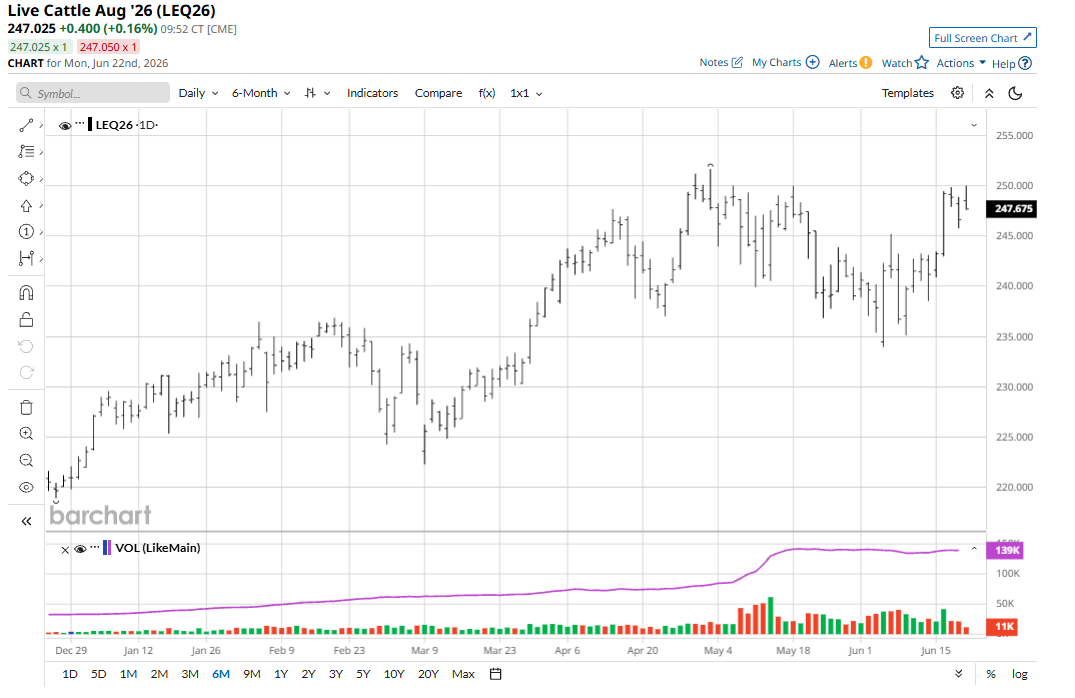

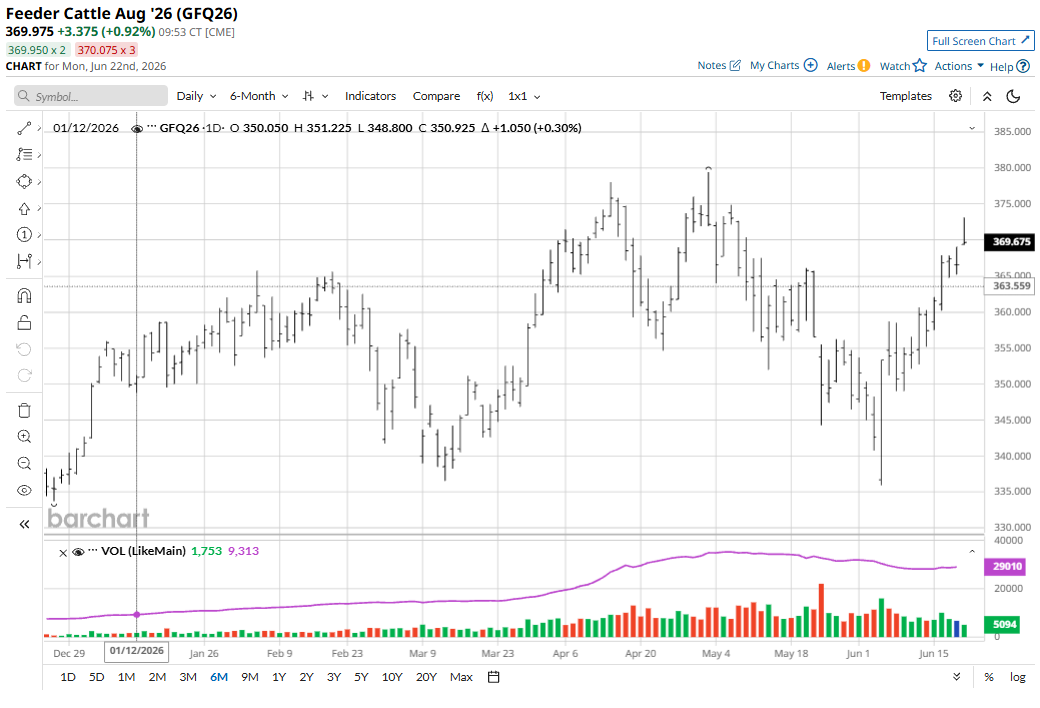

August live cattle (LEQ26) futures last Thursday closed down $2.225 to $246.625 and for the week were up $5.45. August feeder cattle (GFQ26) futures fell $0.825 to $366.60, hit a five-week high, and for the week were up $9.175. The cattle futures bulls have the firm near-term technical advantage as prices are in near-term uptrends. The trend is the bulls’ friend.

The cattle futures bulls got an added boost with last Thursday afternoon’s monthly USDA cattle-on-feed report that leaned price-friendly for futures.

The agency reported U.S. cattle and calves on feed for the slaughter market for feedlots with capacity of 1,000 or more head totaled 11.7 million head on June 1. The inventory was 2% above June 1, 2025. However, placements in feedlots during May totaled 1.70 million head, 10% below 2025. Net placements were 1.65 million head. Marketings of fed cattle during May totaled 1.55 million head, 12% below 2025. Marketings were the second lowest for May since the series began in 1996.

The cattle futures markets are focused on the price-bullish supply ramifications from New World screwworm on the U.S. cattle industry. The USDA Animal and Plant Health and Inspection Service (APHIS) on its NWS website is now reporting 15 total New World screwworm detected cases, still all in Texas and New Mexico.

Cash cattle trading late last week was still very light, with the USDA last Thursday reporting scant cash trading averaging $254.00. That compares to the week prior’s USDA-reported cash cattle trading average of $256.08.

The recent closure of another JBS-owned packing facility, this one in Souderton, Pennsylvania, underscores tight U.S. cattle supplies. Speculative traders have returned to cattle futures in full force as supplies are likely to remain hindered by the lingering closure of the U.S.-Mexico border due to New World screwworm. Also, there is hesitance around domestic herd rebuilding as prices remain elevated and adverse pasture conditions and weather add layers of uncertainty.

The major U.S. stock indexes are not far below their recent record highs. Also, gasoline prices at the pump have dropped below $4.00 a gallon, on average. These are cattle-market-bullish elements that suggest U.S. consumer confidence will be upbeat in the coming months, meaning better demand for beef at the meat counter.

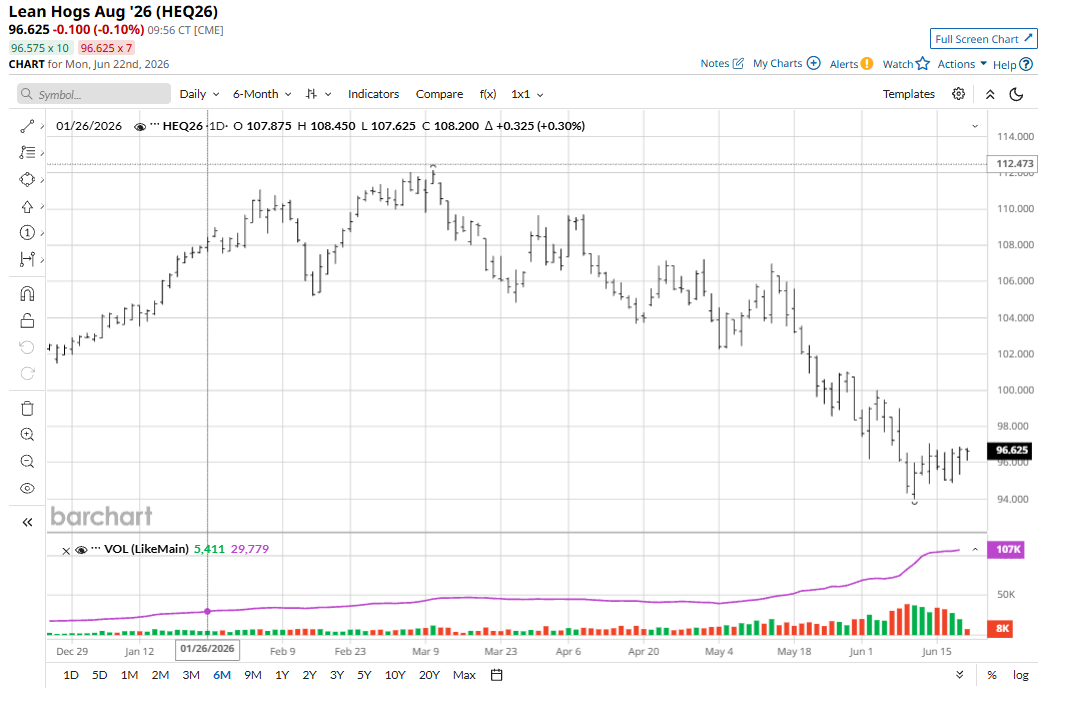

Lean Hog Futures Bears Remain in Firm Control

August lean hog (HEQ26) futures last Thursday rose $0.225 to $96.725 and for the week were up $0.325. Hog futures had a choppy, holiday-shortened trading week as the bulls worked to right the ship but without much success. Prices remain trapped in a downtrend on the daily bar chart.

The U.S. pork export picture also remains dim. The USDA last week reported U.S. pork export sales totaled 16,100 MT for the 2026 marketing year and for the week ended June 11. That was a marketing year low. Net sales were down 31% from the previous week and down 50% from the four-week average.

The latest CME lean hog index is up 50 cents to $92.43. Today’s projected CME index price is up 1 cent at $92.44. The national direct five-day rolling average cash hog price quote for last Thursday was $96.64.

Plentiful pork supplies continue to limit buyer interest in lean hog futures, as slaughter levels continue to outpace those of one year ago. Unlike cattle, hogs are in a gradual supply growth and productivity-driven expansion, keeping futures under pressure.

Demand for pork could improve on substitution demand if American consumers start to become more sensitive to higher-priced beef at the meat counter.

Tell me what you think. I enjoy hearing from my valued Barchart readers from all around the globe. Email me at jim@jimwyckoff.com.

On the date of publication, Jim Wyckoff did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20sign%20at%20the%20headquarters%20by%20VDB%20Photos%20via%20Shutterstock.jpg)

/Space/Cargo%20spacecraft%20in%20low-Earth%20orbit%20by%20Paopano%20via%20Shutterstock.jpg)