Call center software provider Five9 (NASDAQ: FIVN) beat analysts' expectations in Q2 CY2024, with revenue up 13.1% year on year to $252.1 million. On the other hand, next quarter's revenue guidance of $255 million was less impressive, coming in 4.6% below analysts' estimates. It made a non-GAAP profit of $0.57 per share, improving from its profit of $0.52 per share in the same quarter last year.

Is now the time to buy Five9? Find out by accessing our full research report, it's free.

Five9 (FIVN) Q2 CY2024 Highlights:

- Revenue: $252.1 million vs analyst estimates of $245.1 million (2.8% beat)

- Adjusted Operating Income: $31.04 million vs analyst estimates of $26.18 million (18.5% beat)

- EPS (non-GAAP): $0.57 vs analyst estimates of $0.44 (30.2% beat)

- Revenue Guidance for Q3 CY2024 is $255 million at the midpoint, below analyst estimates of $267.2 million

- The company dropped its revenue guidance for the full year from $1.06 billion to $1.02 billion at the midpoint, a 3.8% decrease

- Gross Margin (GAAP): 53%, in line with the same quarter last year

- Free Cash Flow of $8.09 million, down 52.9% from the previous quarter

- Billings: $250.1 million at quarter end, up 12.6% year on year

- Market Capitalization: $3.05 billion

Started in 2001, Five9 (NASDAQ: FIVN) offers software as a service that makes it easier for companies to set up and efficiently run call centers, and offer more tailored customer support.

Video Conferencing

Work is becoming more distributed, both across geographies and devices. In order for businesses to keep functioning efficiently, they need to be able to communicate as well as they did when the teams were co-located, which drives the demand for integrated communication platforms.

Sales Growth

As you can see below, Five9's 22.9% annualized revenue growth over the last three years has been decent, and its sales came in at $252.1 million this quarter.

This quarter, Five9's quarterly revenue was once again up 13.1% year on year. However, its growth did slow down compared to last quarter as the company's revenue increased by just $5.08 million in Q2 compared to $7.95 million in Q1 CY2024. While we'd like to see revenue increase by a greater amount each quarter, a one-off fluctuation is usually not concerning.

Next quarter's guidance suggests that Five9 is expecting revenue to grow 10.8% year on year to $255 million, slowing down from the 16% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 19.4% over the next 12 months before the earnings results announcement.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

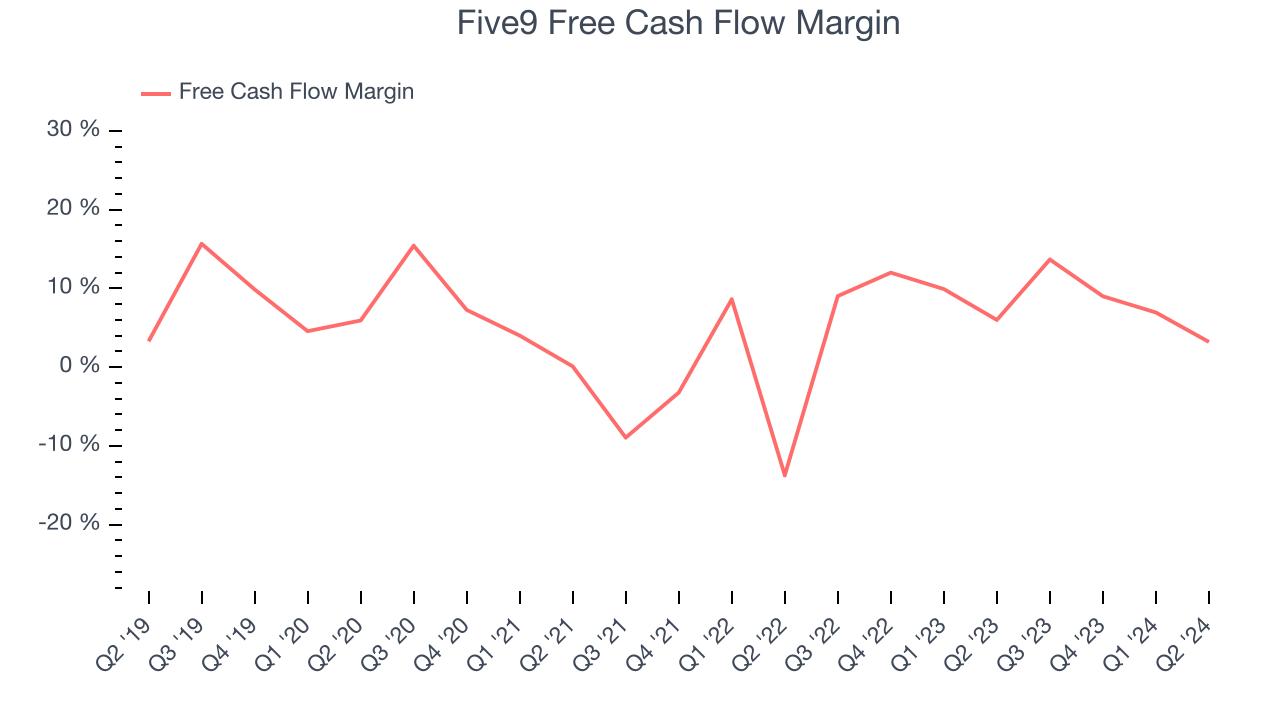

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Five9 has shown mediocre cash profitability over the last year, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 8.1%, subpar for a software business.

Five9's free cash flow clocked in at $8.09 million in Q2, equivalent to a 3.2% margin. The company's cash profitability regressed as it was 2.8 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren't a big deal because investment needs can be seasonal, but we'll be watching to see if the trend extrapolates into future quarters.

Over the next year, analysts predict Five9's cash conversion will improve. Their consensus estimates imply its free cash flow margin of 8.1% for the last 12 months will increase to 12.2%, giving it more money to invest.

Key Takeaways from Five9's Q2 Results

It was good to see Five9 beat analysts' billings expectations this quarter. We were also glad its revenue outperformed Wall Street's estimates. On the other hand, its full-year revenue guidance was below expectations and its revenue guidance for next quarter missed Wall Street's estimates. This quarter featured some positives but overall could have been better. The stock traded down 8.4% to $38.92 immediately after reporting.

Five9 may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)