Henry Schein, Inc. (HSIC), headquartered in Melville, New York, provides health care products and services to dental practitioners, laboratories, physician practices, and ambulatory surgery centers, government, institutional health care clinics, and other alternate care clinics. Valued at $9 billion by market cap, the company provides shop supplies, as well as dental and medical solutions and services to improve operational success and clinical outcomes.

Companies worth $2 billion or more are generally described as “mid-cap stocks,” and HSIC fits right into that category with its market cap exceeding this threshold, reflecting its substantial size, influence, and dominance in the medical distribution industry. A 94-year leader in healthcare distribution, HSIC is known for quality and reliability. Its product mix spans exclusive deals and private-label consumables serving 1 million+ customers. Under its BOLD+1 plan, acquisitions expand its footprint in software, specialty, and services to fuel digital transformation and long-term growth.

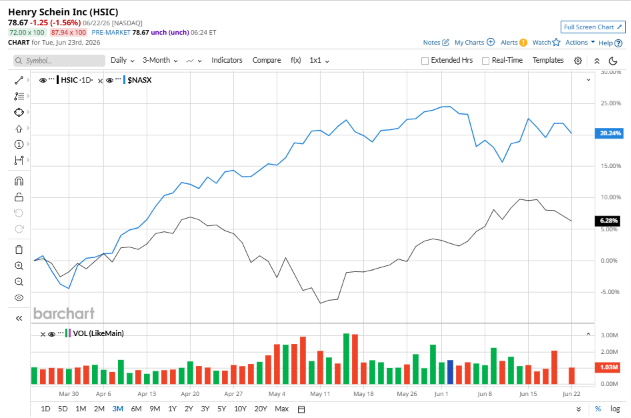

Despite its notable strength, HSIC slipped 11.9% from its 52-week high of $89.29, achieved on Feb. 24. Over the past three months, HSIC stock has gained 5.7%, underperforming the Nasdaq Composite’s ($NASX) 19.2% gains during the same time frame.

Shares of HSIC rose 4.1% on a YTD basis and climbed 9.4% over the past 52 weeks, underperforming NASX’s YTD gains of 12.6% and 33.3% returns over the last year.

To confirm the bullish trend, HSIC has been trading above its 200-day moving average since early November, 2025, with slight fluctuations. The stock is trading above its 50-day moving average since late May.

HSIC’s medical segment softened due to a milder flu season lowering point-of-care diagnostic demand, though strength in Home Solutions and tech offerings largely offset the impact.

On May 5, HSIC shares closed up more than 3% after reporting its Q1 results. Its adjusted EPS of $1.32 exceeded Wall Street expectations of $1.20. The company’s revenue was $3.4 billion, beating Wall Street forecasts of $3.3 billion. HSIC expects full-year adjusted EPS in the range of $5.23 to $5.37.

In the competitive arena of medical distribution, McKesson Corporation (MCK) has lagged behind HSIC, with 9% losses on a YTD basis and 3.4% returns over the past 52 weeks.

Wall Street analysts are reasonably bullish on HSIC’s prospects. The stock has a consensus “Moderate Buy” rating from the 17 analysts covering it, and the mean price target of $88.07 suggests a potential upside of 11.9% from current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)