/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

After a strong rally, Qualcomm (QCOM) has lost momentum. The stock has fallen 14.6% from its recent high and is down 20.13% over the past month, reflecting valuation concerns and a challenging smartphone market.

The recent pullback comes after Qualcomm's sharp three-month rally pushed its valuation to elevated levels. At the same time, rising demand for AI infrastructure has tightened memory supply, driving up memory prices and increasing costs for smartphone manufacturers. The impact has been particularly evident in China, where many handset makers have scaled back production plans and reduced inventory levels.

As a result, Qualcomm's QCT Android handset business in China continues to face near-term pressure. Management expects revenue from Chinese handset customers to bottom in the third quarter before returning to sequential growth in the following quarter.

Despite these headwinds, Qualcomm's long-term growth story remains intact. The company has solid opportunities in automotive, AI-powered edge computing, and data centers.

Qualcomm Is Becoming Much More Than a Smartphone Chip Company

For decades, Qualcomm's business was driven by strong demand from the smartphone industry. While its mobile processors and modem chips continue to generate a significant amount of revenue, QCOM is no longer relying on smartphones as its primary growth engine.

Instead, Qualcomm is transforming itself into a diversified AI and semiconductor powerhouse. That strategy is beginning to pay off.

The company has expanded into high-growth markets, including automotive technology, IoT devices, industrial AI, robotics, and AI-powered data center infrastructure. These businesses not only reduce Qualcomm's dependence on the cyclical smartphone market but also position the company to benefit from some of the semiconductor industry's fastest-growing trends.

Management's long-term financial targets reflect that confidence. Recently, Qualcomm doubled its fiscal 2029 non-handset revenue target to $40 billion, highlighting the accelerating contribution from businesses outside smartphones. Moreover, Qualcomm also focuses on data center revenue of more than $15 billion by 2029.

Automotive remains another major growth pillar. Qualcomm expanded its automotive design-win pipeline to $65 billion and now expects the segment to generate $10 billion in revenue by fiscal 2029. Meanwhile, the company is extending its AI platform into robotics and industrial automation, and is focusing on Physical AI opportunities.

Looking further ahead, Qualcomm expects agentic AI to drive a new upgrade cycle across intelligent edge devices. Combined with long-term opportunities in AI infrastructure, autonomous driving, industrial AI, and eventually 6G, these markets can fuel solid growth well beyond 2029.

Thanks to solid growth prospects, Qualcomm is targeting adjusted earnings per share (EPS) of more than $18 by fiscal 2029.

ByteDance Deal Could be Major Win

Qualcomm is reportedly in talks with China's ByteDance, the parent company of TikTok, to provide chip-design services. If the deal goes through, ByteDance would give Qualcomm’s chip-design business a significant boost.

The partnership could come at a crucial time for Qualcomm. The company has faced headwinds this year as rising memory chip prices have pressured smartphone manufacturers, creating uncertainty for its core business. Securing ByteDance as a customer could diversify Qualcomm's revenue streams and strengthen investor confidence in its long-term growth strategy.

Is Qualcomm Stock a Buy?

Qualcomm's pivot toward automotive, AI edge computing, industrial AI, and data center is creating multiple growth engines beyond handsets. Potential design wins, including the reported ByteDance partnership, could further validate its diversification strategy.

While the pullback has made Qualcomm's valuation attractive, near-term weakness in the smartphone market could still limit the upside potential. Also, its margins are expected to remain under pressure due to the weaker handset business.

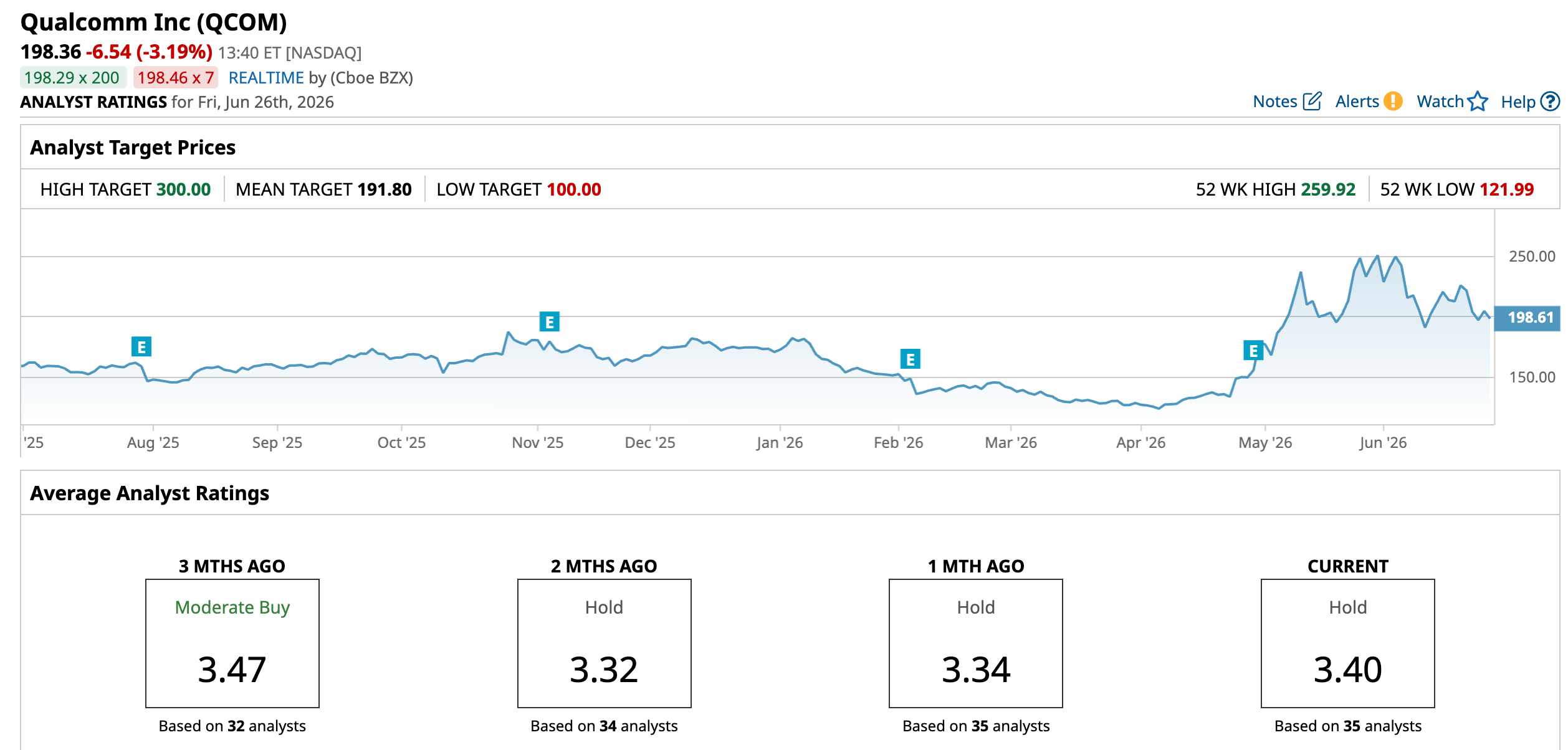

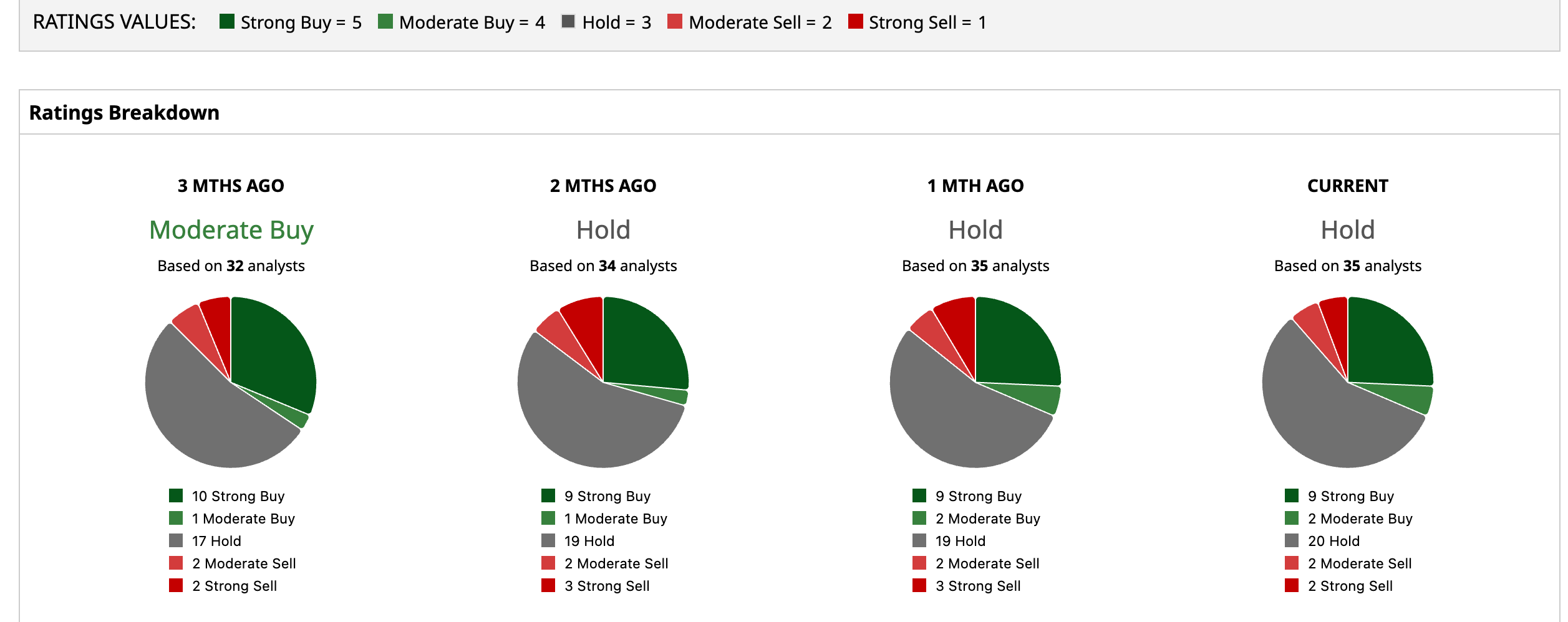

Given the short-term challenges, Wall Street analysts maintain a “Hold” consensus rating on QCOM stock.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)