/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

Jefferies upgraded FuelCell Energy (FCEL) to a “Buy” on Friday, simultaneously raising its price target to $24. The upgrade was catalyzed by FCEL’s newly announced strategic partnership with Fit Energy U.S., which establishes a multi-phase agreement to supply up to 380 megawatts of clean baseload fuel cell power for data center infrastructure.

Including today’s pop, FuelCell stock is trading up more than 225% versus the start of this year.

Why Jefferies Upgraded FuelCell Stock

The Jefferies analyst characterized FCEL shares' investment narrative as having shifted from a speculative “show me” story to one centered on executing against a visible and growing backlog.

The firm specifically highlighted what it called a “deep valuation discount” relative to competitor Bloom Energy (BE), describing the current entry point as offering asymmetric upside for investors.

This framing suggests Jefferies believes the market has not yet fully priced in the commercial momentum emerging from the Fit Energy deal and the broader data center power opportunity.

A Sneak Peek Into Fit Energy Deal

The Fit Energy agreement includes an immediate deposit for an initial 30 MW commitment, with deliveries expected to begin later in 2026.

Subsequent phases give Fit Energy options to trigger expansions of 100 MW, followed by two 125 MW phases, all anchored by milestone-based payments and long-term service agreements spanning 15 to 20 years.

The structure includes warrants for Fit Energy to purchase up to 12 million FuelCell shares at $26.44 each, vesting only as deployment milestones are met, aligning customer incentives with execution.

AI Boom Could Drive FCEL Shares Higher

The broader investment thesis for FCEL stock rests on surging AI and data center power demand.

FuelCell’s second-quarter commercial pipeline reached 4 GW, up a whopping 267% sequentially, with about 89% of proposals tied to data centers.

The clean energy company’s standardized 12.5 MW FuelCell Energy Block is designed to reduce engineering and permitting complexity, helping projects advance faster in grid-constrained markets.

According to CEO Jason Few, the Fit Energy agreement validates the company’s decision to scale production capacity to 500 MW.

The Risks of Owning FuelCell Energy

Despite the bullish momentum, significant risks remain. FuelCell reported a gross loss of $12.9 million and a net loss of $77.6 million in the most recent quarter on revenues of just $35.6 million.

Management has indicated that adjusted EBITDA positivity depends on reaching at least 100 MW of annualized production, versus roughly 30 MW currently.

The company's backlog actually declined 9.9% year-over-year to $1.14 billion as of April 2026, reflecting revenue burn-off that new contracts have only partially offset.

With nearly $441 million in total cash and restricted cash, FuelCell has liquidity to pursue growth, but the path from pipeline proposals to contracted revenue and ultimately profitability remains the central challenge investors must weigh against the Jefferies upgrade.

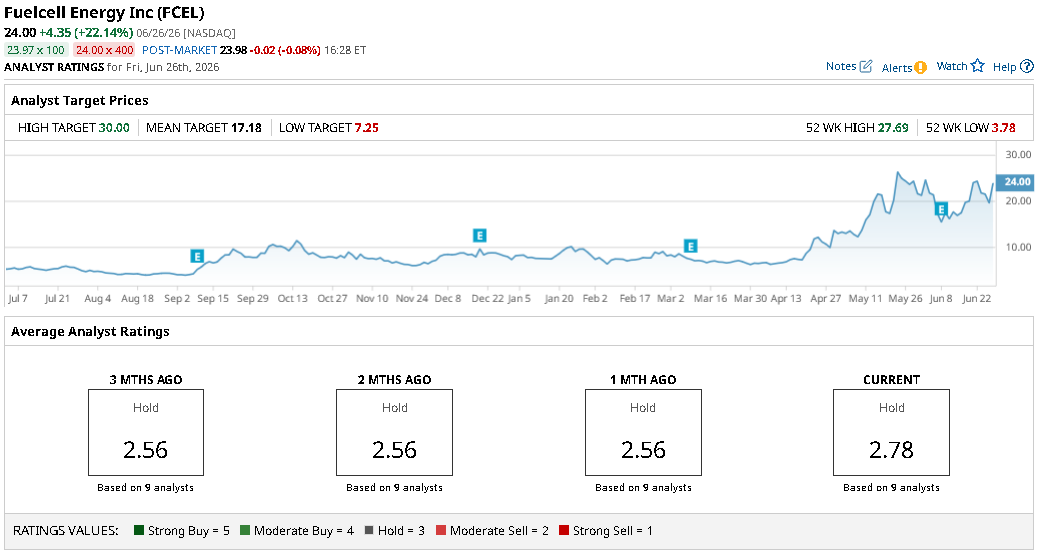

What’s the Consensus Rating on FCEL

Note that other Wall Street firms actually disagree with Jefferies constructive view on FCEL stock.

The consensus rating on FuelCell Energy sits at “Hold” only, with the mean price target of about $17 indicating potential for significant downside from current levels.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)