Valued at a market cap of $15.8 billion, CF Industries Holdings, Inc. (CF) is a leading global manufacturer and distributor of hydrogen and nitrogen products, serving agricultural, industrial, and clean energy markets. The Northbrook, Illinois-based company’s core product portfolio includes anhydrous ammonia, granular urea, urea ammonium nitrate (UAN), and ammonium nitrate (AN), which are essential for enhancing crop yields and supporting global food security.

Companies valued at $10 billion or more are typically classified as “large-cap stocks,” and CF fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the agricultural inputs industry. The company derives its primary competitive strength from its cost-advantaged North American footprint, which grants the company direct access to plentiful, low-cost natural gas as its primary feedstock.

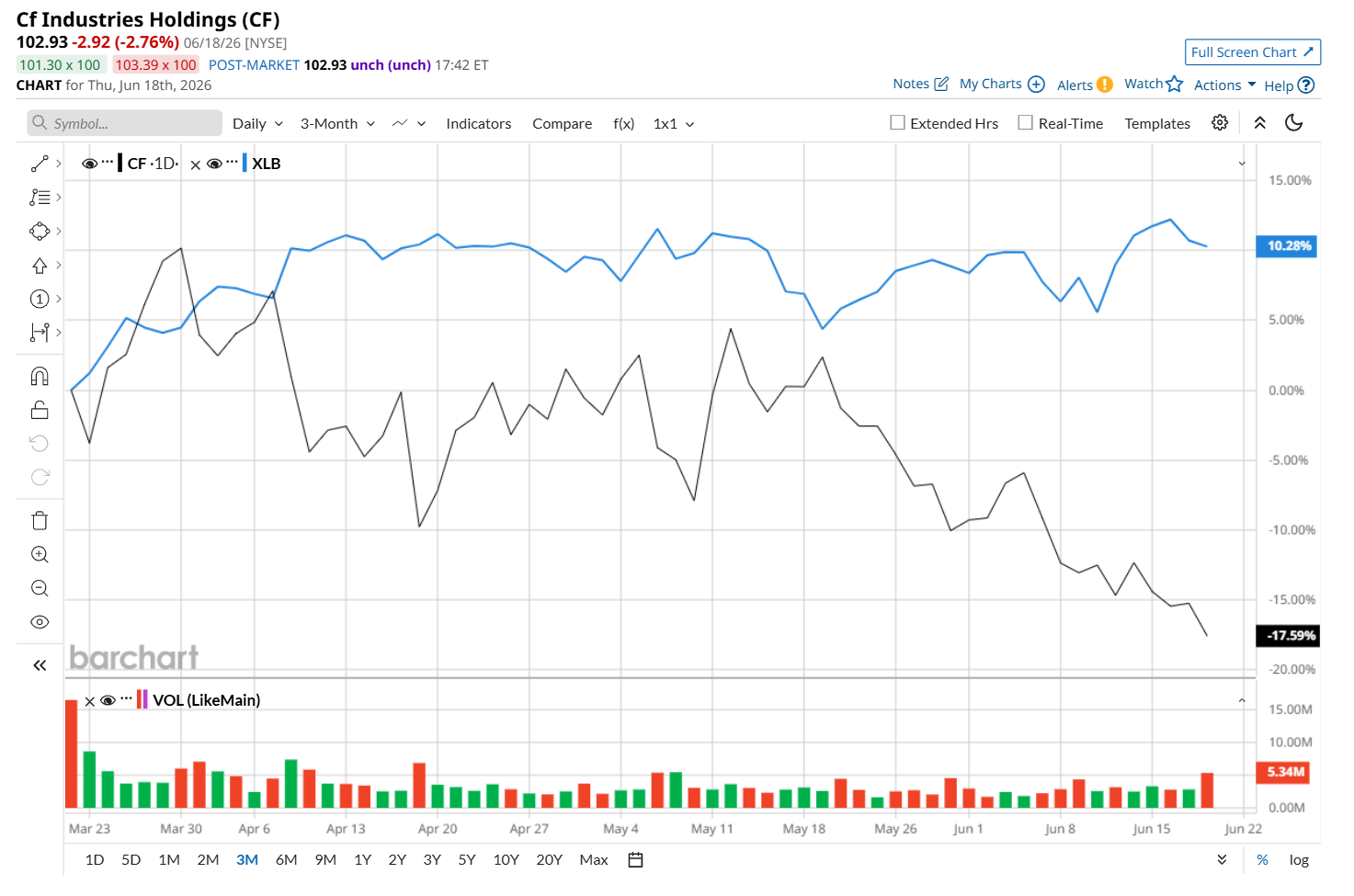

Despite its notable strength, the company had slipped 27.5% from its 52-week high of $141.96, reached on Mar. 30. Shares of CF have declined 18.8% over the past three months, considerably underperforming the State Street Materials Select Sector SPDR ETF’s (XLB) 6.9% uptick during the same time frame.

Moreover, in the longer term, CF has gained 2.6% over the past 52 weeks, notably lagging XLB’s 19.1% return over the same time period. However, on a YTD basis, shares of CF are up 33.1%, outpacing XLB’s 14.2% rise.

To confirm its recent bearish trend, CF has been trading below its 50-day moving average since mid-May. However, it has remained above its 200-day moving average since mid-January.

On May 6, shares of CF tumbled 6.5% despite reporting stronger-than-expected Q1 results. The company’s net sales came in at $2 billion, up 19.4% year-over-year and 12.4% ahead of analysts' estimate. Moreover, on the earnings front, its adjusted EBITDA of $983 million increased 52.6% from the year-ago quarter, while its EPS of $3.98 improved by a notable 115.1%. First quarter 2026 financial results reflect a gain of approximately $170 million from a litigation settlement.

CF has significantly outpaced its rival, The Mosaic Company (MOS), which declined 37.2% over the past 52 weeks and 4.9% on a YTD basis.

Given CF’s recent underperformance, analysts remain cautious about its prospects. The stock has a consensus rating of "Hold” from the 19 analysts covering it, and the mean price target of $123.89 suggests a 20.4% premium to its current price levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/AI%20chip%20by%203Dsss%20via%20Shutterstock.jpg)