The market doesn't always reward a good quarter right away, and Cerebras Systems (CBRS) may be the latest example. Shares of Cerebras – which designs AI chips and develops AI infrastructure and is a potential rival to AI giant Nvidia Corporation (NVDA) – tumbled after reporting its first earnings results as a publicly traded company. Investors zeroed in on near-term gross margin concerns. But several Wall Street analysts argue the market may be missing the forest for the trees.

Morgan Stanley, for one, is bullish on Cerebras. Instead of backing away after the post-earnings dip, analyst Joseph Moore reiterated his “Overweight” rating and lifted his price target to $273 from $250. His view is that the softer margin outlook reflects conservative guidance rather than weakening demand. In fact, the analyst believes Cerebras is playing the long game as it builds out one of the world’s largest AI cloud businesses.

So, while the stock stumbled after earnings, Wall Street’s smart money is not waving the white flag. If anything, analysts appear to be treating the pullback as a bump in the road rather than the end of the journey. And that’s a reminder that sometimes the market focuses on the next quarter while investors with a longer horizon keep their eyes on the bigger prize.

About Cerebras Stock

Founded in 2015 and headquartered in Sunnyvale, California, Cerebras Systems is one of the fastest-rising names in AI hardware. The company has built its reputation around the Wafer-Scale Engine (WSE), a processor carved from an entire silicon wafer that is designed to train and run AI models far faster than conventional chips.

Its CS-2 and CS-3 systems serve cloud providers, enterprises, research institutions, and government-backed AI projects. With operations spanning multiple regions and a market capitalization of $36.3 billion, Cerebras is rapidly positioning itself as a credible challenger in the booming AI infrastructure market.

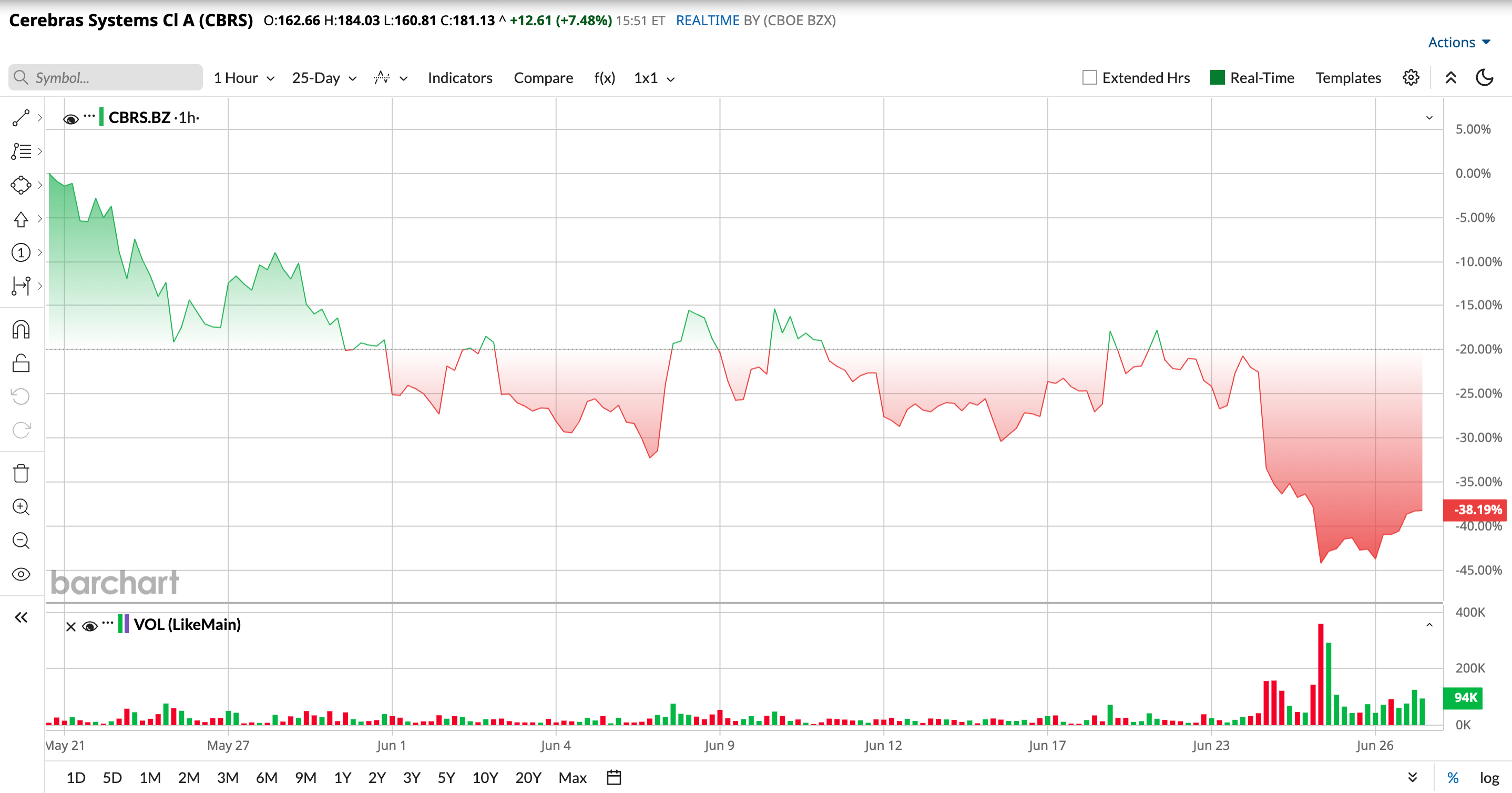

If there’s one word to describe CBRS stock since its IPO, it is volatile. The AI chipmaker entered the public market in May riding the same AI wave that has lifted much of the semiconductor sector, and investor appetite proved even stronger than expected.

On May 14, CBRS soared nearly 68%, finishing at $311.07 after touching an intraday high of $386.34. For a while, it looked like Cerebras could do no wrong. Then reality set in. As the IPO buzz faded, investors began taking a harder look at the company’s rich valuation, and broader enthusiasm across AI stocks cooled. Shares gradually drifted back toward the low-$200 range before finding support.

Momentum picked up again earlier this month after the post-IPO quiet period expired. A string of bullish analyst initiations helped reignite optimism, with Wall Street highlighting Cerebras’ fast-inference technology and long-term AI opportunities.

The latest twist came after the company's first quarterly earnings report. Although the results were strong, management's guidance for lower gross margins rattled investors. The stock dropped 19.6% on June 24 and fell another 7.5% the following session. Over the past month, CBRS has declined 24.9%, including a 22.6% slide in just the last five trading days, showing that while the long-term AI story remains intact, the road ahead is unlikely to be a smooth one.

Cerebras’ First Earnings Report as a Public Company Packed Plenty of Positives

For a company that’s only been public for a few weeks, Cerebras delivered a strong first impression. Its first-quarter fiscal 2026 results, released on June 23, showed that demand for its AI hardware and cloud platform continues to accelerate, while profitability is steadily moving in the right direction.

Core revenue jumped 92.3% year-over-year (YOY) to $191.3 million. Hardware remained the largest contributor, with revenue climbing 60% annually to $111.6 million, but the real standout was the Cloud and Other Services business, where revenue surged 167.4% YOY to $79.8 million. That mix matters because cloud services typically carry higher margins and generate more recurring revenue over time.

Profitability took a meaningful step forward. Core gross profit rose 112.4% to $89.1 million, lifting the company’s core gross margin to 46.5%, up from 42.1% a year ago. Hardware generated a respectable 42% gross margin, while the higher-value cloud business posted an even stronger 52.9% margin.

The losses continued to shrink as the business scaled. Core operating loss narrowed 81.8% to $3.5 million, while core net loss fell 83.1% to $2.5 million. Perhaps the biggest milestone was adjusted EBITDA, which swung to a $12.7 million profit from a $15.4 million loss in the same quarter last year.

Additionally, the balance sheet gives Cerebras room to keep investing aggressively. The company ended the quarter with $1.7 billion in cash and cash equivalents, more than doubling from $701.7 million at the end of 2025.

Beyond the numbers, Cerebras continued expanding its AI ecosystem. Alongside its high-profile OpenAI partnership, the company launched a multi-year agreement with Amazon's (AMZN) Amazon Web Services to deliver high-speed AI inference globally, broadening its reach across startups, AI-native businesses, and large enterprises.

Looking ahead, management expects Q2 core revenue of about $194 million, representing 88% YOY growth. It guided for a core gross margin of 36% to 38% and a core operating margin of negative 30% to negative 32%. For the full fiscal year, Cerebras forecasts $855 million to $865 million in core revenue – roughly 69% annual growth at the midpoint – along with core gross margins of 38% to 41%. While margins are expected to fluctuate as the company rapidly expands its cloud infrastructure, management’s outlook suggests growth remains the top priority, with demand showing little sign of slowing.

While the company is still in growth mode, so profitability is not expected overnight. Wall Street projects a -$0.98 per share loss in fiscal 2026, followed by a sharp turnaround in 2027, when earnings are forecast to climb to $0.96 per share.

Why Morgan Stanley Is Still Betting on Cerebras

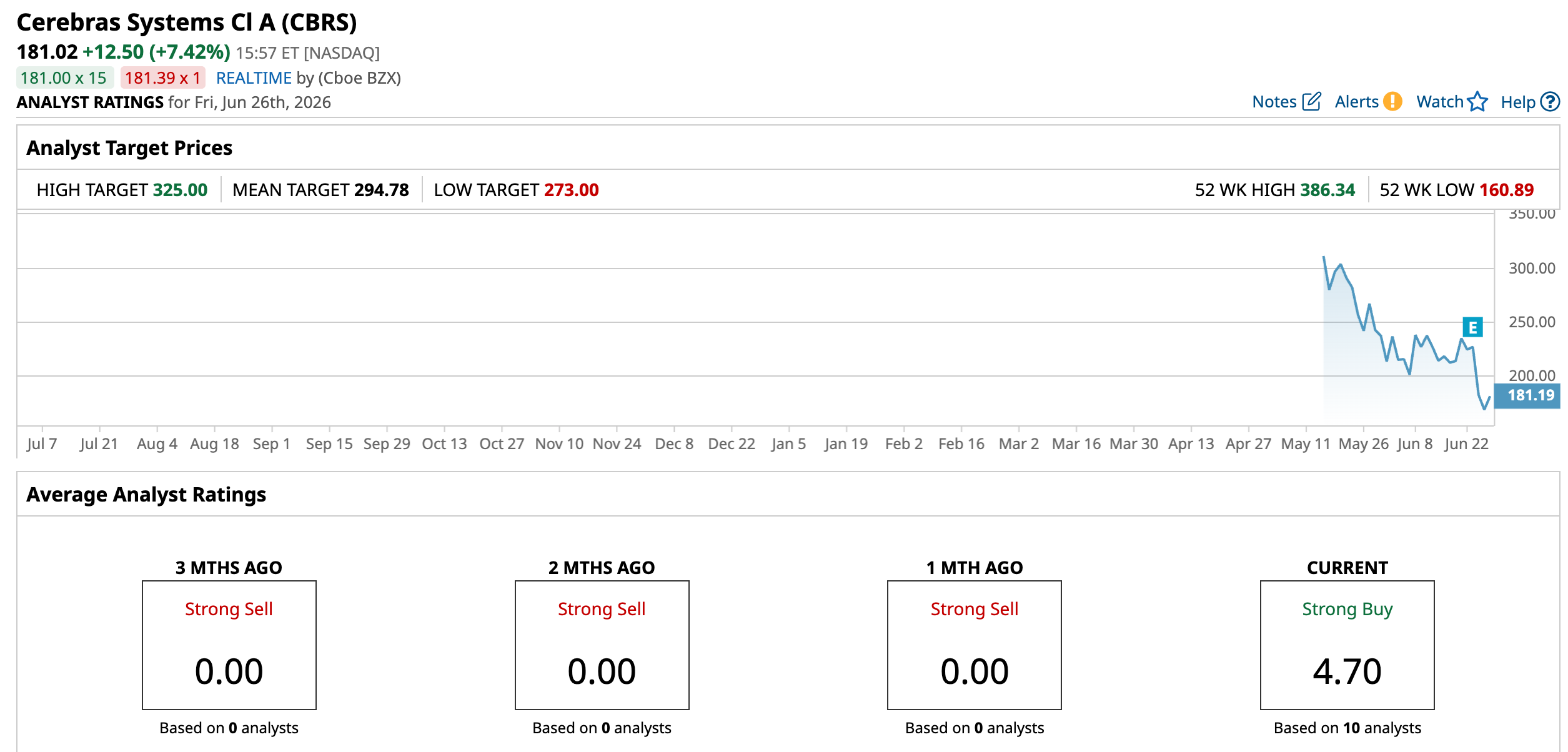

Cerebras may have stumbled after its first earnings report as a public company, but Morgan Stanley believes investors are getting caught up in the short-term noise. Analyst Joseph Moore kept his “Overweight” rating and raised his price target to $273 from $250, arguing that the company's long-term story remains firmly intact.

Moore called the first quarter a solid debut, saying the results were largely in line with expectations following the recent IPO. He believes management is deliberately setting conservative expectations, especially as Cerebras builds out its AI cloud business. While margins took a hit, that was not because demand is weakening. Instead, the company temporarily rented hardware from G42 to quickly meet customer demand while expanding its own cloud infrastructure.

Morgan Stanley sees the 750-megawatt OpenAI contract as the biggest growth engine over the next few years. Although the agreement gives OpenAI the option to buy hardware later, Moore continues to model it as a cloud-services business, viewing that as the more conservative assumption. He also highlighted that Cerebras is already supporting ChatGPT 5.4 and working on future AI models, underscoring the strength of its technology.

The firm also believes Amazon could become a bigger contributor over time. While the opportunity is still modeled conservatively, this week’s definitive agreement is an important milestone. Moore noted that once additional power and data center capacity come online, Cerebras should have more computing capacity available to expand its business with Amazon. In Morgan Stanley’s view, the near-term margin pressure is simply the cost of building a much larger AI infrastructure business, while demand remains as strong as ever.

What Are Other Analysts Saying After Cerebras’ Recent Selloff?

Morgan Stanley is not the only firm brushing off Cerebras’ post-earnings pullback. Other Wall Street analysts also came away encouraged, arguing that the company’s first report as a public company strengthened, rather than weakened, the long-term investment story.

Needham analyst N. Quinn Bolton reiterated his “Buy” rating and maintained a $300 price target after Cerebras topped expectations on both Q1 results and its 2026 revenue and gross margin outlook. Bolton pointed to strong customer demand, improving cloud pricing, and faster-than-expected margin improvement as key reasons for his optimism.

He also highlighted that OpenAI’s GPT-5.4 is already running on Cerebras hardware, with work underway to bring GPT-5.5 onto the platform. Another bright spot was Cerebras’ newly finalized agreement with Amazon Web Services, where Trainium3 chips will handle prefill while Cerebras’ CS-3 systems perform decode. Needham expects that partnership to begin contributing meaningful revenue in 2027. The brokerage firm also noted that Cerebras’ biggest hurdle is not chip supply, but it is simply having enough data center capacity to meet demand.

Meanwhile, Wedbush analyst Matt Bryson kept his “Outperform” rating and raised his price target to $280 from $270. Bryson said the company’s inaugural earnings report largely reinforced his bullish thesis. He believes management is setting realistic targets that leave room to outperform, while stronger pricing validates the value of Cerebras’ technology. More importantly, Bryson sees the OpenAI and Amazon partnerships as powerful long-term growth drivers that significantly reduce the risk of the company falling short of expectations.

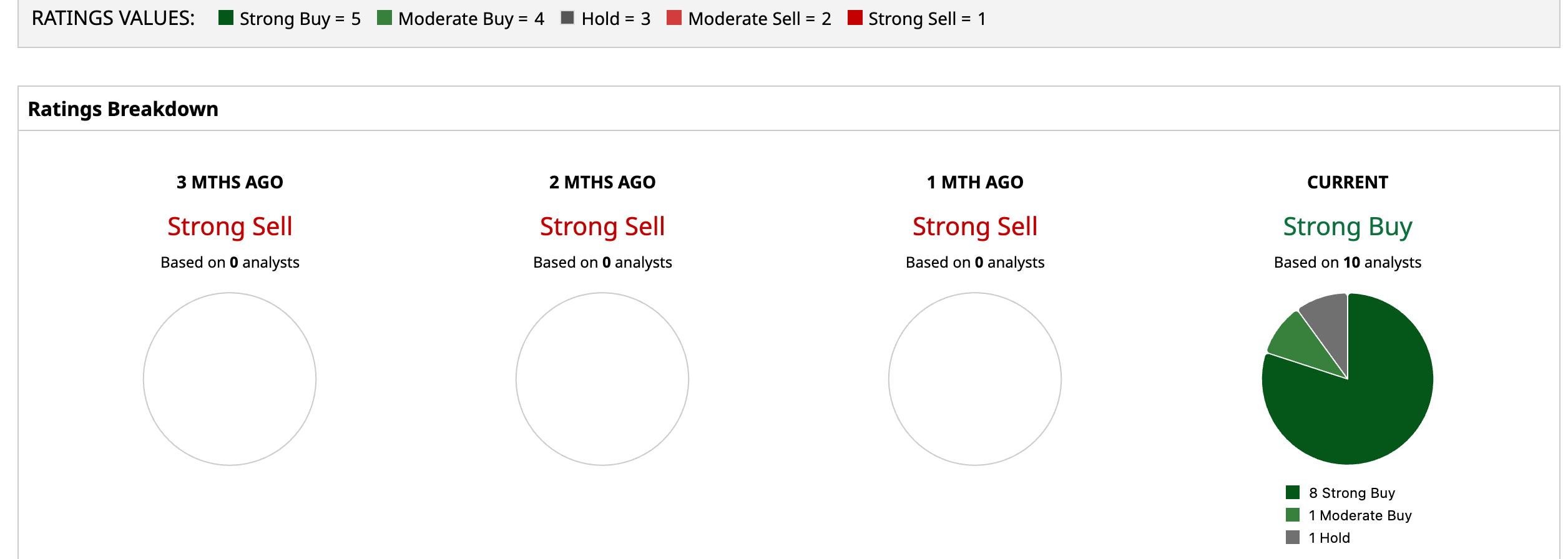

Wall Street is overwhelmingly bullish on CBRS. The stock carries a consensus “Strong Buy” rating, with eight of 10 analysts covering the stock recommending a “Strong Buy,” one has a “Moderate Buy,” and the remaining one analyst assigning a “Hold” rating.

The average analyst price target suggests CBRS has an upside potential of 62.8% from the current level. The Street-high target of $325 implies the stock could rally as much as 79.5%.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)