/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

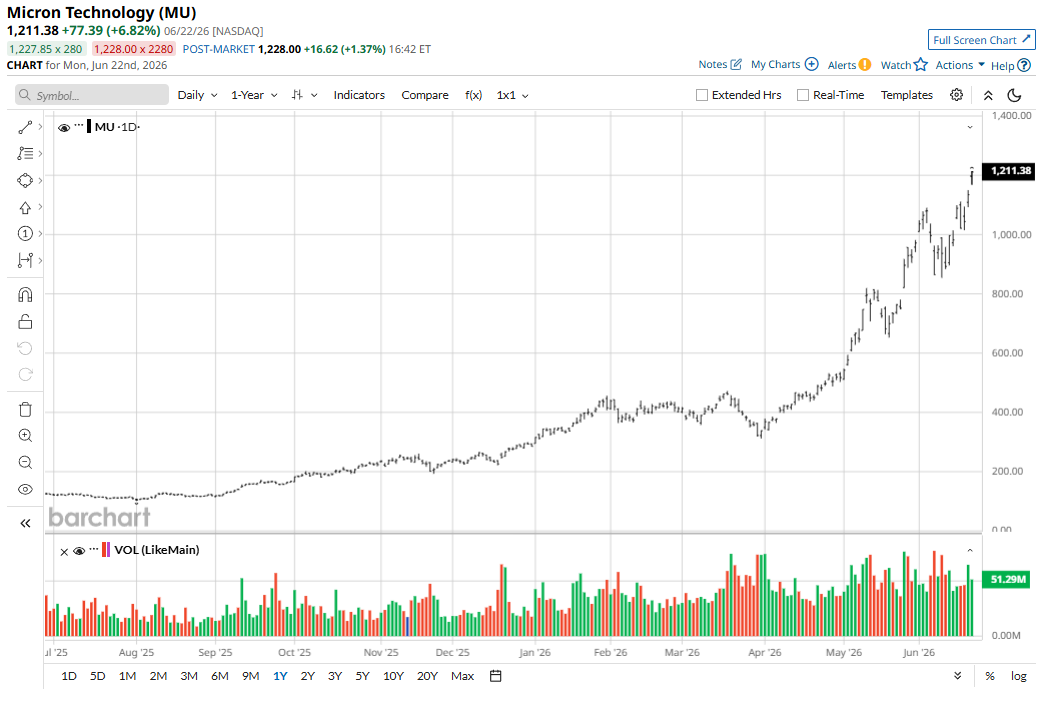

Micron's (MU) market capitalization has reached an astronomical $1.2 trillion. The market is currently in a state of intense euphoria regarding MU stock, easily granting the company a trailing price-to-earnings (P/E) ratio of 56.9 times. Bulls might argue that the forward P/E is only 20 times, and investors believe that the current windfall profits are guaranteed for the company for decades to come. However, in my view, this fundamental misperception is creating a dangerously overheated stock, driven by a misunderstanding of the nature of the manufacturing deficit. Reality operates by different rules.

The Formula for Delusion: Extrapolating to Infinity

The main mistake being made by market bulls lies in their belief that the shortage of high-bandwidth memory (HBM) will last forever.

Unquestionably, the old paradigm is dead. The era when demand obediently followed the cyclical, wave-like purchases of smartphones and personal computers is gone forever, giving way to AI clusters that devour silicon continuously in massive volumes. But investors are confusing a fundamental shift in consumption patterns with a mundane shortage of assembly lines.

Sky-high profits have nothing to do with a unique economic moat. They are simply the result of factories' physical inability to rapidly stack and package multi-layer chips. Sooner or later, this bottleneck in the memory market will clear up.

Oligopoly in Action: A Chronicle of the Coming Surplus

The memory industry has nothing in common with the comfortable dominance seen by the likes of Nvidia (NVDA). Here, competition among three apex predators — Samsung, SK Hynix, and Micron itself — rules the game. Hundreds of billions of dollars in cloud computing budgets are at stake. Naturally, no one is going to sit on the sidelines, which is why all three firms are currently flooding the market with capital expenditures, rolling out an unprecedented construction boom of new fabrication plants.

By the end of 2026, SK Hynix's M15X site in Korea will aggressively enter the fray, with its full ramp-up expected in mid-2027, alongside Micron's new packaging lines in Singapore. In 2027, the colossal Yongin mega-cluster will also launch, combining the efforts of Samsung and SK Hynix, while fresh Micron capacity will simultaneously come online in Idaho. The final chord will strike in 2028, when factories in Indiana and Hiroshima, Japan, are expected to reach their design capacity. The local deficit will persist for another couple of years. However, the competitive nature of the market will take its toll. These giants will single-handedly flood the industry with terabytes of new capacity.

The Math of Three Years' Profits

What does this mean for Micron in practice? The company will indeed skim the richest cream over the next two to three years, generating a massive amount of cash.

But let's apply some sober math. Three years of massive windfall profits only justify adding a +3 multiple to the company's fair value P/E (to account for the accumulated cash). After that, the period of super-profits will end. Therefore, it is impossible to extrapolate these three years of earnings far into the future and fully bake them into the P/E ratio.

Once the shortage disappears, stabilization will begin. To be clear, Micron won't collapse or regress. It will remain a massive, strong, and technologically powerful corporation, as demand from data centers will stay consistently high.

But the deficit will no longer exist. And without a deficit, the abnormal pricing premium will vanish. Memory prices will inevitably correct under the competitive pressure of the industry's three giants.

Conclusion

In my view, buying shares of Micron at current prices in the expectation of an endless AI fever borders on madness. In three years, the charts for profitability and absolute net income will inevitably take a nosedive. The fundamental laws of a capital-intensive economy and competition cannot be canceled out, even by the loudest hype. The stock market is pricing a permanent deficit into a situation that is merely a mundane, temporary delay in pouring the concrete foundations for new factories.

All told, the euphoria surrounding MU stock has gone too far, and long-term investors should exercise extreme caution.

On the date of publication, Mikhail Fedorov did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)