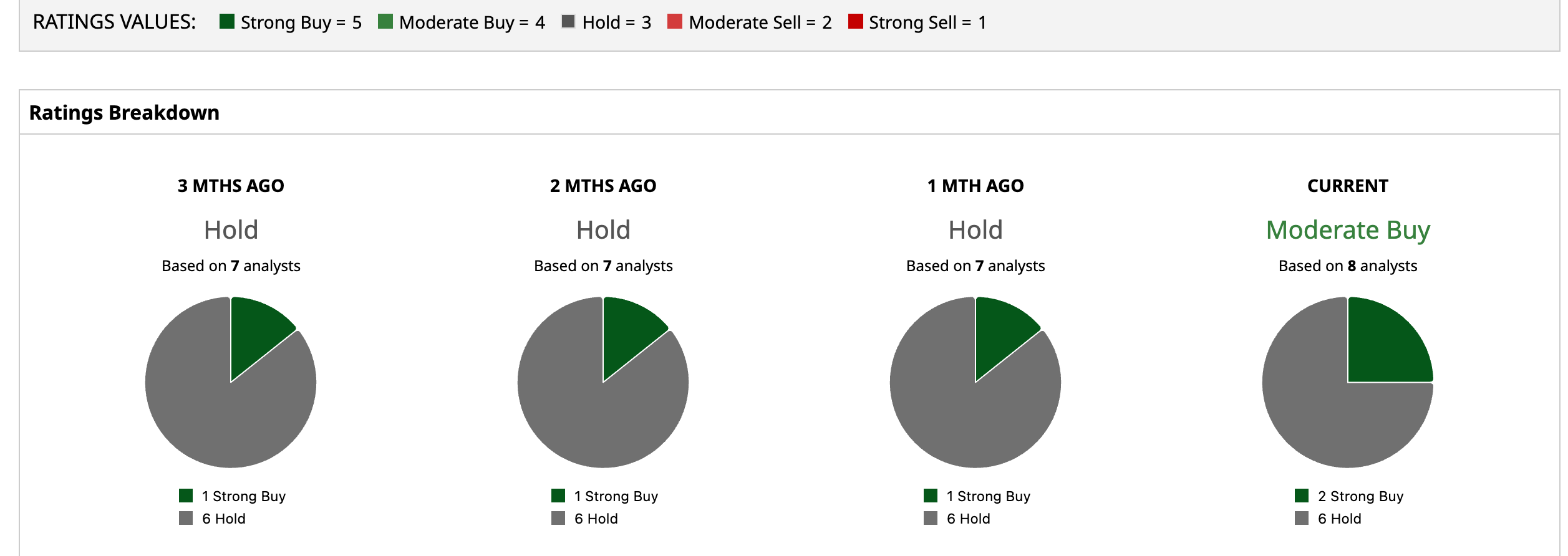

Across the wider coverage list, the tone is more cautious but clearly improving. A total of eight analysts now land on a “Moderate Buy” consensus, suggesting the balance has tilted toward the bulls, even if not everyone is convinced yet. The average price target is $7.81, representing 31.5% downside from the stock's current trading price.

Conclusion

BlackBerry finally looks like more than a nostalgia trade. A clean earnings beat, solid growth from QNX and Secure Communications, and a 20% jump in the share price all point to a turnaround that is starting to show up in the numbers. This is not “mission accomplished” yet, but it does look like the most convincing shift the stock has seen in years. With a high target of $13 backing up where the shares trade now, the near‑term risk‑reward leans more toward further upside than a drop back to the bargain bin.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Renewable%20Energy%20by%20Yuri%20Hoya%20via%20Shutterstock.jpg)

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)