Data-mining and analytics company Palantir (NYSE:PLTR) announced better-than-expected results in Q2 CY2024, with revenue up 27.2% year on year to $678.1 million. Guidance for next quarter's revenue was also optimistic at $699 million at the midpoint, 2.8% above analysts' estimates. It made a non-GAAP profit of $0.09 per share, improving from its profit of $0.05 per share in the same quarter last year.

Is now the time to buy Palantir? Find out by accessing our full research report, it's free.

Palantir (PLTR) Q2 CY2024 Highlights:

- Revenue: $678.1 million vs analyst estimates of $652.4 million (3.9% beat)

- Adjusted Operating Income: $253.6 million vs analyst estimates of $211.3 million (20% beat)

- EPS (non-GAAP): $0.09 vs analyst expectations of $0.08 (in line)

- Revenue Guidance for Q3 CY2024 is $699 million at the midpoint, above analyst estimates of $680.2 million

- The company lifted its revenue guidance for the full year from $2.68 billion to $2.75 billion at the midpoint, a 2.3% increase

- Gross Margin (GAAP): 81%, up from 80% in the same quarter last year

- Adjusted EBITDA Margin: 38.6%, up from 26.9% in the same quarter last year

- Free Cash Flow of $148.7 million, similar to the previous quarter

- Billings: $714.4 million at quarter end, up 27.5% year on year

- Market Capitalization: $55.09 billion

Started by Peter Thiel after seeing US defence agencies struggle in the aftermath of the 2001 terrorist attacks, Palantir (NYSE:PLTR) offers software as a service platform that helps government agencies and large enterprises use data to make better decisions.

Data Analytics

Organizations generate a lot of data that is stored in silos, often in incompatible formats, making it slow and costly to extract actionable insights, which in turn drives demand for modern cloud-based data analysis platforms that can efficiently analyze the siloed data.

Sales Growth

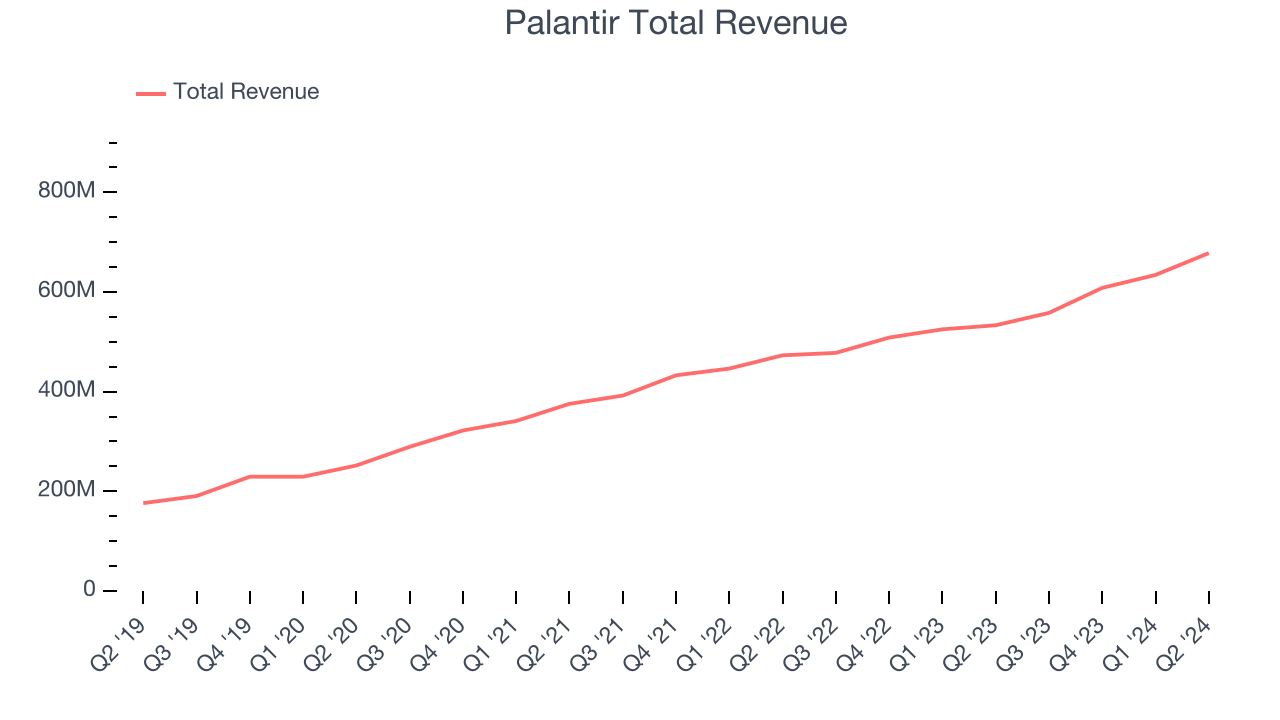

As you can see below, Palantir's revenue growth has been decent over the last three years, growing from $375.6 million in Q2 2021 to $678.1 million this quarter.

This quarter, Palantir's quarterly revenue was once again up a very solid 27.2% year on year. On top of that, its revenue increased $43.8 million quarter on quarter, a very strong improvement from the $25.99 million increase in Q1 CY2024. This is a sign of acceleration of growth and great to see.

Next quarter's guidance suggests that Palantir is expecting revenue to grow 25.2% year on year to $699 million, improving on the 16.8% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 19.4% over the next 12 months before the earnings results announcement.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Cash Is King

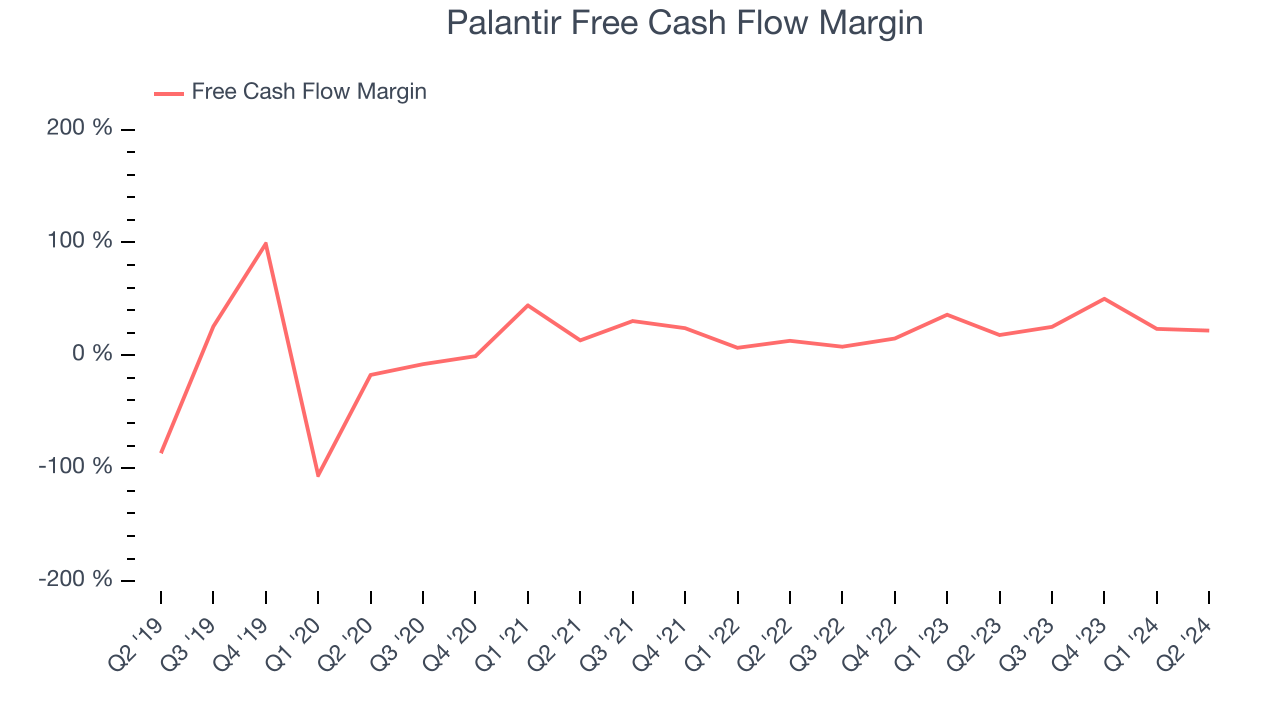

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Palantir has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company's free cash flow margin was among the best in the software sector, averaging 30% over the last year.

Palantir's free cash flow clocked in at $148.7 million in Q2, equivalent to a 21.9% margin. This quarter's result was good as its margin was 3.9 percentage points higher than in the same quarter last year, but we note it was lower than its one-year cash profitability. Nevertheless, we wouldn't read too much into a single quarter because investment needs can be seasonal, causing short-term swings. Long-term trends carry greater meaning.

Over the next year, analysts' consensus estimates show they're expecting Palantir's free cash flow margin of 30% for the last 12 months to remain the same.

Key Takeaways from Palantir's Q2 Results

We were impressed by how strongly Palantir blew past analysts' revenue, billings, and adjusted operating income expectations this quarter. We were also glad it raised its full-year revenue and adjusted operating income guidance, beating Wall Street's estimates. Zooming out, we think this was an impressive quarter that should delight shareholders. The stock traded up 16% to $27.94 immediately following the results.

Palantir may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)