For years, Getty Images Holdings (GETY) looked like a company with its back against the wall. As generative AI exploded onto the scene, many critics saw the writing on the wall, arguing that machines capable of creating images on demand would turn stock photo libraries into yesterday’s news. Wall Street largely bought into that story, and Getty stock spent years fighting an uphill battle.

But as the old saying goes, if you cannot beat them, join them! And this week, in a move few saw coming, Getty Images struck a multi-year display agreement with OpenAI, putting its vast vault of licensed content directly into ChatGPT’s search and discovery experiences. The same AI wave that once threatened to pull the rug out from under Getty suddenly became its ace in the hole. Investors wasted no time connecting the dots, sending GETY stock soaring and nearly doubling the stock.

Details around the economics remain under wraps, but the force many believed would bury Getty Images may have just handed it a second act. And if analysts’ projections are accurate, this rally could still be just the tip of the iceberg.

About Getty Images Stock

Founded in 1995 and headquartered in Seattle, Washington, Getty Images is one of the world’s leading providers of visual content and media services. Through its flagship Getty Images brand, along with iStock and Unsplash, the company delivers photography, video, illustrations, and editorial content to businesses, media organizations, and creators across nearly every country. Its market capitalization currently stands at $481.8 million.

Its offerings span creative assets, news, sports, and entertainment coverage, as well as music licensing, digital asset management, and data services, serving clients worldwide. Getty also owns one of the world’s largest privately held photographic archives. As artificial intelligence reshapes the industry, the company has expanded into AI-powered content solutions built on licensed and permissioned imagery, providing customers with commercially safe tools and legal protections.

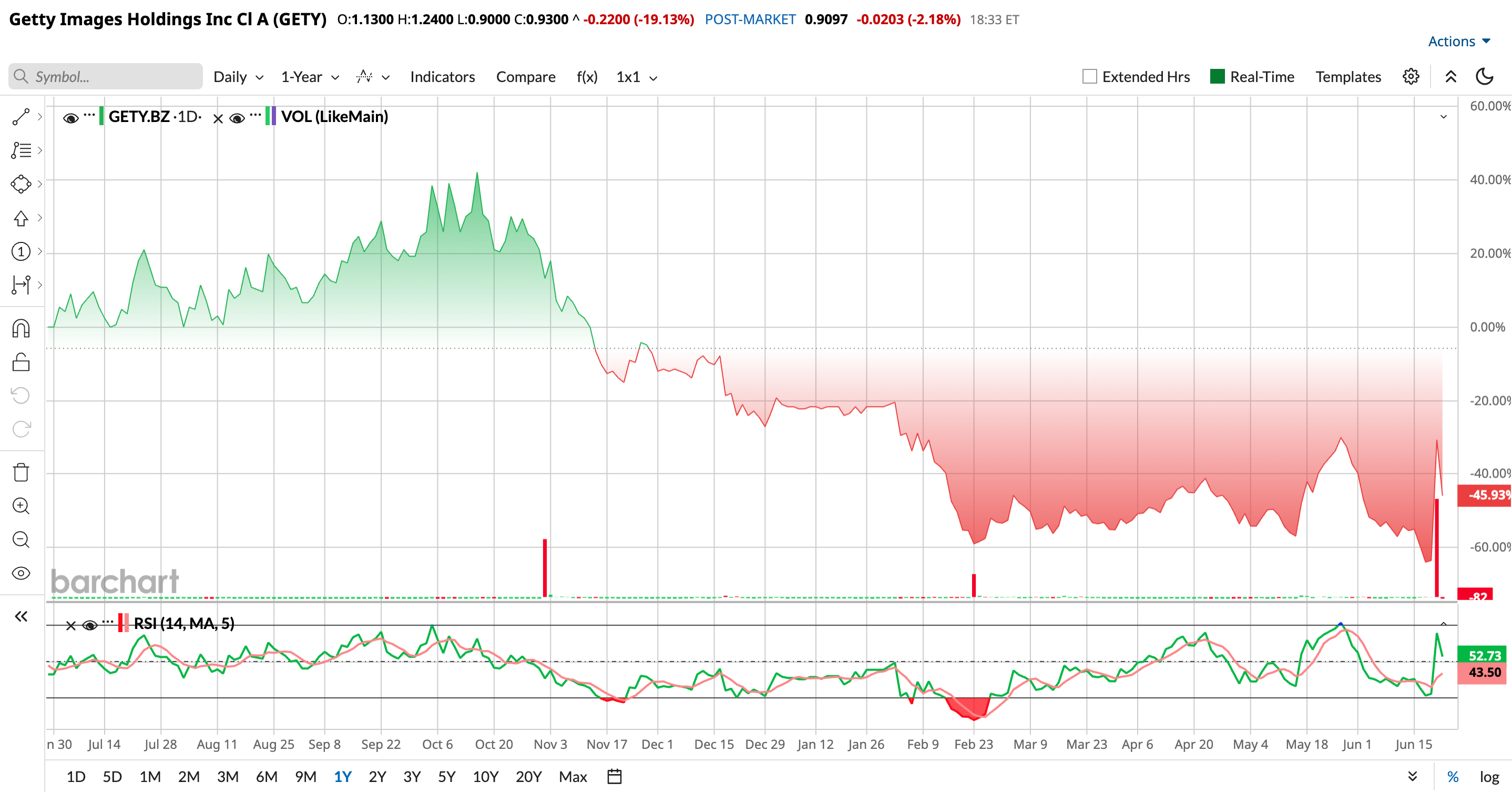

Getty Images’ ride on Wall Street has been anything but a walk in the park. When the company returned to public markets through its SPAC merger in July 2022, shares debuted at around $9.35, and investors came charging in. A famous brand and a limited float turned the stock into the hottest ticket in town, sending it to an intraday peak of $37.88 just days later.

But then the tide turned. Generative AI burst onto the scene, and suddenly the question hanging over Getty was if a computer could whip up an image from a text prompt, then why pay to license one? That story hit the stock like a ton of bricks. Revenue growth slowed, enthusiasm evaporated, and over the next three years, shares gave back more than 75% of their value.

Getty did not wave the white flag. It banned AI-generated content from its platform in 2022 and took Stability AI to court over copyright issues. But investors remained skeptical. Over the past year, the stock declined 49.73%, and it is down 30.6% in 2026. In fact, just last week, GETY hit rock bottom, touching an all-time low of $0.58 on June 18, and now down 71% from its October 2025 high of $3.21.

Then, out of left field, came a twist. Getty’s new licensing deal with OpenAI lit a fire under the stock, sending shares soaring 90% in Monday's session. Yesterday's pullback, with the stock down nearly 15% and trading below $1, suggests traders are taking some chips off the table. Still, after years in the doghouse, Getty may finally have a fresh card to play.

A Snapshot of Getty Images’ Q1 Numbers

Getty Images’ first-quarter report for fiscal 2026 was mixed. There were some bumps in the road, but the company still managed to keep moving forward. CEO Craig Peters said the market remains dynamic, with pressure continuing in areas like Agency and Microstock. Still, he noted that most of the business is seeing growth, helped by strong customer renewals, premium content, and the value Getty brings to clients.

Revenue for the quarter came in at $226.6 million, up 1.1% from a year ago, though it fell short of Wall Street’s expectations. Under that, the picture was mixed. Creative revenue slipped 4.5% to $126.2 million, while Editorial revenue climbed 11% year-over-year (YOY) to $91.7 million. Subscription revenue continued to do the heavy lifting, accounting for 57.4% of total sales, slightly above last year’s level.

On the profitability front, Getty tightened the screws. Adjusted net loss narrowed sharply to $6.5 million, or $0.02 per share, compared with a loss of $58.3 million, or $0.14 per-share loss, a year earlier.

Adjusted EBITDA totaled $61.6 million, down 12.2% YOY, with margins slipping to 27.2% from 31.3%. Management attributed the decline to a change in revenue mix, accounting impacts, and higher expenses tied to covering the Winter Olympics.

Cash generation remained solid. Operating cash flow rose to $40 million, while free cash flow reached $24 million. Getty ended the quarter with $96.6 million in cash and total liquidity of $246.6 million. Restricted cash stood at $640.7 million, while total debt remained sizable at $2 billion.

Some customer metrics moved in the wrong direction. For the last 12 months that ended on March 31, 2026, total purchasing customers fell 4.7% YOY to 675,000, active annual subscribers dropped 19% to 258,000, and paid downloads edged lower to 92 million. Still, subscriber revenue retention held firm at 90%.

Looking ahead, management is keeping a fairly cautious tone. Getty expects full-year 2026 revenue to land between $948 million and $988 million. That range implies anything from a 3.4% decline to modest growth of about 0.6% from last year, suggesting the company still sees some headwinds hanging around. Plus, adjusted EBITDA is estimated to be between $279 million and $295 million, which translates to an annual decline of roughly 8.1% to 12.9% from 2025 levels.

Analysts expect fiscal 2026 revenue to reach about $962.2 million, even as the company posts a loss of roughly $0.03 per share. Losses are expected to widen by 133.3% YOY in fiscal 2027 to -$0.07 per share.

How Bullish Is Wall Street on Getty Images Shares?

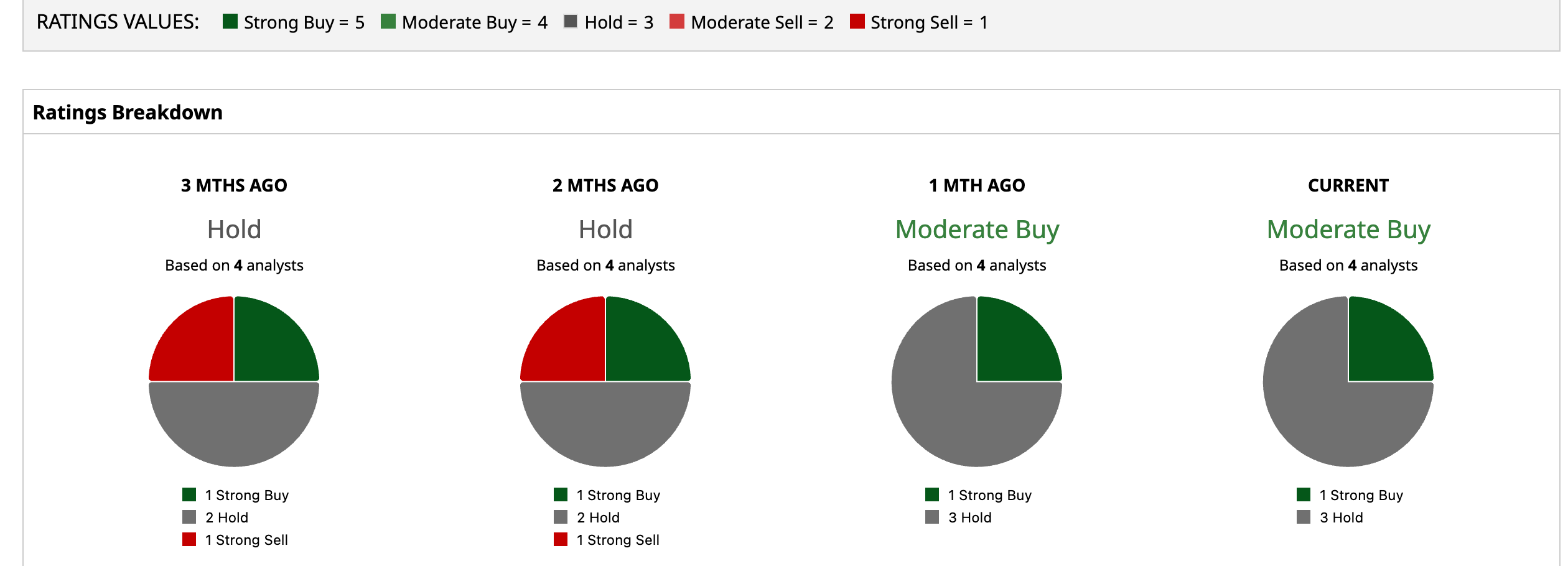

Wall Street appears to be warming up to Getty Images after keeping it on the sidelines for quite some time. A couple of months ago, analysts were sitting on the fence with a “Hold” call, but the mood has brightened, and the stock now carries a consensus “Moderate Buy” rating. Of the four analysts covering the stock, one suggests a “Strong Buy,” and three recommend a “Hold.”

Even so, the numbers are eye-catching. The average price target points to 306.5% upside potential as of writing, and the most bullish target of $7.00 suggests the stock could climb 652.7% if everything falls into place.

Conclusion

For Getty, the OpenAI deal may have changed the mood, but it has not changed all the math. The company still faces a ticking clock to regain compliance with NYSE listing requirements, while its proposed $3.7 billion Shutterstock acquisition remains under regulatory review.

And despite the market’s excitement, the OpenAI announcement leaves plenty between the lines. Financial terms are unknown, and whether Getty’s images can be used to train future AI models remains unanswered – a sensitive issue for the creators whose work built the platform. In other words, Wall Street has embraced the headline, but the fine print may determine whether this is the start of a true comeback or simply a brief bounce after years of decline.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Lululemon%20Athletica%20inc_%20storefront%20by-%20Robert%20Way%20via%20iStock.jpg)

/Semiconductor%20chip%20by%20Mykola%20Pokhodzhay%20via%20iStock.jpg)