/Robinhood%20app%20on%20phone%20by%20Andrew%20Neel%20via%20Unsplash.jpg)

Robinhood (HOOD) shares are expensive relative to their fintech peers in 2026, but that premium is rather “warranted,” says BTIG’s senior analyst Andrew Harte.

At the time of writing, HOOD is going for a forward price-to-earnings (P/E) multiple of about 54x, versus a much more modest 29x on the likes of SoFi Technologies (SOFI).

Robinhood stock has been an exciting investment in recent months, currently up nearly 50% versus its low in late March.

The Bull Case for Robinhood Stock

Harte expects HOOD shares to rip higher as management continues to deliver on its promise of transforming the platform into a “one-stop shop” for retail investing and personal finance.

He initiated coverage of Robinhood this morning with a “Buy” rating, tied to an aggressive $125 price target that signals potential upside of another 28% from current levels.

BTIG remains bullish on the fintech firm given “the combination of low TAM penetration, a client base still in the early stages of its wealth accumulation journey, and a vast product suite.”

Note that Robinhood has a history of gaining nearly 10% on average in July — a seasonal trend that makes it even more attractive for the near term.

HOOD Shares Experienced a Technical Breakout Today

Andrew Harte remains convinced that HOOD is well-positioned to sustain platform asset growth at 20% “for years to come.”

Other reasons the BTIG analyst cited for the positive stance in his research note include the firm’s venture into prediction markets and its launch of tokenized U.S. stocks for EU customers last year.

All in all, Robinhood shares are poised for continued gains on the back of increasing engagement, new customer additions, and product and geographical expansion, he concluded.

Note that HOOD pushed past its 20-day moving average (MA) today, signaling bullish momentum could be sustained in the near term.

Robinhood Remains Buy-Rated Among Wall Street Firms

While not as bullish as BTIG, Robinhood remains in favor with other Wall Street analysts as well.

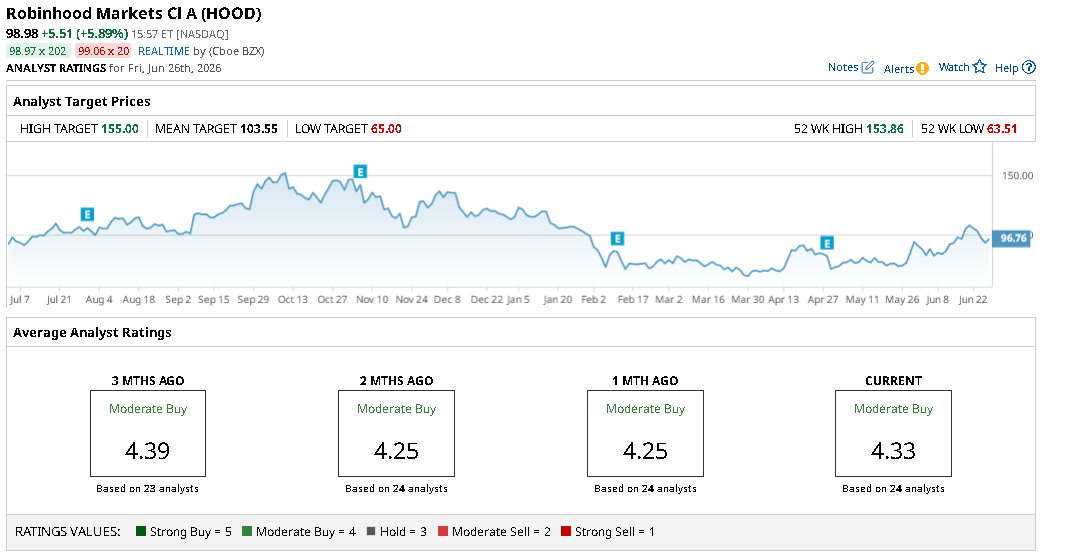

The consensus rating on HOOD stock sits at “Moderate Buy” currently, with the mean price target of roughly $104 indicating potential for a 7% rally from here.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)